Hayek (1950) on why the current stimulus will fail

18 Mar 2020 Leave a comment

in Austrian economics, business cycles, economic history, economics of information, F.A. Hayek, fiscal policy, history of economic thought, labour economics, labour supply, macroeconomics, monetary economics, occupational choice, Public Choice, public economics Tags: fiscal policy, Keynesian macroeconomics

Fama in full on fiscal policy

27 Feb 2020 Leave a comment

Fama on a fiscal stimulus

25 Feb 2020 1 Comment

in applied price theory, budget deficits, business cycles, economic growth, financial economics, fiscal policy, global financial crisis (GFC), great recession, labour economics, labour supply, macroeconomics, monetary economics, politics - USA, Public Choice, public economics Tags: fiscal policy

Paul Samuelson on where he disagreed with Milton Friedman on macroeconomic policy

19 Mar 2015 Leave a comment

in budget deficits, business cycles, economic growth, fiscal policy, inflation targeting, macroeconomics, Milton Friedman, monetarism, monetary economics Tags: fiscal policy, monetary policy, Paul Samuelson, rules versus discretion, stabilisation policy

via Samuelson vs. Friedman, David Henderson | EconLog | Library of Economics and Liberty and An Interview With Paul Samuelson, Part One — The Atlantic.

Deflation and Depression: Is There an Empirical Link?

31 Jan 2015 Leave a comment

in budget deficits, business cycles, economic growth, Euro crisis, great depression, great recession, macroeconomics, monetary economics, politics - Australia, politics - New Zealand, politics - USA Tags: deflation, fiscal policy, liquidity traps, monetary policy, stabilisation policy

Deflation has a bad reputation. People blame deflation for causing the great depression in the 1930s. What worse reputation can you get as a self-respecting macroeconomic phenomena?

The inconvenient truth for this urban legend is empirical evidence of deflation leading to a depression is rather weak.

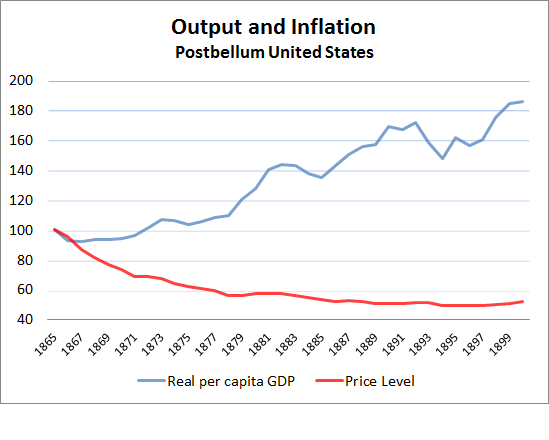

The most obvious is confounding evidence, is up until the great depression, deflation was commonplace. In the late 19th century, deflation coincided with strong growth, growth so strong that it was called the Industrial Revolution.

For deflation to be a depressing force, something must have happened in the lead up to the Great Depression to change the impact of deflation on economic growth.

Atkeson and Kehoe in the AER looked into the relationship between deflation and depressions and came up empty-handed.

Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

Deflation and Depression: Is There an Empirical Link?

Andrew Atkeson, and Patrick J. Kehoe, 2004.

Are deflation and depression empirically linked? No, concludes a broad historical study of inflation and real output growth rates. Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

View original post 1,842 more words

Earl A. Thompson on fiscal and monetary policy in the Great Recession

09 Oct 2014 Leave a comment

in budget deficits, business cycles, economic growth, fiscal policy, great recession, macroeconomics, monetary economics Tags: crowding out, Earl A. Thomson, fiscal policy, great depression, great recession, permanent income hypothesis, Ricardian equivalence

Krugman explains why a broken window is a fiscal stimulus

27 Sep 2014 Leave a comment

HT: Robert P. Murphy

The broken window fallacy explained

27 Sep 2014 Leave a comment

in fiscal policy, macroeconomics Tags: broken window fallacy, crowding out, externalities, fiscal policy

