Interview: Eugene F. Fama, 2013 Prize in Economic Sciences

23 Sep 2018 Leave a comment

in applied price theory, economics of information, entrepreneurship, financial economics Tags: Eugene Fama

Eugene Fama’s advice for the next president

01 Dec 2016 Leave a comment

in applied price theory, constitutional political economy, economics of regulation, entrepreneurship, financial economics Tags: 2016 presidential election, Eugene Fama

Are markets efficient? Eugene Fama (yes!) and Richard Thaler (no!) debate

30 Nov 2016 Leave a comment

in applied price theory, behavioural economics, entrepreneurship, financial economics Tags: active investing, efficient markets hypothesis, Eugene Fama, passive investing

Eugene Fama Why Small Caps and Value Stocks Outperform

09 Nov 2016 Leave a comment

in applied price theory, economic history, entrepreneurship, financial economics Tags: efficient market hypothesis, Eugene Fama

Eugene Fama on what is a bubble

19 Jun 2015 Leave a comment

in economic history, economics of media and culture, entrepreneurship, financial economics Tags: asset price bubbles, dot.com bubble, entrepreneurial alertness, Eugene Fama

The Rise and Rise of the Super Working Rich

15 May 2015 1 Comment

in economic history, entrepreneurship, financial economics, human capital, industrial organisation, labour economics, occupational choice, property rights, survivor principle, theory of the firm Tags: entrepreneurial alertness, Eugene Fama, Leftover Left, separation of ownership and control, super-rich, superstar wages, superstars, top 1%, Twitter left, working rich

The rise of the rentiers is nothing new. What is new is the degree of financial globalization and liberalization that has supercharged the fortunes of the super-wealthy even beyond robber baron levels. But it’s no mystery how to reverse this. It’s a matter of setting better rules for markets and taxing earners at the top a bit more.

In the course of a deranged rant against the entrepreneurs in society, the Atlantic collected an excellent set of information suggesting that the working rich have replaced rentiers as the super-rich. Rentiers are the idle rich. A rentier is a person or entity receiving income derived from patents, copyrights, interest, etc.

In The Evolution of Top Incomes: A Historical and International Perspective (NBER Working Paper No. 11955), Thomas Piketty and Emmanuel Saez concluded that:

While top income shares have remained fairly stable in Continental European countries or Japan over the past three decades, they have increased enormously in the United States and other English speaking countries.

This rise in top income shares is not due to the revival of top capital incomes, but rather to the very large increases in top wages (especially top executive compensation). As a consequence, top executives (the “working rich”) have replaced top capital owners at the top of the income hierarchy over the course of the twentieth century…

The Twitter Left claim that the surge in top compensation in the United States is attributable to an increased ability of top executives to set their own pay and to extract rents at the expense of shareholders. Obviously, from the chart below the pay the top 0.1% goes up and down with the share market. Top wages do not seem to have any independent power to dupe shareholders into overpaying them in bad times.

Xavier Gabaix and Augustin Landier found back in 2008 that what a major company’s CEO earns is directly proportional to the size of the firm that they are responsible for running. Executive compensation closely track the evolution of average firm value. During 2007 – 2009, firm value decreased by 17%, and CEO pay by 28%. During 2009-2011, firm value increased by 19% and CEO pay by 22%.

Xavier Gabaix and Augustin Landier also found that compensation for executives has risen with the market capitalization. From 1980 to 2003, the average value of the top 500 companies rose by a factor of six. Two commonly used indexes of chief executive compensation show close to a proportional six-fold matching increase.

Better executive decisions create more economic value. If the number of big companies is greater than the number of good chief executives, competitive bidding will push up executive pay to reflect the value of the talent that is available.

What happens to share prices when there is a surprise CEO resignation? Up or down? Apple went up and down in billions on news of Steve Jobs’ health.

When Hewlett Packard’s CEO Mark Hurd resigned unexpectedly, the value of HP stock dropped by about $10 billion! This makes his $30 million in annual compensation a bargain for shareholders. The fall in share price represents the difference between what the market expected from Hurd as Hewlett Packard’s CEO and what the market expects from his successor. Was Hurd under-paid?

