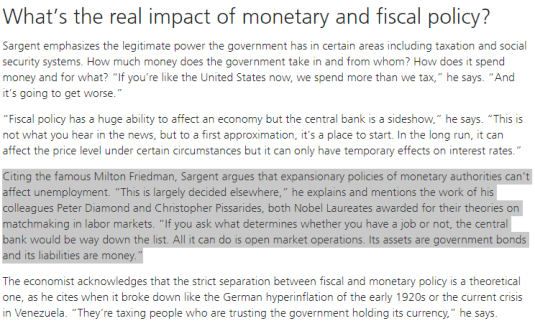

Thomas Sargent:The 2011 Nobel Prize Winner For His Work On Relating Policy & Economics. 2017 interview

30 Aug 2020 Leave a comment

in budget deficits, business cycles, econometerics, economic growth, economic history, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), great depression, great recession, inflation targeting, job search and matching, macroeconomics, monetarism, monetary economics, Robert E. Lucas Tags: monetary policy

2013 BOK Conference Keynote Speeches : Thomas.J.Sargent on liquidity

29 Aug 2020 Leave a comment

in budget deficits, business cycles, economic growth, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), great depression, great recession, history of economic thought, macroeconomics, monetarism, monetary economics, Robert E. Lucas Tags: monetary policy

Thomas J. Sargent on macroeconomics and the crisis 2013

27 Aug 2020 Leave a comment

in budget deficits, business cycles, currency unions, econometerics, economic growth, economic history, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), great depression, great recession, inflation targeting, Jan van Ours, job search and matching, macroeconomics, Milton Friedman, monetarism, monetary economics, Robert E. Lucas, unemployment Tags: monetary policy

“The Recession of 2007 to ?” by Robert E. Lucas – Friedman Forum Lecture 2012

26 Aug 2020 Leave a comment

in budget deficits, business cycles, development economics, econometerics, economic growth, economic history, entrepreneurship, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), great depression, great recession, industrial organisation, inflation targeting, job search and matching, labour economics, labour supply, macroeconomics, monetarism, monetary economics, Robert E. Lucas, unemployment Tags: monetary policy

A history of macroeconomics| Thomas J. Sargent in China 2020

26 Aug 2020 Leave a comment

in Alfred Marshall, applied price theory, budget deficits, business cycles, econometerics, economic growth, economic history, economics of information, Edward Prescott, financial economics, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics, Marxist economics, Milton Friedman, monetarism, monetary economics, politics - USA, Public Choice, public economics, Robert E. Lucas Tags: Keynesian macroeconomics, New Keynesian macroeconomics

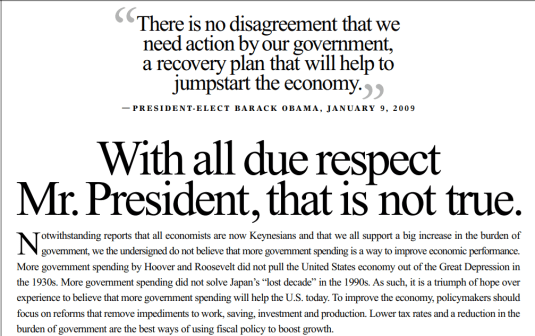

From @Cato ad in @WSJ on 2009 fiscal stimulus @taxpayersUnion @JordNZ

16 Aug 2020 Leave a comment

in applied welfare economics, budget deficits, business cycles, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics, public economics

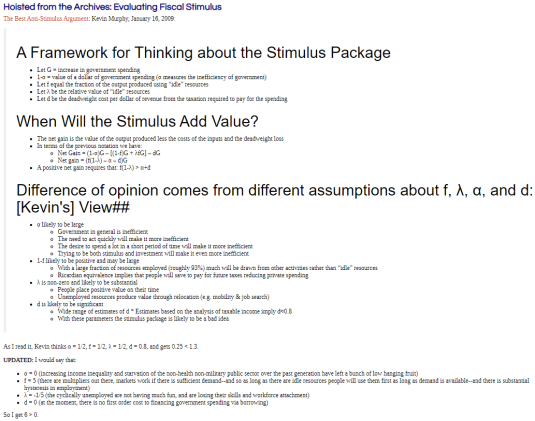

Best Anti-Stimulus Argument in 2009 was from Kevin Murphy @TaxpayersUnion @JordNZ

