Business Cycles – Edward C. Prescott

25 Mar 2017 Leave a comment

in business cycles, development economics, economic growth, economic history, financial economics, fiscal policy, macroeconomics Tags: Edward Prescott, real business cycles

@garethmorgannz’s #UBI finishes the job on #GenerationRent @JordNZ

29 Mar 2016 Leave a comment

in fiscal policy, labour economics, labour supply, macroeconomics, politics - New Zealand, population economics, poverty and inequality Tags: Edward Prescott, New Zealand superannuation, old age pensions, social insurance, timing inconsistency, universal basic income, welfare state

Gareth Morgan revealed today a hitherto unnoticed design feature in his Universal Basic Income of $11,000 per annum. It will be phased in over a long time. That will mean that Generation Rent will continue to pay taxes to fund a universal old age pension for their parents and grandparents, but will not be fortunate enough to receive that themselves.

Source: Morgan Foundation (2016) Taxpayers Union Critique of the UBI just bonkers – again

They are not left of their own devices. Generation Rent is expected to save the Universal Basic Income they receive over their working lives to avoid living in poverty in their retirement. Does not strike me as a political winner.

The Morgan Foundation does not understand the implications of time inconsistency for retirement savings policy:

- Which is better? Save for your retirement through the share market or save to own your own home and then present yourself at the local social security office to collect your taxpayer funded old-age pension?

- Under this fine game of bluff, you bleed the taxpayer in your old age and pass on your debt-free home to your children.

This strategy of not saving much for retirement is rational for the less well-paid. The family home is exempt from income and asset testing for social security. If you lose you bet, sell your house and live off the capital. For ordinary workers, this is a good bet. The middle class might prefer to live in a more luxurious retirement.

For ordinary workers, whose wages are not a lot more than their old age pension from the government, a government funded pension is a good political gamble. The old-age pension for a couple in New Zealand is set at no less that 60% of average earnings.

Edward Prescott argues for compulsory retirement savings account albeit with important twists because it is otherwise irrational for many to save for their retirement against the background of a welfare state:

The reason we need to have mandatory retirement accounts is not because people are irrational, but precisely because they are perfectly rational — they know exactly what they are doing.

If, for example, somebody knows that they will be cared for in old age — even if they don’t save a nickel — then what is their incentive to save that nickel? Wouldn’t it be rational to spend that nickel instead?

…Without mandatory savings accounts we will not solve the time-inconsistency problem of people under-saving and becoming a welfare burden on their families and on the taxpayers. That’s exactly where we are now.

Current State of World Economic Development by Ed Prescott (8 December 2015)

17 Dec 2015 Leave a comment

in development economics, economic growth, macroeconomics Tags: Edward Prescott

Recurrent business cycles without shocks – the role of lumpy investments

11 Aug 2015 Leave a comment

in business cycles, economic growth, Edward Prescott, entrepreneurship, financial economics, fiscal policy, industrial organisation, macroeconomics, Milton Friedman, monetarism, monetary economics Tags: Edward Prescott, mega sports events, mega-projects, Mexico, Norway, prosperity and depression, R&D, real business cycles, Richard Rogerson, Robert Barro, technology diffusion lags

Think it is time for a re-post of @LHSummers' brilliant, brilliant paper on RBC from 1986. minneapolisfed.org/research/qr/qr… http://t.co/S7tGIjEebI—

Simon H (@simonhinrichsen) August 10, 2015

The brilliant monetary economist Scott Freeman was one of the 1st to show the existence of real business cycles without the need of shocks to drive the ups and downs of the economy. He did this when taking time off from showing that much of the apparent correlation between the nominal and the real side of the economy is due to the endogenous response of money created by banks to fluctuations in real activity.

In 1999, Scott Freeman co-wrote Endogenous Cycles and Growth with Indivisible Technological Developments. The paper was about large, discrete technological improvements that required the accumulation of research or infrastructural investment over time before any benefits for realised in terms of increased output. With these lead-times for research or infrastructure investments, growth paths display cyclical patterns even in the absence of any shocks.