There is an easy way to test for whether top executives cheat public shareholders. Compare the pay of large private companies, and public companies with a large or a few share holders, with public companies with diffuse share holdings. Private equity typically also pay its top executives very well, even though the capacity to dupe public shareholders are not a factor.

The burst of takeovers and leverage buyouts in the 1980s were very much driven by opportunities to profit from reducing corporate slack and downsizing flabby corporate headquarters of large publicly listed companies.

The response of the Left over Left of the day was support regulation to stop these mergers and takeovers rather than applauding them as giving lazy capitalists their comeuppance. This regulation undermined the market the corporate control rather than strengthened it as Michael Jensen explains:

This political activity is another example of special interests using the democratic political system to change the rules of the game to benefit themselves at the expense of society as a whole.

In this case, the special interests are top-level corporate managers and other groups who stand to lose from competition in the market for corporate control. The result will be a significant weakening of the corporation as an organizational form and a reduction in efficiency.

Central to the hypothesis of the Twitter Left of CEOs overpaying themselves is there is free cash within the business they pocket in pay rises, fringe benefits and lavished corporate headquarters rather than pay out in dividends or invest in profitable investments.

The interests and incentives of managers and shareholders frequently conflict over the optimal size of the firm and the payment of free cash to shareholders. What to pay the top executives is a minor manifestation of this common entrepreneurial difference of opinion the future of the business.

These conflicts in entrepreneurial judgements are severe in firms with large free cash flows–more cash than profitable investment opportunities. Jensen defines free cash flow as follows:

Free cash flow is cash flow in excess of that required to fund all of a firm’s projects that have positive net present values when discounted at the relevant cost of capital. Such free cash flow must be paid out to shareholders if the firm is to be efficient and to maximize value for shareholders.

Payment of cash to shareholders reduces the resources under managers’ control, thereby reducing managers’ power and potentially subjecting them to the monitoring by the capital markets that occurs when a firm must obtain new capital. Financing projects internally avoids this monitoring and the possibility that funds will be unavailable or available only at high explicit prices.

Michael Jensen developed a theory of mergers and takeovers based on free cash flows that explains:

- the benefits of debt in reducing agency costs of free cash flows,

- how debt can substitute for dividends,

- why diversification programs are more likely to generate losses than takeovers or expansion in the same line of business or liquidation-motivated takeovers,

- why bidders and some targets tend to perform abnormally well prior to takeover.

Michael Jensen noted that free cash flows allowed firms’ managers to finance projects earning low returns which, therefore, might not be funded by the equity or bond markets. Examining the US oil industry, which had earned substantial free cash flows in the 1970s and the early 1980s, he wrote that:

[the] 1984 cash flows of the ten largest oil companies were $48.5 billion, 28 percent of the total cash flows of the top 200 firms in Dun’s Business Month survey.

Consistent with the agency costs of free cash flow, management did not pay out the excess resources to shareholders. Instead, the industry continued to spend heavily on [exploration and development] activity even though average returns were below the cost of capital.

Jensen also noted a negative correlation between exploration announcements and the market valuation of these firms—the opposite effect to research announcements in other industries. Not surprisingly, after a successful corporate takeover, there is major changes to realise the untapped benefits they saw in the company that the incumbent management were not seizing capturing:

Corporate control transactions and the restructurings that often accompany them can be wrenching events in the lives of those linked to the involved organizations: the managers, employees, suppliers, customers and residents of surrounding communities.

Restructurings usually involve major organizational change (such as shifts in corporate strategy) to meet new competition or market conditions, increased use of debt, and a flurry of recontracting with managers, employees, suppliers and customers.

All modern theories of the focus in part or in full on reducing opportunistic behaviour, cheating and fraud in employment and commercial relationships. The market the corporate control, and mergers and takeovers realise large benefits from displacing underperforming manager teams. Premiums in hostile takeover offers historically exceed 30 percent on average. Acquiring-firm shareholders on average earn about 4 percent in hostile takeovers and roughly zero in mergers.

In terms of corporate control, Eugene Fama divides firms into two types: the managerial firm, and the entrepreneurial firm.

