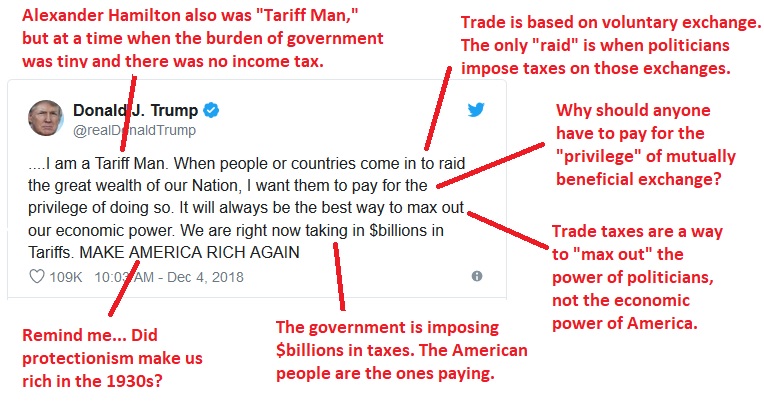

Donald Trump, who describes himself as “Tariff Man,” recently wrote a column in defense of his protectionist trade policy for the Wall Street Journal. After reading the column, my first thought was that Trump was trying to show he is more economically illiterate than Joe Biden (a big challenge, as seen here and here). And […]

By Paul Homewood h/t Ian Cunningham Heat pumps were supposed to coming down in price, we were told. Instead the opposite has occurred. The Telegraph report: “The cost of fitting a heat pump has risen by a third in six years despite generous government grants – leading critics to accuse installers […]

Notably, oil produced in the Gulf of Mexico is less carbon-intensive than oil produced elsewhere; one May 2023 analysis commissioned by the National Ocean Industries Association (NOIA) found that oil extracted offshore in the Gulf of Mexico is 46% less carbon-intensive than the global average excluding the U.S. and Canada.

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

Recent Comments