16 Aug 2020 Leave a comment

in applied price theory, applied welfare economics, business cycles, fiscal policy, macroeconomics, politics - USA, Public Choice, public economics, unemployment

From https://www.bradford-delong.com/2011/10/hoisted-from-the-archives-evaluating-fiscal-stimulus.html and see too https://www.wsj.com/articles/SB123423402552366409

At https://www.chicagobooth.edu/research/igm/events-forums/myron-scholes-forum/speaker-series/2009-01-16 Murphy says

Kevin Murphy sketched out a simple equation—into which anyone could easily plug their own assumptions—to compare the benefits and costs of stimulus spending. The advantage, he argued, is the equation helps everyone to be clear about exactly what they are assuming and why it supports their approach to the stimulus. According to Murphy, the main items everyone should be clear about are: the fraction of the economy’s resources that are idle; the value of keeping those resources idle (e.g., most people value their time, and will not work without compensation); the deadweight loss from raising taxes in the future to pay for the spending; and the cost of allocating spending through government, if it is allocated less efficiently as a result (this can be negative —i.e., a benefit—if government is better than the private sector at allocating resources).

Murphy did not consider the stimulus a good proposal, but he explained how his assumptions about each element of his framework differed from those of president-elect Obama’s team. “It’s easy to see what you have to assume in order to make the stimulus make sense,” Murphy said. Regarding the tax cut measures in the stimulus plan, Murphy thought they were designed in an especially inefficient way. Since marginal tax rates are what matter for incentives, he argued, it was not helpful that the Obama plan would give tax cuts in the form of direct credits to certain taxpayers without lowering rates. That the president would likely address the resulting deficit by raising rates in the future would exacerbate the problem.

And Robert Lucas adds

Robert Lucas pointed out that the US economy was already 4 percent below its long-term trend level in January 2008. In addition, consensus forecasts—which “mean a lot” over short horizons such as a year—suggested the economy would be 8 percent below after another year. This would be larger than any other postwar recession, though nowhere near as bad as the 30 percent gap in the 1930s. “It’s not the worst in my lifetime, but it’s the worst in Obama’s,” Lucas said, “and it would be foolish not to take some actions to deal with it.”

Monetary measures to deal with the recession make a lot of sense, said Lucas, who added that many of the Fed’s actions were beneficial. The trouble was the fiscal stimulus did not seem designed to deal with the real problem. A good approach, Lucas said, would be to use the fiscal stimulus “as another way of getting cash into circulation in the private sector.” He mentioned hypothetical examples that Milton Friedman—dropping money from helicopters—and John Maynard Keynes—paying people to dig and refill ditches—had posed as ways of achieving this. “If fiscal stimuli are designed to be effective, they’re going to be effective because they carry along a monetary policy of the sort that raises the dollar spending level,” Lucas said. Based on the plans and information he had seen from president-elect Obama’s advisors, however, Lucas said that this did not seem to be what the new administration was planning. Instead, he said, “all they’re talking about is transferring resources, additional levels of spending, from one use to another,” which, he argued, would have no substantial effect on the average level of spending and thus would not help fight the recession.

Why The Coronavirus May Forever Change Grocery Shopping | @WSJ

14 Jul 2020 Leave a comment

in budget deficits, business cycles, economic growth, fiscal policy, health economics, macroeconomics, monetary economics, public economics Tags: creative destruction, economics of pandemics

How Much Spending Is OK Before Inflation Takes Over?

02 Jul 2020 Leave a comment

in fiscal policy, macroeconomics, monetary economics Tags: economics of pandemics, monetary policy

Does cutting interest rates further matter?