Keynesian analysis implicitly assumes that a fiscal deficit does not have any effects on other spending

01 Aug 2014 1 Comment

in budget deficits, fiscal policy, macroeconomics, Milton Friedman, monetarism Tags: budget deficits, fiscal policy, fiscal stimulus, Milton Friedman

The

The

Eugene Fama and the simulative effects of fiscal policy

31 Jul 2014 6 Comments

in budget deficits, fiscal policy, great depression, great recession, macroeconomics Tags: crowding out, Eugene Fama, fiscal policy, Treasury view of fiscal policy

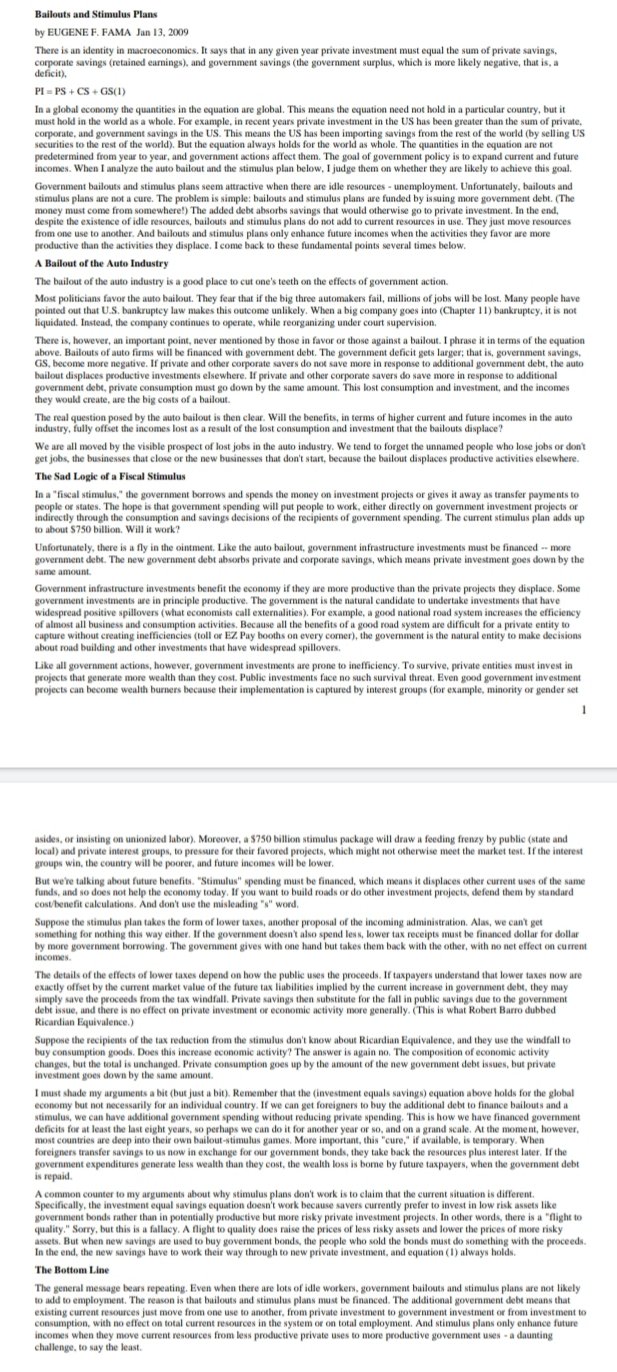

Eugene Fama argues that government bailouts and stimulus plans seem attractive when there are idle resources – when there is unemployment such as in a recession or depression including in the 1930s.

Fama counters that:

1. Bailouts and stimulus plans must be financed.

2. If the financing takes the form of additional government debt, the added debt displaces other uses of the funds.

3. Thus, stimulus plans only enhance incomes when they move resources from less productive to more productive uses.

In the end, despite the existence of idle resources, bailouts and stimulus plans do not add to current resources in use. They just move resources from one use to another.