This lumpiness over time implied that a costly process such as research or construction must be completed on a large scale before the greatest part of a project’s benefits in output can be realized as Freeman and co. argue:

There are numerous examples of big research or infrastructural projects that are characterized by huge investments and relatively long development periods, where most of the benefits occur only after the project is complete.

Freeman and his co-authors gave as examples space research and satellite programs and major medical research. These are examples of prolonged and costly R & D whose benefits come primarily at the conclusion of the project.

Lags in the development of a new drug between the commencement of the R&D project and any revenues received is routinely now more than a decade. The Human Genome Project seems to be going on without end with few initial benefits.

Infrastructural examples given by Freeman and his co-authors included the installation of telephone, the internet, transportation shipping canals, interregional highways, railroads, mass transit or electricity transmission projects. All of these projects with long lead times, once completed that may increase the productivity of many economic sectors in addition to increasing output in the area concerned. In many cases there are no benefits whatsoever of the project and to after it is completed many years in the future. Oil pipelines can take up to a decade to build.

The 1973 oil price crisis launched a research and development program into alternative sources of energy and alternative sources of oil and gas supply that has lasted to this day.

Classic further examples of long lead times are mega sports events such as the World Cup and Olympic Games. Years of planning, development and construction for any benefits or revenues are obtained.

What is important in terms of the random shocks that drive the business cycle as championed by Ed Prescott is there are a range of sectors within the economy where there are long lead times before the investment leads to any outputs. Not surprisingly the first article in the real business cycle literature included in its title “time to build“.

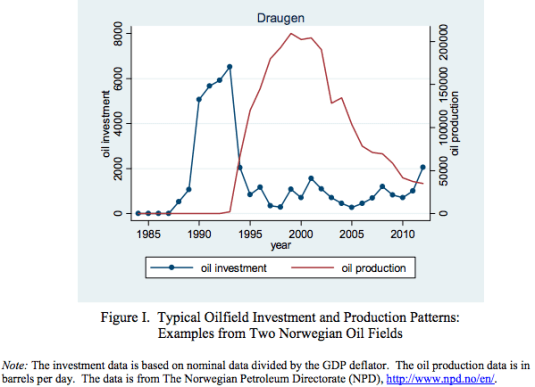

Rabah Arezki, Valerie Ramey, and Liugang Sheng in “News Shocks in Open Economies: Evidence from Giant Oil Discoveries” explore a related theme of real business cycles without shocks. In particular, they investigate news of productivity enhancements. They look at what happens to economies that discover oil. An oil discovery is a well identified “news shock.”

An oil discovery is well publicised and creates an incentive to invest in oil drilling. More importantly, there is news of greater income in the future but no change in current labour productivity or technological opportunities.

Rabah,Valerie, and Liugang found that after big oil discoveries, during the period of investment, the newly rich oil country borrows from abroad to build oil wells, oil pipelines and associated port infrastructure, obviously, but also borrows to finance higher consumption now. Consumption goes up and stays up in permanent income hypothesis fashion.

Interestingly, employment declines because of the wealth effect from the future income but there is no higher productivity of labour to encourage more work today. Investment rises soon after the news of the oil discovery arrives, while GDP does not increase for 5 years or more.

This is consistent with experience in the oil-rich Arab countries where there was increased consumption of leisure in anticipation of high future income is based on oil.

The same happened in Norway where massive investment was funded by foreign borrowing that led to annual current account deficits of up to 15% of GDP. Domestic savings fell away because Norwegians anticipated higher future incomes and started spending some of it now as predicted by the permanent income hypothesis. Norway now has a huge sovereign wealth fund able to fund a large part of its demographic burden from an ageing society.

After Mexico’s discovery of oil in the early 1970s, investment was high in oil and related industries. Consumption—by households and government—rose because of the increase in prospective real income. Since real GDP was not yet high, Mexico borrowed to pay for both the oil investment and the higher current consumption. Mexico’s foreign debt increased from $3.5 billion or 9% of GDP in 1971 to $61 billion or 26% of GDP in 1981. This boom in consumption and investment occurred without any productivity shock. All that was required was the ability to borrow.

