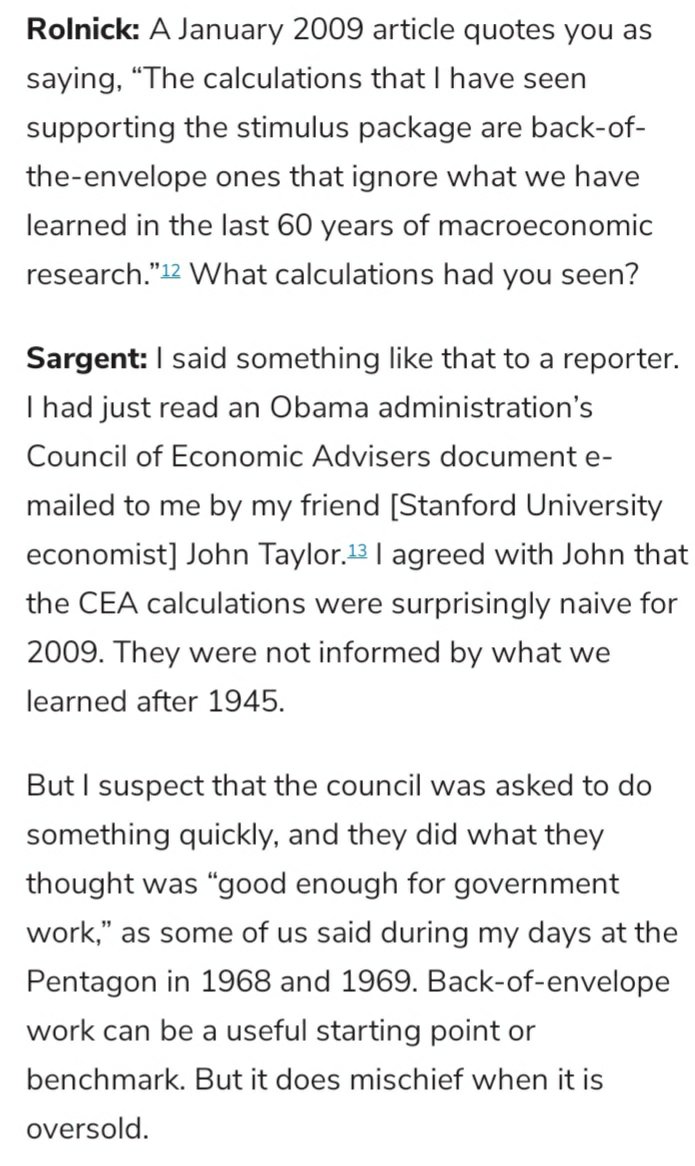

Tim Sablik of the Richmond Fed interviews “Ellen McGrattan: On measuring what businesses do, developing effective tax policy, and searching for answers beyond the lamppost” (Econ Focus: Federal Reserve Bank of Richmond, First/Second Quarter 2026). Here are a few of the comments that caught my eye: How did McGrattan become interested in business cycles? In…

Interview with Ellen McGrattan: Business Cycles and Intangible Capital

Interview with Ellen McGrattan: Business Cycles and Intangible Capital

17 Apr 2026 Leave a comment

in business cycles, Edward Prescott, entrepreneurship, financial economics, global financial crisis (GFC), great recession, history of economic thought, human capital, labour economics, macroeconomics, monetary economics, occupational choice, Robert E. Lucas