The entrepreneurial firms are owned and managed by the same people (Fama and Jensen 1983b). Mediocre personnel policies and sub-standard staff retention practices within entrepreneurial firms are disciplined by these errors in judgement by owner-managers feeding straight back into the returns on the capital that these owner-managers themselves invested. Owner-managers can learn quickly and can act faster in response the discovery of errors in judgement. The drawback of entrepreneurial firms is not every investor wants to be hands-on even if they had the skills and nor do they want to risk being undiversified.

The owners of a managerial firm advance, withdraw, and redeploy capital, carry the residual investment risks of ownership and have the ultimate decision making rights over the fate of the firm (Klein 1999; Foss and Lien 2010; Fama 1980; Fama and Jensen 1983a, 1983b; Jensen and Meckling 1976).

Owners of a managerial firm, by definition, will delegate control to expert managerial employees appointed by boards of directors elected by the shareholders (Fama and Jensen 1983a, 1983b). The owners of a managerial firm will incur costs in observing with considerable imprecision the actual efforts, due diligence, true motives and entrepreneurial shrewdness of the managers and directors they hired (Jensen and Meckling 1976; Fama and Jensen 1983b).

Owners need to uncover whether a substandard performance is due to mismanagement, high costs, paying the employees too much or paying too little, excessive staff turnover, inferior products, or random factors beyond the control of their managers (Jensen and Meckling 1976; Fama and Jensen 1983b, 1985).

Many of the shareholders in managerial firms have too small a stake to gain from monitoring managerial effort, employee performance, capital budgets, the control of costs and the stinginess or generosity of wage and employment policies (Manne 1965; Fama 1980; Fama and Jensen 1983a, 1983b; Williamson 1985; Jensen and Meckling 1976). This lack of interest by small and diversified investors does not undo the status of the firm as a competitive investment nor introduce slack in the monitoring of payments to top executives.

Large firms are run by managers hired by diversified owners because this outcome is the most profitable form of organisation to raise capital and then find the managerial talent to put this pool of capital to its most profitable uses (Fama and Jensen 1983a, 1983b, 1985; Demsetz and Lehn 1985; Alchian and Woodward 1987, 1988).

More active investors will hesitate to invest in large managerial firms whose governance structures tolerate excessive corporate waste and do not address managerial slack and and overpaid executives. Financial entrepreneurs will win risk-free profits from being alert and being first to buy or sell shares in the better or worse governed firms that come to their notice.

The risks to dividends and capital because of manifestations of corporate waste, reduced employee effort, and managerial slack and aggrandisement in large managerial firms are risks that are well known to investors (Jensen and Meckling 1976; Fama and Jenson 1983b). Corporate waste and managerial slack also increase the chances of a decline in sales and even business failure because of product market competition (Fama 1980; Fama and Jensen 1983b).

Investors will expect an offsetting risk premium before they buy shares in more ill-governed managerial firms. This is because without this top-up on dividends, they can invest in plenty of other options that foretell a higher risk-adjusted rate of return. The discovery of monitoring or incentive systems that induce managers to act in the best interest of shareholders are entrepreneurial opportunities for pure profit (Fama and Jensen 1983b, 1985; Alchian and Woodward 1987, 1988; Demsetz 1983, 1986; Demsetz and Lehn 1985; Demsetz and Villalonga 2001).

Investors will not entrust their funds to who are virtual strangers unless they expect to profit from a specialisation and a division of labour between asset management and managerial talent and in capital supply and residual risk bearing (Fama 1980; Fama and Jensen 1983a, 1983b; Demsetz and Lehn 1985). There are other investment formats that offer more predictable, more certain rate of returns.

Competition from other firms will force the evolution of devices within the firms that survive for the efficient monitoring the performance of the entire team of employees and of individual members of those teams as well as managers (Fama 1980, Fama and Jensen 1983a, 1983b; Demsetz and Lehn 1985). These management controls must proxy as cost-effectively as they can having an owner-manager on the spot to balance the risks and rewards of innovating.

