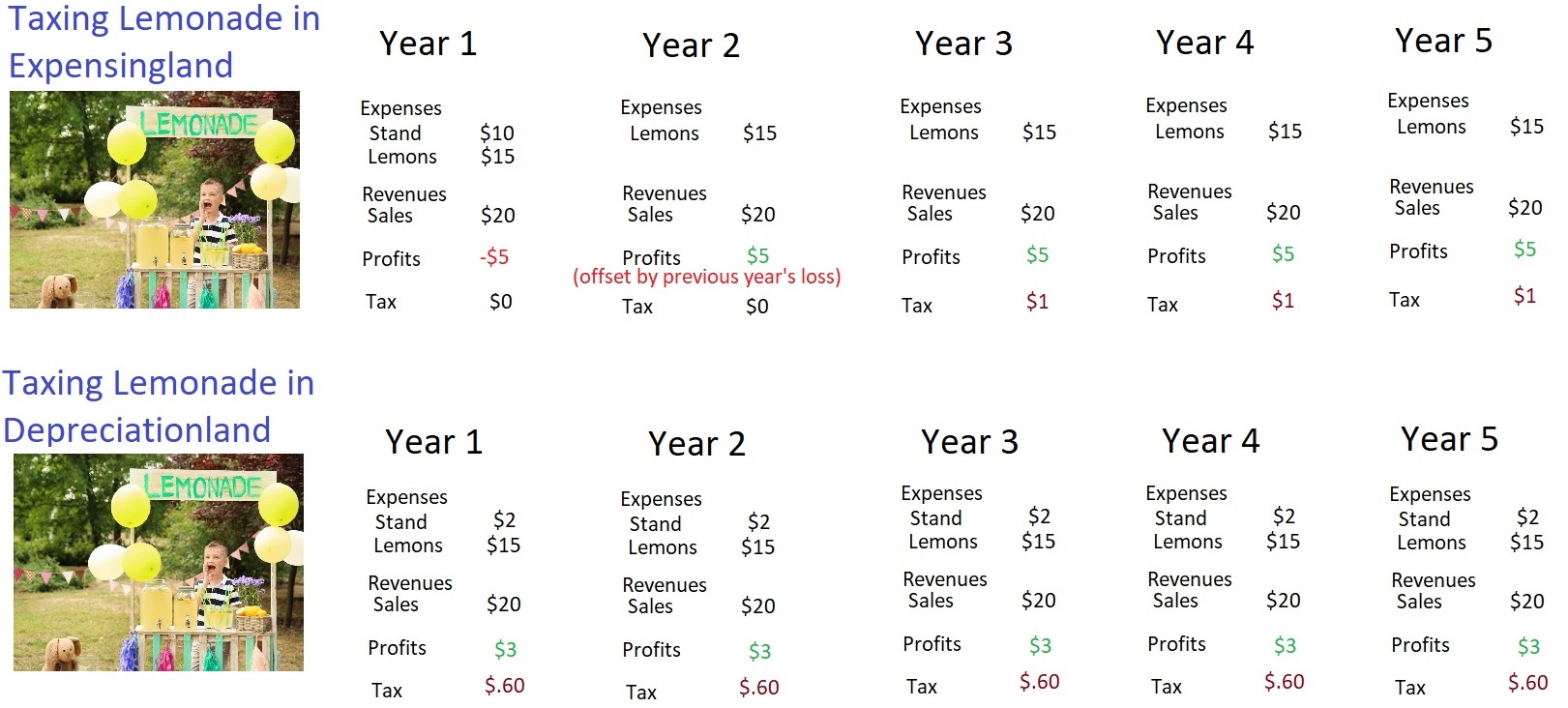

Zwick and Zidar argue that a substantial share of the decline in labor share can be accounted for by changing forms of pay, including pass-throughs and equtiy compensation. In particular, if an employee is paid in stock and that stock increases in value then the tax rules tend to count some of that as capital…

Capital Gains Can Be Labor Income

Capital Gains Can Be Labor Income

10 Jul 2026 Leave a comment

in applied price theory, fiscal policy, macroeconomics, Public Choice, public economics Tags: taxation and entrepreneurship, taxation and investment, top 1%