12 Jun 2020 Leave a comment

in business cycles, financial economics, fiscal policy, job search and matching, macroeconomics, Milton Friedman, monetarism, monetary economics, unemployment

Unpleasant arithmetic hyperinflation – Tom Sargent is lecturing via YouTube

31 May 2020 Leave a comment

in budget deficits, economic history, financial economics, fiscal policy, macroeconomics, monetarism, monetary economics Tags: hyperinflation, monetary policy

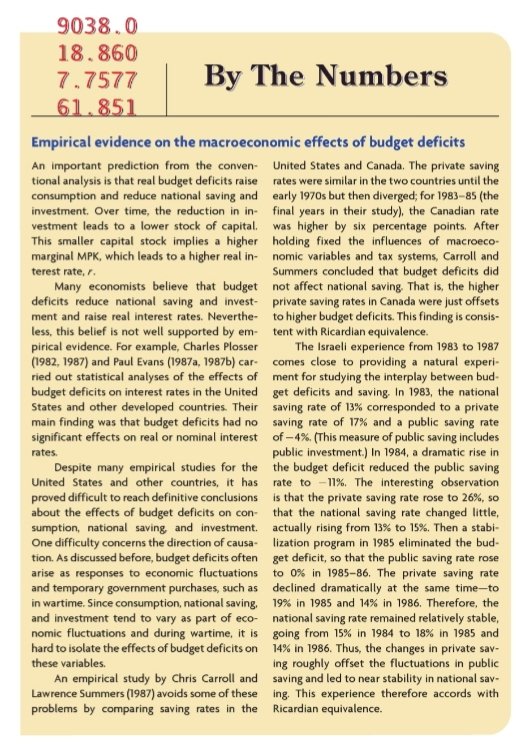

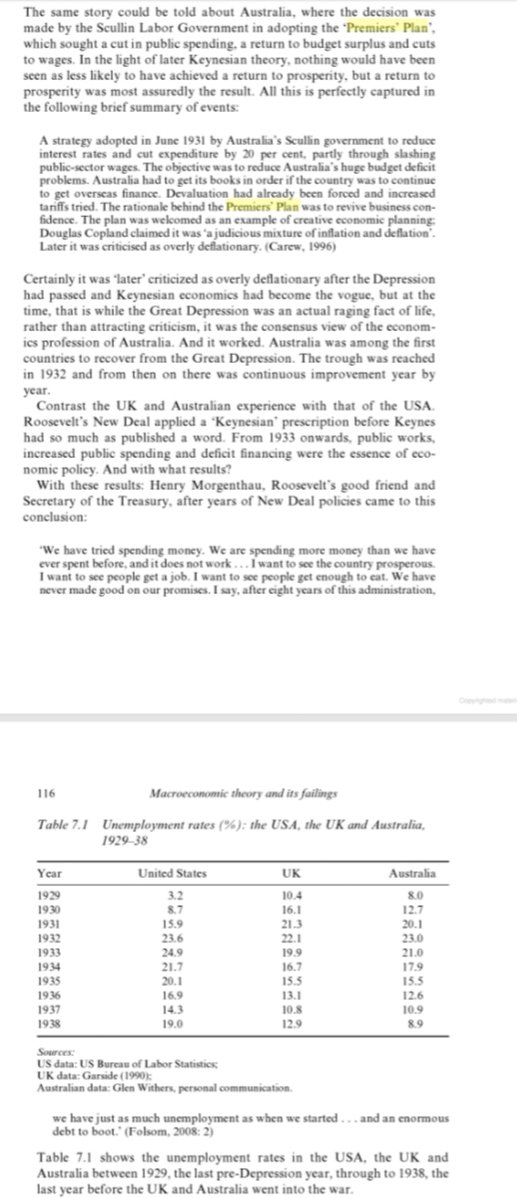

The Premiers’ Plan versus the New Deal. Do Keynesian macroeconomists ever study 1930s Australia

30 May 2020 Leave a comment

in budget deficits, business cycles, economic history, fiscal policy, great depression, history of economic thought, job search and matching, labour economics, labour supply, macroeconomics, Milton Friedman, monetarism, monetary economics, politics - Australia, politics - USA, public economics, unemployment Tags: Keynesian macroeconomics, new classical macroeconomics, New Keynesian macroeconomics

Recent Comments