The reward for forming a well-disciplined managerial firm despite the drawbacks of diffuse ownership is the ability to raise large amounts in equity capital from investors seeking diversification and limited liability (Demsetz 1967; Jensen and Meckling 1976; Fama 1980; Fama and Jensen 1983b; Demsetz and Lehn 1985). Portfolio investors may know little about each other and only so much about the firm because diversification and limited liability makes this knowledge less important (Demsetz 1967; Jensen and Meckling 1976; Alchian and Woodward 1987, 1988).

It is unwise to suppose that portfolio investors will keep relinquishing control over part of their capital to virtual strangers who do not manage the resources entrusted to them in the best interests of the shareholders (Demsetz 1967; Williamson 1985; Fama 1980, 1983b; Alchian and Woodward 1987, 1988).

Managerial firms who are not alert enough to develop cost effective solutions to incentive conflicts and misalignments will not grow to displace rival forms of corporate organisation and methods of raising equity capital and loans, allocating legal liability, diversifying risk, organising production, replacing less able management teams, and monitoring and rewarding employees (Fama and Jensen 1983a, 1983b; Fama 1980; Alchian 1950).

Entrepreneurs will win profits from creating corporate governance structures that can credibly assure current and future investors that their interests are protected and their shares are likely to prosper (Fama 1980; Fama and Jensen 1983a, 1983b, 1985; Demsetz 1986; Demsetz and Lehn 1985). Corporate governance is the set of control devices that are developed in response to conflicts of interest in a firm (Fama and Jensen 1983b).

At bottom, the private sector is highly successful designing forms of organisation that allow large sums of money, billions of dollars to be raised in the capital market and entrusted to management teams.

via The Rise and Rise of the Super-Rich – The Atlantic and How the Richest 400 People in America Got So Rich – The Atlantic.

Eugene Fama on it’s difficult, if not impossible, to distinguish luck from skill

24 Feb 2015 Leave a comment

A firm with no employees is not a firm

16 Feb 2015 Leave a comment

in econometerics, politics - USA, theory of the firm Tags: Armen Alchian, Eugene Fama, Harold Demsetz, Ronald Coase, Yoram Barzel

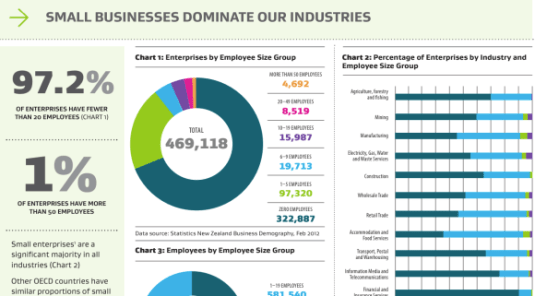

Business demographic statistics in New Zealand include companies with zero employees and calls them a firm.

Source: Statistics New Zealand.

Every definition of a firm that I have seen refers to a firm as a relationship between employers, employees and others. There is team production or some sort of nexus of contracts or dependent assets, something social.

The notion is that transactions that normally take place in the market are taken out of the market and take place within the firm. Most profoundly, as Ronald Coase explained in 1937 in his seminal work The Nature of the Firm is what needs to be explained is the existence of the firm, with its

distinguishing mark … [of] the supersession of the price mechanism.

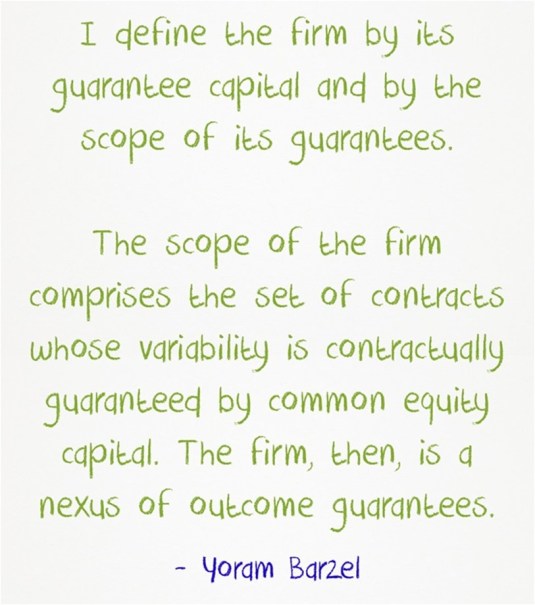

If there’s only one person in the firm, there is no one to transact with within the firm that the parties would normally have otherwise done in the market at arm’s length. There is no suppression of the price system, because all the dealings of the one person firm is with others. There are no transactions outside of the price system. As Barzel and Kochin explain when contrasting Ronald Coase’s theory of the firm with that of Alchian and Demsetz:

Even though they offer an alternative to Coase’s theory of the firm, their firm, nevertheless, is fundamentally a transaction cost phenomenon – it arises in response to the costs associated with measuring and policing various inputs and outputs.