Once the oil comes on line, the economy concern exports oil and pays back debt. This is when GDP including oil production finally rises a good five years and often more after the oil discovery. Consumption continues for its previous high rates while investment falls as the oil wells and pipelines have been built.

As with Scott Freeman, the long lead times not only can lead to large swings in investment, lumpy investments can also lead to increases in consumption, savings and employment without any productivity shocks.

Keynesian macroeconomics postulated that the economy slips into recessions for all sorts of reasons such as shifts and turns in the animal spirits and a loss of consumer confidence leading to a fall in autonomous investment and autonomous consumption. A collapse in autonomous investment and autonomous consumption is the Keynesian explanation for the great depression.

Both Keynesian macroeconomics and real business cycle theories at least at the outset couldn’t explain why there were recessions. Both attributed to them to causes they were yet to explain.

Keynesian macroeconomics could not explain what drove the waves of optimism and pessimism that either sharply increased or reduced investment. At bottom, Keynesian macroeconomics makes an unjustified assumption that technological progress unfolds at a relatively smooth rate and it attributes volatility in the economy to fluctuations in investment unrelated to trends in productivity.

The key inside of Keynesian macroeconomics was that inflation and unemployment were inversely correlated, so as one went up, the other went down as Milton Friedman explains.

Marvellously simple. A key that apparently unlocks the mystery of long-continued unemployment: inadequate autonomous spending or too low a propensity to consume. Increase either, or both, being careful simply not to go too far, and full employment could be attained.

What a wonderful prescription: for consumers, spend more out of your income, and your income will rise; for governments, spend more, and aggregate income will rise by a multiple of your additional spending; tax less, and consumers will spend more with the same result.

Though Keynes himself, and even more, his disciples, produced much more sophisticated and subtle versions of the theory, this simple version contains the essence of its great appeal to non-economists and especially governments.

A well-functioning economy should have no business cycles – no bouts of high inflation or persistent unemployment as Richard Rogerson explained:

So if there are cycles, that’s an indication of a malfunctioning economy. That idea permeated thinking for many years and was deeply ingrained. In effect, if an economy is in recession, someone should fix it.

The Keynesians only retreated as their empirical predictions were thoroughly discredited in the 1970s stagflation. Ad hoc auxiliary hypotheses were included about the supply-side in the Keynesian paradigm to prop up the old-time religion, not find new paths as Robert Barro put it:

At least Prescott and other real business cycle theorists accepted that they must eventually unpack productivity drops and name causes that can be explored further to be found persuasive or perhaps wanting. They argued that periods of temporarily low output growth need not be market failures, but could follow from temporarily slow improvements in production technologies.

As research progressed, real business cycles were viewed as recurrent fluctuations in an economy’s incomes, products, and factor inputs—especially labour—due to changes in technology, tax rates and government spending, tastes, government regulation, terms of trade, and energy prices.

Scott Freeman took this research further. He, his colleagues and his progeny showed that real business cycles can occur without any productivity rises and falls whatsoever. All that was needed was the ability to borrow and invest across time to finance lumpy investments. These lumpy investments can be anything from oil wells, dams to new drugs, anywhere involving time to build and capital accumulation:

HT: The Grumpy Economist: Arezki, Ramey, and Sheng on news shocks.

Annual hours worked per working age American, German and French, 1950–2013

12 May 2015 Leave a comment

in applied price theory, economic growth, economic history, great depression, labour economics, labour supply, macroeconomics, politics - USA, Public Choice, public economics, taxation Tags: Edward Prescott, Euroclerosis, France, Germany, labour supply, Robert Lucas, taxation and labour supply

Figure 1 shows that Americans work the same hours per year pretty much the entire post-war period. By contrast, there is been a long decline in hours worked in Germany and France. The large drop in 1992 was German unification.