Fama noted that there was just one valid negative comment in response to this argument that appears to be valid which was made by Brad DeLong.

Fama thinks Delong’s point about involuntary inventory accumulation is consistent with Fama’s initial arguments about the need for the stimulus to work through moving resources to higher value uses.

For me, the notion that a fiscal stimulus is a negative productivity shock is a good starting point for analysis. The method of financing the stimulus is important too.

Economic agents know that a temporary expenditure program has no lasting effect on employment but has lasting effect on disposable income and taxes. Indeed, massive public interventions to maintain employment and investment during a financial crisis can, if they distort incentives enough, lead to a depression.

In Australia, there was a massive fiscal contraction from late 1930 onwards called the Premiers’ Plan. In 1931, unemployment rates was 25% or more.

- The Premiers’ Plan required the federal and state governments to cut spending by 20%, including cuts to wages and pensions and was to be accompanied by tax increases, reductions in interest on bank deposits and a 22.5% reduction in the interest the government paid on internal loans.

- The Premiers’ Plan was complementary to the Arbitration Court’s 10 per cent nominal wage cut in January 1931 and the devaluation of the Australian pound. Most countries had abandoned the gold standard by 1931 and 1932 and devalued by about 10% including the UK. These competitive devaluations were called currency wars. Most countries below started to recovery before they left the gold standard, a year or two before they left the cross of gold.

Maclaren (1936) dated the Australian economic recovery from the last months of 1932. It was to take another three years before unemployment rates fell below 10 per cent — the rate it had been during most of the 1920s.

The June 1931 Premiers’ Plan of fiscal consolidation had time by late 1932 to become credible and take hold given the usual leads and lag on fiscal policy. Unemployment data for the time show a rapid fall in the high twenties unemployment rate in 1932 to be below 10 per cent by 1937.

Does fiscal policy cause inflation?

11 Jul 2014 Leave a comment

in budget deficits, fiscal policy, macroeconomics, Milton Friedman, monetary economics Tags: budget deficits, fiscal policy, inflation

Robert Lucas explained his support for U.S. monetary policy in 2008 as follows

10 Jul 2014 Leave a comment

in global financial crisis (GFC), great recession, macroeconomics, Robert E. Lucas Tags: fiscal policy, GFC, monetary policy, Robert Lucas

- There are many ways to stimulate spending, but monetary policy was the most helpful counter-recession action because it was fast and flexible.

- There is no other way that so much cash could have been put into the system as fast, and if necessary it can be taken out just as quickly. The cash comes in the form of loans.

- There is no new government enterprises, no government equity positions in private enterprises, no price fixing or other controls on the operation of individual businesses, and no government role in the allocation of capital across different activities. These were important virtues.

Brad Delong and Larry Summers on the ineffectiveness of fiscal policy in stimulating the economy

05 Jul 2014 3 Comments

Repeat after me: fiscal policy is ineffective when there is a flexible exchange rate!

04 Jul 2014 2 Comments

in fiscal policy, macroeconomics Tags: exchange rate crowding out, fiscal policy, Mundell Fleming model

New Zealand, Australia, and most other economies are small open economies. Any expansion in the budget deficit will drive up the exchange rate because of the higher interest rates. This appreciation of the local currency in response to the capital inflow will make imports cheaper. Any increase in so-called aggregate demand will simply result in an decrease in net exports. There will be no increase in local production or employment.

- a fiscal expansion puts upward pressure on the domestic interest rate

- But this immediately invites a massive capital inflow.

- This appreciates the nominal exchange rate.

- This will decrease net exports, since we are able to import more goods and services with less money because of the currency appreciation, while foreigners will import less of our products because of our appreciated domestic currency

- The exchange rate appreciates and the trade balance worsens until the initial increase in government spending is completely offset.

Under a floating exchange rate and high capital mobility, fiscal policy is ineffective in stimulating the economy because of exchange rate crowding out. The appreciating exchange rate will increase imports and reduce exports to render fiscal policy impotent or at least to shadow of its former closed economies self.

Recent Comments