Doug Allen, along with Eugene Fama, argue that all economic organisations are designed to maximise the gains from trade net of transaction costs. Other forms of organisation, forms of organisation that do not maximise the gains from trade net of transaction costs as well would not survive in market competition.

Transaction costs are defined by Allen as the costs of establishing and maintaining property rights. Yoram Barzel defines (economic) property rights (in this paper, p. 394) as:

… an individual’s net valuation, in expected terms, of the ability to directly consume the services of the asset, or to consume it indirectly through exchange. A key word is ability: The definition is concerned not with what people are legally entitled to do but with what they believe they can do.

A property right, according to Alchian (1965, 1987) and Cheung (1969), is essentially the ability to enjoy a piece of property, but this ability to benefit from an asset or commodity, either directly, or indirectly through market exchange, is seldom unhindered. Eugene Fama observed that:

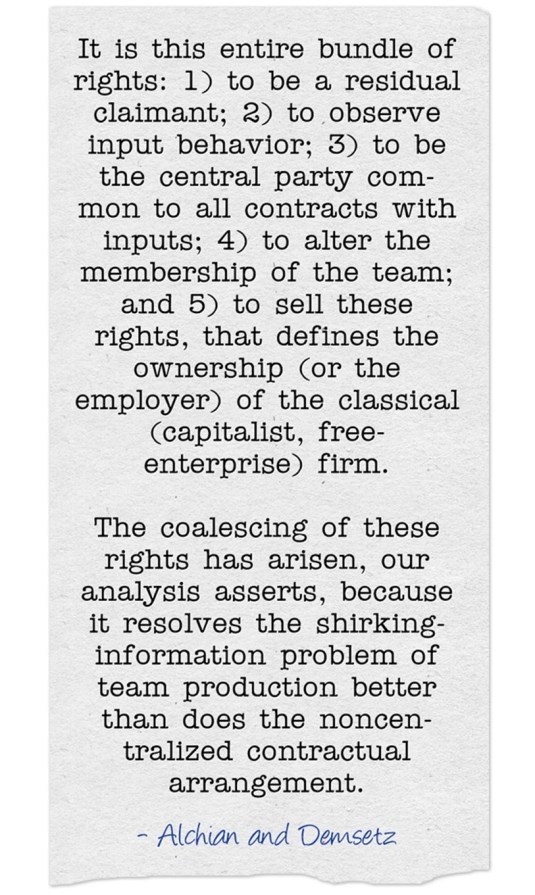

The striking insight of Alchian and Demsetz (1972) and Jensen and Meckling (1976) is in viewing the firm as a set of contracts among factors of production. In effect, the firm is viewed as a team whose members act from self-interest but realize that their destinies depend to some extent on the survival of the team in its competition with other teams.

If the firm consists only of the owner, there is no internal constraints on the establishment and maintenance of property rights because no one else is in the firm to cause any conflict. There is no nexus of contracts between different suppliers of production inputs whose destinies depend on the ability of them as a team to survive in competition with other teams.

Whatever constraints might arise about the ability of the owner to actually exercise property rights, none of these constraints arise internally to the firm because of the presence of employees or partners.

If there are no employees, if the firm only consist of the owner, the purpose of the firm, which is to make the incentives of workers compatible with those of owners is lost.

Firms, to be a firm, must have employees. If not employees, there must be at least more than one party involved, such as in a partnership.