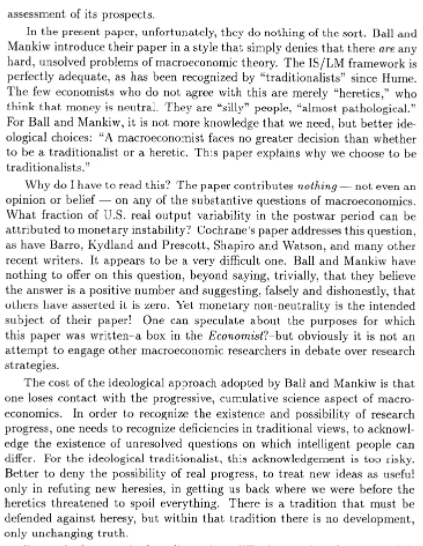

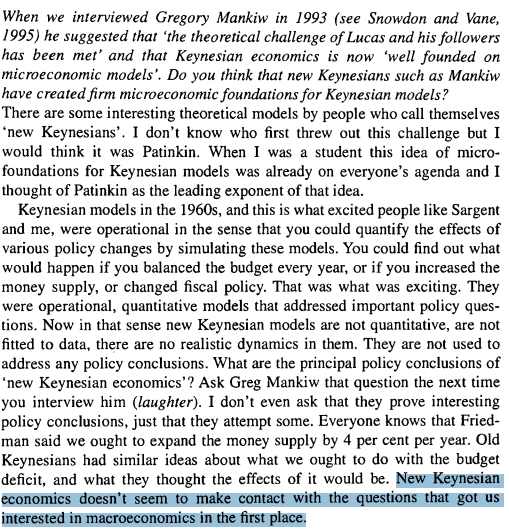

Interview with Greg Mankiw: New Keynesian Macro, Growth, and Economic Policy

04 Sep 2024 Leave a comment

in applied price theory, budget deficits, business cycles, development economics, econometerics, economic growth, economic history, Edward Prescott, fiscal policy, great depression, history of economic thought, labour economics, law and economics, macroeconomics, Milton Friedman, monetarism, monetary economics, politics - USA, Public Choice, Robert E. Lucas, unemployment

Jon Hartley interviews Greg Mankiw on topics including New Keynesian macroeconomics, growth, and economic policy more broadly at his Capitalism and Freedom website (August 20, 2024, video and transcript available). Here are a few of the comments that caught my eye. On big models and small models in studying the macroeconomy: [O]n the issue of…

Interview with Greg Mankiw: New Keynesian Macro, Growth, and Economic Policy

Bob Lucas on Growth, Poverty and Business Cycles 2/5/2007

19 May 2023 Leave a comment

in business cycles, comparative institutional analysis, development economics, economic history, economics of education, growth disasters, growth miracles, history of economic thought, human capital, labour economics, law and economics, macroeconomics, Milton Friedman, monetarism, monetary economics, Robert E. Lucas, unemployment Tags: monetary policy

This paper attempts to resolve the paradox of Friedmanian monetary theory: “Money is a veil, but when the veil flutters, real output sputters.”

07 Sep 2022 Leave a comment

in business cycles, history of economic thought, macroeconomics, Milton Friedman, monetarism, monetary economics, Robert E. Lucas

The Lucas Revolution 50 years ago

04 Sep 2022 Leave a comment

in history of economic thought, macroeconomics, Robert E. Lucas

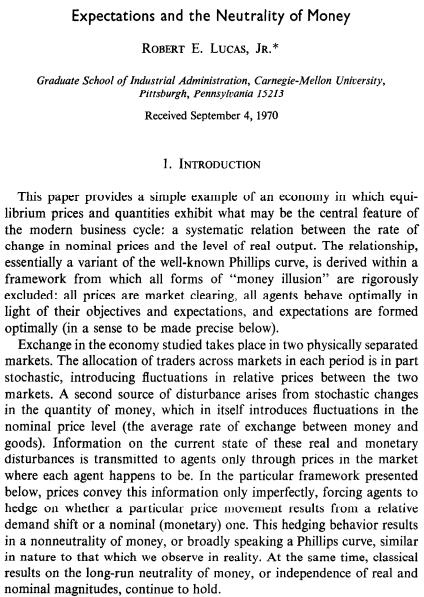

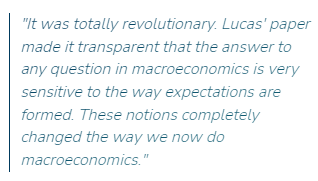

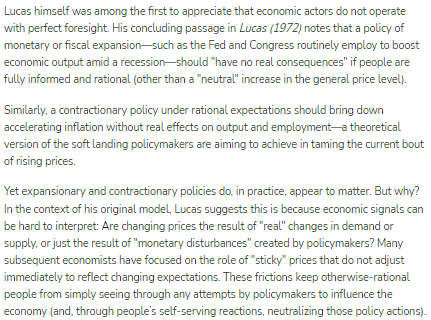

Expectations and the power of policy

03 Sep 2022 Leave a comment

in applied price theory, business cycles, econometerics, fiscal policy, macroeconomics, monetary economics, Robert E. Lucas, unemployment