Callaghan failure

14 Jun 2026 Leave a comment

in applied price theory, economics of bureaucracy, industrial organisation, politics - New Zealand, Public Choice, public economics, rentseeking, survivor principle, theory of the firm Tags: industry policy, picking losers

The Post reports: Nearly a third of the Callaghan Innovation’s $149 million Covid-era research and development loan book is in arrears, including $21.5m linked to 63 failed or insolvent businesses, as the agency enters its final months before disestablishment. Callaghan Innovation – a government entity set up to make businesses around the country more innovative…

Callaghan failure

Piketty’s Eco-Marxist Utopia: Why Degrowth and Global Redistribution Will Trap the Poor in Poverty

13 Jun 2026 Leave a comment

in applied price theory, development economics, econometerics, economic growth, economic history, economics of climate change, economics of regulation, energy economics, environmental economics, environmentalism, fiscal policy, global warming, human capital, income redistribution, industrial organisation, international economics, labour economics, labour supply, macroeconomics, Public Choice, public economics Tags: climate activists, climate alarmism, regressive left

The world’s poor deserve better than another utopia designed for them by the globalist intelligentsia. They deserve cheap energy, open markets, secure property rights, and the freedom to industrialise on terms they choose for themselves. That is what worked in East Asia. It is what will work in South Asia, Africa and Latin America. And…

Piketty’s Eco-Marxist Utopia: Why Degrowth and Global Redistribution Will Trap the Poor in Poverty

Professors Behind the California Wealth Tax Threaten Possible Legal Action Against Critic

11 Jun 2026 Leave a comment

in income redistribution, law and economics, politics - USA, Public Choice, public economics Tags: taxation and entrepreneurship, taxation and investment

There is an interesting controversy brewing in California after four California university professors threatened a political candidate, Richard Lucas, for…

Professors Behind the California Wealth Tax Threaten Possible Legal Action Against Critic

Superannuation affordability options

09 Jun 2026 Leave a comment

in economic growth, fiscal policy, income redistribution, labour economics, labour supply, macroeconomics, politics - New Zealand, Public Choice, public economics Tags: ageing society, economics of immigration, population bust

Lyric Waiwiri-Smith at The Spinoff asked me what I thought the options might be for dealing with rising superannuation costs. Her story’s here, along with comment from Max Rashbrooke and Shamubeel Eaqub. My most-preferred option is ongoing increases in immigration rates, coupled with shifting to CPI-indexation of super benefits and indexing the age of eligibility to healthy…

Superannuation affordability options

Europe’s War on Wealth

29 May 2026 Leave a comment

in applied price theory, economic growth, economic history, fiscal policy, income redistribution, industrial organisation, labour economics, labour supply, macroeconomics, occupational choice, P.T. Bauer, poverty and inequality, Public Choice, public economics Tags: European Union

Given the relative economic weakness that plagues most European nations (documented here, here, here, here, and here), a top priority for policy makers should be to improve incentives for wealth creation. But that assumes politicians care about the prosperity of citizens. Based on a new report from the European Commission, the answer is no. Instead of […]

Europe’s War on Wealth

Liberal Economists Score an Own Goal Against Bezos

25 May 2026 Leave a comment

in applied price theory, fiscal policy, James Buchanan, labour economics, labour supply, macroeconomics, Public Choice, public economics

Jeff Bezos tweeted: Yes, the United States has the most progressive tax system in the world. The top 1% pay 40% of taxes, the bottom 50% pay 3% of taxes. We can make it even more progressive by zeroing out taxes on the bottom half. It’s a small amount of the total tax revenue but…

Liberal Economists Score an Own Goal Against Bezos

The (Amusingly) Destructive Economics of Wealth Taxation

24 May 2026 Leave a comment

in applied price theory, economic growth, entrepreneurship, fiscal policy, human capital, income redistribution, labour economics, labour supply, macroeconomics, poverty and inequality, Public Choice, public economics Tags: taxation and entrepreneurship, taxation and investment, taxation and labour supply