Firms exist because it is cheaper to organize inputs within a firm than buy and sell in many different markets. This buying and selling requires a continual negotiation, renegotiation, enforcement and monitoring of contracts at arm’s length with independent suppliers of inputs. Barzel stressed this enforcement of property rights in an unpublished paper:

I hypothesize that the firm is organized for the express purpose of creating rights that are more economically enforced by non-state rather than by state means.

Many of these firms with zero employees in the New Zealand business demographic statistics, a classification that accounts for over 60% of all firms in New Zealand, are shelf companies or property investment companies.

There is no measuring and policing of inputs and outputs in a firm that has no employees and only an owner. These entities are not firms. They meet none of the criteria for a firm in the economics of industrial organisation.

This failure to distinguish between a firm and other forms of organisation leads the Minister of Economic Development to say unfortunate things such as:

97 per cent of enterprises in New Zealand are small businesses and have fewer than 20 employees.

Two thirds of that 97% of enterprises has no employees. Any discussion that pretends to know that there are too many or too few small and large firms in New Zealand should not be confused with other forms of organisation of capital that have nothing to do with the topic at hand, which is usually workplace productivity and entrepreneurial competence.

Many of these zero employee firms are not even economic organisations. They are legal mechanisms for exercising legal property rights. Including these property rights in business demographic statistics on business organisations is confusing.

Eugene Fama and the simulative effects of fiscal policy

31 Jul 2014 6 Comments

in budget deficits, fiscal policy, great depression, great recession, macroeconomics Tags: crowding out, Eugene Fama, fiscal policy, Treasury view of fiscal policy

Eugene Fama argues that government bailouts and stimulus plans seem attractive when there are idle resources – when there is unemployment such as in a recession or depression including in the 1930s.

Fama counters that:

1. Bailouts and stimulus plans must be financed.

2. If the financing takes the form of additional government debt, the added debt displaces other uses of the funds.

3. Thus, stimulus plans only enhance incomes when they move resources from less productive to more productive uses.

In the end, despite the existence of idle resources, bailouts and stimulus plans do not add to current resources in use. They just move resources from one use to another.

Fama noted that there was just one valid negative comment in response to this argument that appears to be valid which was made by Brad DeLong.

Fama thinks Delong’s point about involuntary inventory accumulation is consistent with Fama’s initial arguments about the need for the stimulus to work through moving resources to higher value uses.

For me, the notion that a fiscal stimulus is a negative productivity shock is a good starting point for analysis. The method of financing the stimulus is important too.

Economic agents know that a temporary expenditure program has no lasting effect on employment but has lasting effect on disposable income and taxes. Indeed, massive public interventions to maintain employment and investment during a financial crisis can, if they distort incentives enough, lead to a depression.

In Australia, there was a massive fiscal contraction from late 1930 onwards called the Premiers’ Plan. In 1931, unemployment rates was 25% or more.

- The Premiers’ Plan required the federal and state governments to cut spending by 20%, including cuts to wages and pensions and was to be accompanied by tax increases, reductions in interest on bank deposits and a 22.5% reduction in the interest the government paid on internal loans.

- The Premiers’ Plan was complementary to the Arbitration Court’s 10 per cent nominal wage cut in January 1931 and the devaluation of the Australian pound. Most countries had abandoned the gold standard by 1931 and 1932 and devalued by about 10% including the UK. These competitive devaluations were called currency wars. Most countries below started to recovery before they left the gold standard, a year or two before they left the cross of gold.

Maclaren (1936) dated the Australian economic recovery from the last months of 1932. It was to take another three years before unemployment rates fell below 10 per cent — the rate it had been during most of the 1920s.

The June 1931 Premiers’ Plan of fiscal consolidation had time by late 1932 to become credible and take hold given the usual leads and lag on fiscal policy. Unemployment data for the time show a rapid fall in the high twenties unemployment rate in 1932 to be below 10 per cent by 1937.

Eugene Fama on share market bubbles

03 Jul 2014 Leave a comment

in economics, entrepreneurship, financial economics Tags: efficient markets hypothesis, Eugene Fama

Q: I guess most people would define a bubble as an extended period during which asset prices depart quite significantly from economic fundamentals.

A: That’s what I would think it is, but that means that somebody must have made a lot of money betting on that, if you could identify it. It’s easy to say prices went down, it must have been a bubble, after the fact.