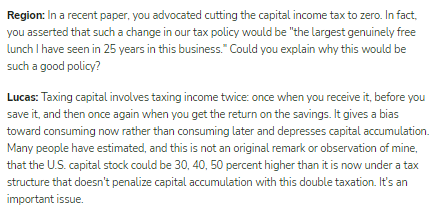

Robert Lucas on optimal taxation of capital

15 Jul 2022 Leave a comment

in applied welfare economics, economic growth, macroeconomics, public economics, Robert E. Lucas

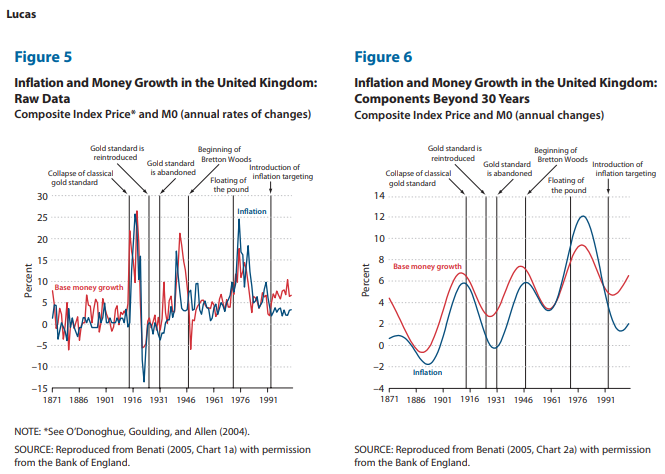

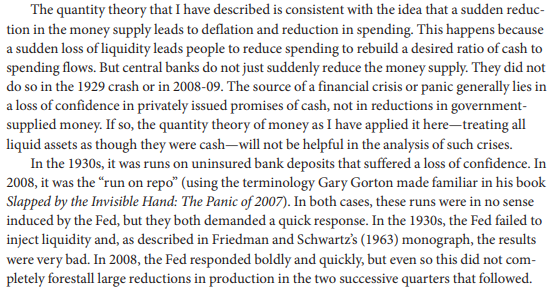

The long-run relation between base money and inflation rates

24 Apr 2022 Leave a comment

in economic history, macroeconomics, monetary economics, Robert E. Lucas

Lucas, the quantity theory and the GFC

23 Apr 2022 Leave a comment

in business cycles, global financial crisis (GFC), macroeconomics, monetary economics, Robert E. Lucas

The Lucas critique summarised by Freeman and Champ

22 Apr 2022 Leave a comment

in budget deficits, business cycles, economic growth, labour economics, labour supply, macroeconomics, monetarism, monetary economics, Robert E. Lucas

Freeman and Champ explain the Lucas revolution

15 Apr 2022 Leave a comment

in business cycles, economic growth, history of economic thought, labour economics, labour supply, macroeconomics, monetarism, monetary economics, Robert E. Lucas, unemployment

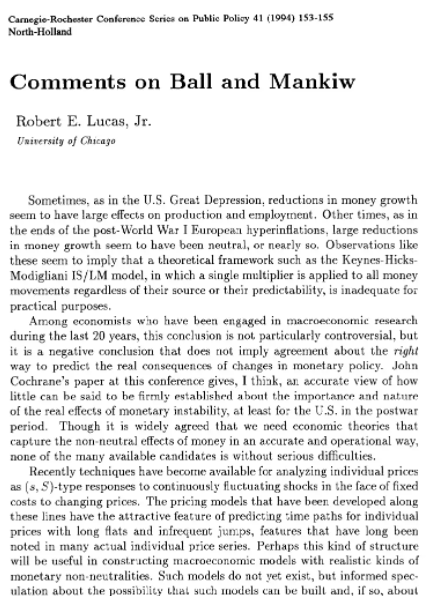

Lucas hooks into Mankiw and Ball

19 Feb 2022 Leave a comment

in business cycles, history of economic thought, macroeconomics, Robert E. Lucas

from https://www.reddit.com/r/Economics/comments/1w22mc/comments_on_ball_and_mankiw_robert_lucas_1994/

Robert Lucas: Labor Reform and Crisis Recovery

28 Jan 2022 Leave a comment

in applied price theory, applied welfare economics, business cycles, comparative institutional analysis, econometerics, economic growth, economic history, economics of regulation, labour economics, labour supply, macroeconomics, Robert E. Lucas Tags: employment law

Recent Comments