I’ve shared several columns (here, here, here, here, and here) reviewing scholarly research on the harmful economic impact of wealth taxation. From now on, however, I think I’ll simply share this clever video from the folks at Reason. The video uses humor to make very important points about how a wealth tax would diminish incentives […]

The (Amusingly) Destructive Economics of Wealth Taxation

The Rise and Fall (and Rise) of Sweden, Part IV

23 May 2026 Leave a comment

in applied price theory, comparative institutional analysis, economic growth, economic history, economics of regulation, industrial organisation, international economics, macroeconomics, public economics Tags: Sweden

I don’t often claim to be ahead of the curve, but I’m going to pat myself on the back in today’s column about Swedish economic policy. More than 16 years ago, I started writing about Sweden’s shift from statism to markets. More than 14 years ago, I praised Swedish policy makers for significantly reducing the […]

The Rise and Fall (and Rise) of Sweden, Part IV

Iceland’s Superb Private Retirement System

17 May 2026 Leave a comment

in fiscal policy, labour economics, macroeconomics, Public Choice, public economics Tags: Iceland

Over the years, I’ve written about the successful private retirement systems in jurisdictions such as Australia, Chile, Switzerland, Hong Kong, Netherlands, the Faroe Islands, Denmark, Israel, and Sweden. Today’s column will add to the collection because we’re going to look at Iceland’s remarkable system of personal retirement accounts. We’ll start with two charts. Here’s a […]

Iceland’s Superb Private Retirement System

The Washington Post vs Elizabeth Warren

25 Apr 2026 Leave a comment

in applied price theory, economics of media and culture, fiscal policy, human capital, income redistribution, labour economics, labour supply, macroeconomics, politics - USA, Public Choice, public economics Tags: taxation and entrepreneurship, taxation and investment, taxation and labour supply

People sometimes will get excited about big-picture tax fights – whether politicians should raise taxes, whether they should add a VAT, or whether they should scrap the IRS for a flat tax. On the other had, there are a handful of tax issues that induce drowsiness but are nonetheless very important for purposes of tax […]

The Washington Post vs Elizabeth Warren

The Laffer Curve and Limits to Class Warfare Tax Policy, Part II

19 Apr 2026 Leave a comment

in applied price theory, econometerics, entrepreneurship, fiscal policy, human capital, income redistribution, labour economics, labour supply, macroeconomics, poverty and inequality, Public Choice, public economics Tags: taxation and entrepreneurship, taxation and investment, taxation and labour supply

In Part I of this series back in 2014, we looked at some academic research from Canada showing that the revenue-maximizing tax rate on the richest taxpayers was 27.5 percent. A key insight from that research is that high-income taxpayers have considerable control over the timing, level, and composition of their income (just like in […]

The Laffer Curve and Limits to Class Warfare Tax Policy, Part II

Chi-Town Meltdown: Chicago Ramps Up Taxes and Debt in Familiar Death Spiral

23 Mar 2026 Leave a comment

in politics - USA, public economics, urban economics

As a Chicago native, I have watched my home city unravel under the policies of Mayor Brandon Johnson and the…

Chi-Town Meltdown: Chicago Ramps Up Taxes and Debt in Familiar Death Spiral

103 ways for local government to save money

17 Mar 2026 Leave a comment

in economics of bureaucracy, politics - New Zealand, Public Choice, public economics

The Taxpayer’s Union has done a report listing 103 ways local government can save money. Some of the more significant ones which I support are: The post 103 ways for local government to save money first appeared on Kiwiblog.

103 ways for local government to save money

Fleecing Rich Taxpayers: Europe vs. the United States

13 Mar 2026 Leave a comment

in applied price theory, entrepreneurship, human capital, income redistribution, labour economics, labour supply, politics - USA, Public Choice, public economics Tags: taxation and entrepreneurship, taxation and investment, taxation and labour supply

I frequently make the point that America’s tax system is more progressive than European tax systems. But not because the United States imposes higher tax rates on upper-income households. Instead, the big difference is that lower-income and middle-class households in the United States face much lower tax burdens than their European counterparts. In those columns, […]

Fleecing Rich Taxpayers: Europe vs. the United States

Recent Comments