Figure 1: annual hours worked per working age American, German and French, 1950 – 2013

Source: OECD StatExtract and The Conference Board Total Economy Database™,January 2014, http://www.conference-board.org/data/economydatabase/

The long decline seemed to tally with the disproportionately sharp rise in the average tax rate on labour income, including social security contributions in France and Germany. When tax rates on labour income, including social security contributions stabilised in about 1980, hours worked stabilised in all countries.

Figure 2: average tax rate on labour income,USA, Germany and France, 1950 – 2013

Source: Source: Cara McDaniel.

Some pander to the great vacation theory of European labour supply. This is the hypothesis of a large increase in the preference for leisure in the European Union member states. That is, mass voluntary unemployment and mass voluntary reductions and labour supply by choice by Europeans. They just decided to work less.

This is not the first outing for the great vacation theory of labour supply. In the late 1970s, Modigliani dismissed the new classical explanation of Lucas and Rapping (1969) of the U.S. great depression in which the 1930s unemployment was voluntary unemployment – the great depression was just a great vacation – with the following remarks:

Sargent (1976) has attempted to remedy this fatal flaw by hypothesizing that the persistent and large fluctuations in unemployment reflect merely corresponding swings in the natural rate itself.

In other words, what happened to the U.S. in the 1930’s was a severe attack of contagious laziness!

I can only say that, despite Sargent’s ingenuity, neither I nor, I expect most others at least of the non-Monetarist persuasion, are quite ready yet. to turn over the field of economic fluctuations to the social psychologist!

As Prescott has pointed out, the USA in the Great Depression and France since the 1970s both had 30% drops in hours worked per adult. That is why Prescott refers to France’s economy as depressed. The reason for the depressed state of the French (and German) economies is taxes, according to Prescott:

Virtually all of the large differences between U.S. labour supply and those of Germany and France are due to differences in tax systems.

Europeans face higher tax rates than Americans, and European tax rates have risen significantly over the past several decades.

Countries with high tax rates devote less time to market work, but more time to home activities, such as cooking and cleaning. The European services sector is much smaller than in the USA.

Time use studies find that lower hours of market work in Europe is entirely offset by higher hours of home production, implying that Europeans do not enjoy more leisure than Americans despite the widespread impression that they do. Europeans did not work less. They worked more on activities that were not taxed.

US post-war economic booms compared

22 Feb 2015 Leave a comment

in business cycles, economic growth, economic history, macroeconomics, politics - USA Tags: Edward Prescott

Source: Edward Prescott

Was the 1990s in the USA a boom period or business as usual?

15 Dec 2014 Leave a comment

Source: Edward Prescott

Abe’s snap election pays off with big win for LDP | The Japan Times

15 Dec 2014 Leave a comment

in economic growth, macroeconomics, politics, Public Choice Tags: Edward Prescott, Japan

the ruling bloc secured a two-thirds supermajority in the 475-seat House of Representatives, giving it the power to override the Upper House.

When I arrived in Japan in 1995, the LDP was out of power and written off.

The LDP were true stayers in politics. They managed to get back into power soon after the 1995 general election by forming a coalition with the Socialist party.

The Socialist party leader was initially the Prime Minister then he resigned later and was replaced by an LDP Prime Minister.

The grip on power of the LDP was consolidated by the great competence of the Koizumi administration.

Source: Edward Prescott

The LDP lost power again in about 2007 but regained power in the next election through the extreme incompetence of their opposition.

In the current election, the main opposition party were unable even to put up enough candidates to actually win a majority.

The key contribution of the main opposition parties in Japan was well stated when they last won an election in 2007. They have shown that they can actually win an election when the LDP performs poorly. That is an important discipline that may not have been there in the 1980s.

via Abe’s snap election pays off with big win for LDP | The Japan Times.

Operations Research and The Revolution in Aggregate Economics – Edward Prescott 2012

18 Nov 2014 Leave a comment

in applied welfare economics, business cycles, economic growth, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics Tags: Edward Prescott, real business cycle theory

The extension of recursive methods to dynamic equilibrium modelling spawned a revolution in aggregate economics.

This revolution has resulted in aggregate economics becoming, like physics, a hard science and not exercises in storytelling.

