This week’s column for the Stuff papers covered the excellent new US work testing the effects of a UBI. From November 2020, 3000 low-income people were randomly assigned into two groups for three years. One thousand people each received $1000 per month in unconditional funds for three years. Two thousand people each received $50 per month.Both…

Basic income, again

Basic income, again

09 Aug 2024 Leave a comment

in applied price theory, econometerics, labour economics, labour supply, poverty and inequality, unemployment, welfare reform Tags: universal basic income

Zwolinski on the UBI

11 Jan 2024 Leave a comment

in applied price theory, history of economic thought, income redistribution, labour economics, labour supply, Public Choice, public economics, welfare reform Tags: negative income tax, universal basic income

Philosopher Matt Zwolinski, co-author of Universal Basic Income: What Everyone Needs to Know, was a core member of the old Bleeding Heart Libertarians blog, which shut down in 2020. Now’s he’s singledly-handed revived the BHL brand on his new Bleeding Heart Libertarian substack. Matt recently published a critique of my response to Chris Freiman on…

Zwolinski on the UBI

Who loses from Morgan’s #UBI of $11,000?

13 Aug 2017 Leave a comment

in labour economics, politics - New Zealand, poverty and inequality, public economics, welfare reform Tags: 2017 New Zealand election, universal basic income

Is a basic income a good idea? IEA

06 Jul 2017 Leave a comment

in applied price theory, applied welfare economics, labour economics, poverty and inequality Tags: UBI, universal basic income

Basic Income: Better Than Welfare?

06 May 2017 Leave a comment

in politics - New Zealand, politics - USA, welfare reform Tags: Bryan Caplan, universal basic income

The Big Kahuna and little kahuna for all to see

07 Mar 2017 Leave a comment

in fiscal policy, labour economics, politics - New Zealand, poverty and inequality, public economics Tags: social insurance, universal basic income, welfare state

Does abolishing bureaucracy save the #UBI? Avoid a great big new tax?

23 Jun 2016 Leave a comment

in applied welfare economics, income redistribution, politics - USA, poverty and inequality, public economics Tags: expressive voting, social insurance, universal basic income

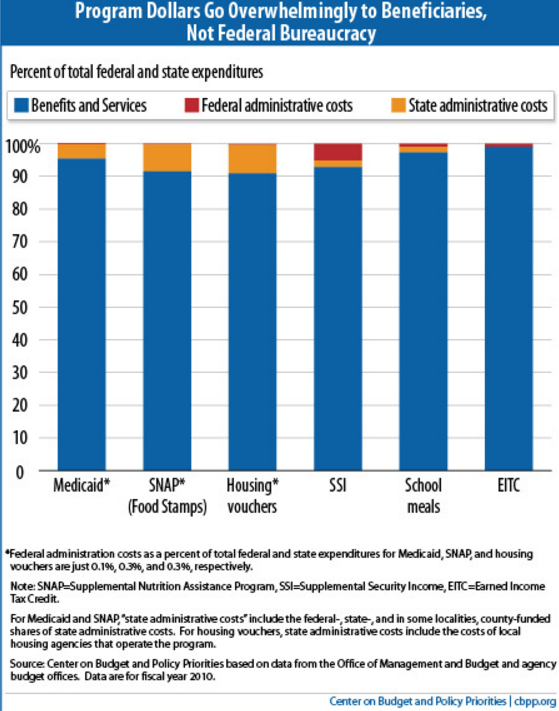

Firing the entire welfare state bureaucracy does not save the day for a universal basic income as Robert Greenstein explains

Suppose UBI provided everyone with $10,000 a year. That would cost more than $3 trillion a year — and $30 trillion to $40 trillion over ten years.

This single-year figure equals more than three-fourths of the entire yearly federal budget — and double the entire budget outside Social Security, Medicare, defense, and interest payments. It’s also equal to close to 100 percent of all tax revenue the federal government collects…

Where would the money to finance such a large expenditure come from? That it would come mainly or entirely from new taxes isn’t plausible.

We’ll already need substantial new revenues in the coming decades to help keep Social Security and Medicare solvent and avoid large benefit cuts in them. We’ll need further tax increases to help repair a crumbling infrastructure that will otherwise impede economic growth. And if we want to create more opportunity and reduce racial and other barriers and inequities, we’ll also need to raise new revenues to invest more in areas like pre-school education, child care, college affordability, and revitalizing segregated inner-city communities.

A UBI that’s financed primarily by tax increases would require the American people to accept a level of taxation that vastly exceeds anything in U.S. history. It’s hard to imagine that such a UBI would advance very far, especially given the tax increases we’ll already need for Social Security, Medicare, infrastructure, and other needs.

why no protests against #UBI bureaucratic job losses but #TPPANoWay protests aplenty about jobs?

08 Jun 2016 Leave a comment

in fiscal policy, labour economics, politics - Australia, politics - New Zealand, politics - USA, poverty and inequality, public economics Tags: expressive voting, growth of government, rational rationality, size of government, social insurance, universal basic income

The universal basic income is a rare bird for the left. It is the only time the usual suspects on the left are happy to cut government bureaucracy.

Furthermore, the left makes no inquiries as to how these redundant bureaucrats who administered the welfare state will find jobs. The market is left to work its magic for once. How convenient.

When a tariff cut is proposed, a trade deal signed, or job reduction in a bureaucracy suggested perhaps as the result of a privatisation, left-wing activists chain themselves to factory gates or government offices in solidarity. The social upheaval from the job losses among existing workers and their dim prospects of reemployment are paramount in their minds.

Why in the case of a universal basic income is the left so relaxed about job losses. Indeed, it celebrates as an advantage of a universal basic income that “Most of the bureaucracy of the welfare system [is] swept away” .

The universal basic income is the only time the left welcomes a reduction in bureaucracy and the role in the state. This switch from welfare payments to a universal basic income does not make those on the benefit any better off. Normally they are worse off under a universal basic income.

None of the the less well groups which of the concern of the left gain from a universal basic income. Despite this, they sell the jobs of their comrades in the public sector down the river.

I cannot believe the explanation is job losses are OK as long as they are the result of left-wing policies. Unless the labour market is liberalised, its ability to find new jobs for workers, for example, made redundant in the public sector after the introduction of a universal basic income is not any under greater than under a right-wing policy that costs jobs.

NZ #UBI can be only $4,700 @JordNZ @GrantRobertson1 @GeoffSimmonz

04 Jun 2016 Leave a comment

in labour economics, labour supply, politics - New Zealand, poverty and inequality Tags: expressive voting, growth of government, New Zealand Labor Party, rational irrationality, size of government, social insurance, universal basic income, welfare state

A universal basic income in New Zealand will have to be financed by a great big new tax because the existing ones are not enough according to the Economist calculations below.

HT: Paul Kerby.

Hayek (1976) on the need for a #UBI

26 May 2016 Leave a comment

in F.A. Hayek Tags: negative income tax, social insurance, universal basic income, welfare state

With friends like these, the #UBI will not live to face its enemies @jordNZ

09 May 2016 Leave a comment

in applied price theory, applied welfare economics, politics - New Zealand, politics - USA, public economics, rentseeking Tags: universal basic income

Running around saying that Universal Basic Income will make work optional leaves open the question of who will be the suckers who actually do the work and pay enormous taxes to fund the idyllic lifestyle of the bohemian rest.

Source: What If Everybody Didn’t Have to Work to Get Paid? – The Atlantic.

Recent Comments