I think most bubbles are twenty-twenty hindsight. Now after the fact you always find people who said before the fact that prices are too high.

People are always saying that prices are too high. When they turn out to be right, we anoint them. When they turn out to be wrong, we ignore them.

They are typically right and wrong about half the time…

I want people to use the term in a consistent way. For example, I didn’t renew my subscription to The Economist because they use the world bubble three times on every page. Any time prices went up and down—I guess that is what they call a bubble. People have become entirely sloppy.

People have jumped on the bandwagon of blaming financial markets. I can tell a story very easily in which the financial markets were a casualty of the recession, not a cause of it.

Does a fiscal stimulus stimulate?

26 Jun 2014 Leave a comment

in applied price theory, budget deficits, business cycles, fiscal policy, macroeconomics Tags: Eugene Fama

Warren Buffett and other business owners

17 Mar 2014 Leave a comment

in entrepreneurship, market efficiency Tags: efficient markets hypothesis, Eugene Fama, Kerry Packer, luck versus skill, Rupert Murdoch, Warren Buffett

The father of the efficient markets hypothesis and a champion of the passive investment index-linked funds Eugene Fama considers Buffett to be more of a businessman than a portfolio investor. To Fama, the high returns by Buffett look great because entrepreneurs that do survive in market competition look good because we ignore the thousands that failed and lost everything.

You should compare Buffett with other businessmen such as Kerry Packer and Rupert Murdoch. These two Australian corporate giants started off with two TV stations and a rather ordinary afternoon newspaper, respectively.

Packer and Murdoch grew their businesses to a global level to move from being millionaires to billionaires. Bill Gates and Steve Jobs also built and ran big companies from scratch.

Packer, Murdoch, Gates and Jobs all had great returns because they were able to obtain a return of their unique management skills and entrepreneurial alertness.

Kaplan and Rauh in “It’s the Market: The Broad-Based Rise in the Return to Top Talent” Journal of Economic Perspectives 2013 found that most of those in the Forbes 400 did not grow up wealthy.

Most of the Forbes 400 are entrepreneurs who accessed education while young and then applied their skills to the technology, finance, and mass retail sectors. In these sectors, through ICT and other innovations, these entrepreneurs could apply their superior talents to larger and larger pools of resources and more and more firms to reach huge numbers of consumers on a national or global scale. They became superstars in terms of their productivity and pay because they could lever their talents so widely over so many firms, workers, consumers and countries.

But remember, hundreds of dot.com firms failed and lost everything for each one that made it big. These are businesses we remember. The dot.com firms that failed are quiz questions, if they are remembered at all.

What is left standing after all this blood letting must be extremely profitable if only to justify the ride for those that risked it all to have it all. Fama estimated that the dot.com bubble was justified if something like 1.4 more Microsofts were born as a result of it!

Frazzini, Kabiller and Pedersen in “Buffett’s Alpha” found that Buffet had “a higher Sharpe ratio than any stock or mutual fund with a history of more than 30 years”. The Sharpe Ratio describes how much excess return you are receiving for the extra volatility in your portfolio because your are holding a riskier asset

Buffett is a volatile investment as Frazzini, Kabiller and Pedersen noted: from July 1998 through February 2000, Berkshire lost 44% of its market value, while the overall share market gained 32%.

A key to Buffett’s success was Berkshire surviving these set-backs.

Both Packer and Murdoch too had a few lucky scraps with their bankers. Steven Jobs was fired by Apple in 1985 because he was no good as a CEO – he was sending the company broke and would not listen. Bill Gates is as good as his next product launch. Nokia shares initially fell by 90% in 2007 when Apple leap-frogged it with a phone that resembled a PC – the iPhone.

Buffett and Murdoch both run an internal capital market where they expect a certain minimum rate of return.

Both are hands-off. Buffett’s corporate head office has 24 employees to do the regulatory and compliance work.

Murdoch reputedly rings the chief executive of each of his companies once a month for one minute. If what the chief executive says is interesting, the call gets longer. This is the essence of entrepreneurial alertness. Noticing what others have not and grasping that opportunity before someone else beats you to it.

Recent Comments