Operations research played a major role in the development of practical methods to model dynamic aggregate economic phenomena and to predict the consequences of policy regimes.

Subsequently recursive methods were used to develop a quantitative theory of aggregate fluctuations and other aggregate phenomena.

Edward C Prescott – Restoring U.S. Prosperity – Brazil, 10 May 2014

27 May 2014 Leave a comment

in Edward Prescott, great recession, macroeconomics Tags: Edward Prescott, great recession

The path to higher U.S. prosperity

12 May 2014 Leave a comment

in applied welfare economics, economic growth, Edward Prescott, great recession, labour economics, macroeconomics Tags: capital taxation, Edward Prescott, retirement savings, tax reform

Suppose the USA:

- Had mandatory savings for retirement

- Eliminated capital income taxes

- Broadened tax base and lowered the marginal tax rate

- Phased in reforms so all birth-year cohorts are made better off

- Left welfare programs and local public good shares the same

- Savings not part of taxable income, saving withdrawals part of taxable income – with these changes U.S. income tax would be a consumption tax

US Detrended GDP per Capita

Source: Edward Prescott and Ellen McGrattan 2013.

A Great Recession or dropping to a lower long-term growth path

03 May 2014 Leave a comment

in great recession, macroeconomics Tags: Edward Prescott, great recession, Robert Lucas

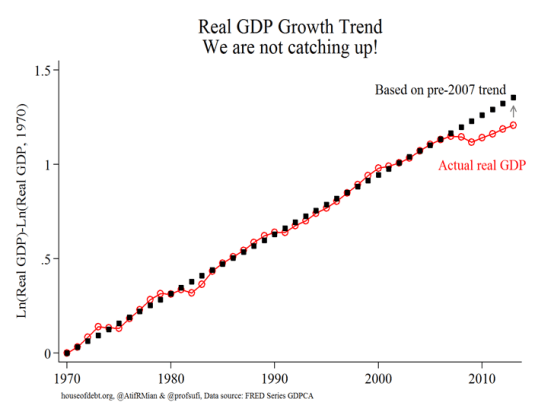

Ed Prescott and Robert Lucas are several of many who use variations of the chart below to show that the USA has moved to a lower long-term growth path.

Source: House of Debt

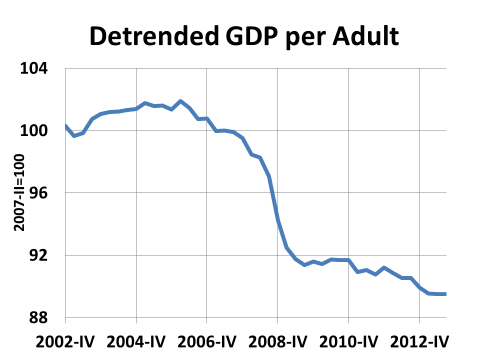

The chart below for output per working age American (ages 15 to 64) is just as depressing.

Source: Edward Prescott

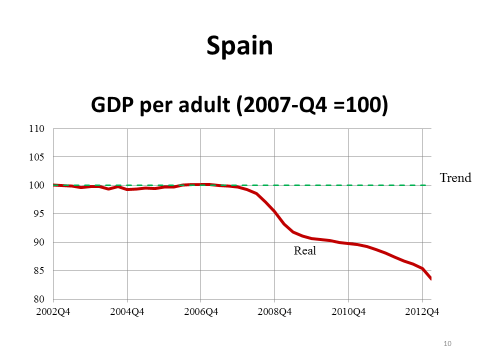

At least Spain with its 25% unemployment rate is doing a little worse.

Source: Edward Prescott

Many people are far too smart to save for their retirements

01 May 2014 Leave a comment

in applied welfare economics, macroeconomics Tags: Edward Prescott, fatal conceit, offsetting behavior, Other people are stupid fallacy, pretense to knowledge, retirement savings, time inconsistency

Which is better? Save for your retirement through the share market or save to own your own home and then present yourself at the local social security office to collect your taxpayer funded old-age pension?

Under this fine game of bluff, you bleed the taxpayer in your old age and pass on your debt-free home to your children.

This strategy is rational for the less well-paid. The family home is exempt from Income and asset testing for social security. If you lose you bet, sell your house and live off the capital.

For ordinary workers, this is a good bet. The middle class might prefer to live in a more luxurious retirement.

For ordinary workers, whose wages are not a lot more than their old age pension from the government, a government funded pension is a good political gamble. The old-age pension for a couple in New Zealand is set at no less that 60% of average earnings.

Compulsory savings for retirement requires the middle class to do what they can afford to do and would have done anyway.

Compulsory savings for retirement requires the working class to do what they can less afford to do.

Instead compulsory retirement savings deprives them of an old-age pension paid for by the taxes of the middle class.

In Australia, ordinary workers are required by law to save 9% of their wages for their retirements at 65 before they have had a chance to save for a car or a house or the rest of the condiments of life the middle class take for granted.

Edward Prescott argues for compulsory retirement savings account albeit with important twists because it is otherwise irrational for many to save for their retirement:

The reason we need to have mandatory retirement accounts is not because people are irrational, but precisely because they are perfectly rational — they know exactly what they are doing.

If, for example, somebody knows that they will be cared for in old age — even if they don’t save a nickel — then what is their incentive to save that nickel? Wouldn’t it be rational to spend that nickel instead?

…Without mandatory savings accounts we will not solve the time-inconsistency problem of people under-saving and becoming a welfare burden on their families and on the taxpayers. That’s exactly where we are now.

Prescott’s proposals are age specific. Those younger than 25 are not required to save anything because they are more pressing priorities such as buying cars and other consumer durables:

- Before age 25, workers would have no mandatory government retirement savings.

- Beginning at age 25, workers would contribute 3% vis-à-vis the current 10.6%.

- At age 30, that rate would increase to 5.3 percent.

- At 35, the rate would equal the full 10.6 percent.

- Upon retirement, there would be an annuity over the remaining lives of the individual and spouse

Most of all, the retirement savings must go into private savings accounts. These savings remain assets of the individual and therefore the compulsory savings requirements is not a tax and does not discourage labour supply, as Prescott explains:

Any system that taxes people when they are young and gives it back when they are old will have a negative impact on labour supply. People will simply work less.

Put another way: If people are in control of their own savings, and if their retirement is funded by savings rather than transfers, they will work more.

Prescott’s Nobel Prize jointly with Finn Kydland was for showing that policies are often plagued by problems of time inconsistency. They demonstrated that society could gain from prior commitment to economic policies.

Of course, as Tyler Cowen observed, forced savings schemes are easily offset by people rearranging their affairs, and they have their entire adult life to do so:

How much can our government force people to save in the first place?

You can make them lock up funds in an account, but they can respond by borrowing more on their credit cards, taking out a bigger mortgage, and in general investing less in their future.

People do not save for their retirements not because they are short-sighted, but because they are far-sighted. They know that governments will not carry out their threats and other big talk about not providing an adequate old-age pension.

The only way that governments can commit to not bailing people out who retire with no savings is to make them save for their own retirements over their working lives.

Some will be against this compulsion. Their opposition to compulsion cannot be based on opposition to the nanny state because that is faulty reasoning.

These opponents of compulsion and everyone else in the retirement income policy debate are playing in a far more complicated, decades long dynamic political game where ordinary people time and again out-smart conceited governments who pretend they know better:

The government has strategies.

The people have counter-strategies.

Ancient Chinese proverb

Robert Lucas and Edward Prescott discuss the future of economic growth, 2014

10 Apr 2014 Leave a comment

in economic growth, great recession, macroeconomics Tags: Edward Prescott, Robert E. Lucas

On 21 March, Robert E. Lucas Jr., and Edward C. Prescott participated in a roundtable on “The Wealth of Nations in the 21st Century” in Barcelona.

via Chong-En Bai, Robert Lucas, Edward Prescott discuss economic growth in Barcelona – Barcelona GSE.

Recent Comments