Time to replace eagle with unicorn? The US as a high growth startup. @JimPethokoukis goo.gl/D4MK9x http://t.co/6WRB7nvUTp—

AEIdeas Blog (@AEIdeas) September 03, 2015

A history of US growth per capita

21 Sep 2015 Leave a comment

in economic growth, economic history, macroeconomics, politics - USA Tags: prosperity and depression

Recurrent business cycles without shocks – the role of lumpy investments

11 Aug 2015 Leave a comment

in business cycles, economic growth, Edward Prescott, entrepreneurship, financial economics, fiscal policy, industrial organisation, macroeconomics, Milton Friedman, monetarism, monetary economics Tags: Edward Prescott, mega sports events, mega-projects, Mexico, Norway, prosperity and depression, R&D, real business cycles, Richard Rogerson, Robert Barro, technology diffusion lags

Think it is time for a re-post of @LHSummers' brilliant, brilliant paper on RBC from 1986. minneapolisfed.org/research/qr/qr… http://t.co/S7tGIjEebI—

Simon H (@simonhinrichsen) August 10, 2015

The brilliant monetary economist Scott Freeman was one of the 1st to show the existence of real business cycles without the need of shocks to drive the ups and downs of the economy. He did this when taking time off from showing that much of the apparent correlation between the nominal and the real side of the economy is due to the endogenous response of money created by banks to fluctuations in real activity.

In 1999, Scott Freeman co-wrote Endogenous Cycles and Growth with Indivisible Technological Developments. The paper was about large, discrete technological improvements that required the accumulation of research or infrastructural investment over time before any benefits for realised in terms of increased output. With these lead-times for research or infrastructure investments, growth paths display cyclical patterns even in the absence of any shocks.

This lumpiness over time implied that a costly process such as research or construction must be completed on a large scale before the greatest part of a project’s benefits in output can be realized as Freeman and co. argue:

There are numerous examples of big research or infrastructural projects that are characterized by huge investments and relatively long development periods, where most of the benefits occur only after the project is complete.

Freeman and his co-authors gave as examples space research and satellite programs and major medical research. These are examples of prolonged and costly R & D whose benefits come primarily at the conclusion of the project.

Lags in the development of a new drug between the commencement of the R&D project and any revenues received is routinely now more than a decade. The Human Genome Project seems to be going on without end with few initial benefits.

Infrastructural examples given by Freeman and his co-authors included the installation of telephone, the internet, transportation shipping canals, interregional highways, railroads, mass transit or electricity transmission projects. All of these projects with long lead times, once completed that may increase the productivity of many economic sectors in addition to increasing output in the area concerned. In many cases there are no benefits whatsoever of the project and to after it is completed many years in the future. Oil pipelines can take up to a decade to build.

The 1973 oil price crisis launched a research and development program into alternative sources of energy and alternative sources of oil and gas supply that has lasted to this day.

Classic further examples of long lead times are mega sports events such as the World Cup and Olympic Games. Years of planning, development and construction for any benefits or revenues are obtained.

What is important in terms of the random shocks that drive the business cycle as championed by Ed Prescott is there are a range of sectors within the economy where there are long lead times before the investment leads to any outputs. Not surprisingly the first article in the real business cycle literature included in its title “time to build“.

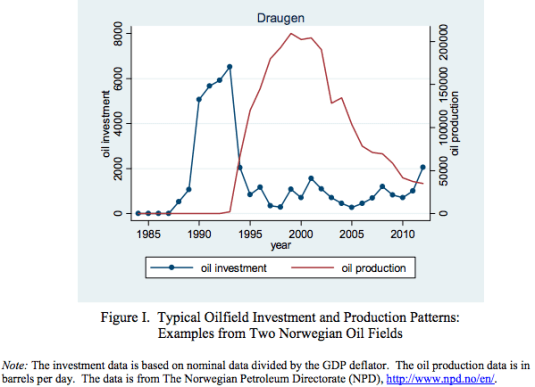

Rabah Arezki, Valerie Ramey, and Liugang Sheng in “News Shocks in Open Economies: Evidence from Giant Oil Discoveries” explore a related theme of real business cycles without shocks. In particular, they investigate news of productivity enhancements. They look at what happens to economies that discover oil. An oil discovery is a well identified “news shock.”

An oil discovery is well publicised and creates an incentive to invest in oil drilling. More importantly, there is news of greater income in the future but no change in current labour productivity or technological opportunities.

Rabah,Valerie, and Liugang found that after big oil discoveries, during the period of investment, the newly rich oil country borrows from abroad to build oil wells, oil pipelines and associated port infrastructure, obviously, but also borrows to finance higher consumption now. Consumption goes up and stays up in permanent income hypothesis fashion.

Interestingly, employment declines because of the wealth effect from the future income but there is no higher productivity of labour to encourage more work today. Investment rises soon after the news of the oil discovery arrives, while GDP does not increase for 5 years or more.

This is consistent with experience in the oil-rich Arab countries where there was increased consumption of leisure in anticipation of high future income is based on oil.

The same happened in Norway where massive investment was funded by foreign borrowing that led to annual current account deficits of up to 15% of GDP. Domestic savings fell away because Norwegians anticipated higher future incomes and started spending some of it now as predicted by the permanent income hypothesis. Norway now has a huge sovereign wealth fund able to fund a large part of its demographic burden from an ageing society.

After Mexico’s discovery of oil in the early 1970s, investment was high in oil and related industries. Consumption—by households and government—rose because of the increase in prospective real income. Since real GDP was not yet high, Mexico borrowed to pay for both the oil investment and the higher current consumption. Mexico’s foreign debt increased from $3.5 billion or 9% of GDP in 1971 to $61 billion or 26% of GDP in 1981. This boom in consumption and investment occurred without any productivity shock. All that was required was the ability to borrow.

Once the oil comes on line, the economy concern exports oil and pays back debt. This is when GDP including oil production finally rises a good five years and often more after the oil discovery. Consumption continues for its previous high rates while investment falls as the oil wells and pipelines have been built.

As with Scott Freeman, the long lead times not only can lead to large swings in investment, lumpy investments can also lead to increases in consumption, savings and employment without any productivity shocks.

Keynesian macroeconomics postulated that the economy slips into recessions for all sorts of reasons such as shifts and turns in the animal spirits and a loss of consumer confidence leading to a fall in autonomous investment and autonomous consumption. A collapse in autonomous investment and autonomous consumption is the Keynesian explanation for the great depression.

Both Keynesian macroeconomics and real business cycle theories at least at the outset couldn’t explain why there were recessions. Both attributed to them to causes they were yet to explain.

Keynesian macroeconomics could not explain what drove the waves of optimism and pessimism that either sharply increased or reduced investment. At bottom, Keynesian macroeconomics makes an unjustified assumption that technological progress unfolds at a relatively smooth rate and it attributes volatility in the economy to fluctuations in investment unrelated to trends in productivity.

The key inside of Keynesian macroeconomics was that inflation and unemployment were inversely correlated, so as one went up, the other went down as Milton Friedman explains.

Marvellously simple. A key that apparently unlocks the mystery of long-continued unemployment: inadequate autonomous spending or too low a propensity to consume. Increase either, or both, being careful simply not to go too far, and full employment could be attained.

What a wonderful prescription: for consumers, spend more out of your income, and your income will rise; for governments, spend more, and aggregate income will rise by a multiple of your additional spending; tax less, and consumers will spend more with the same result.

Though Keynes himself, and even more, his disciples, produced much more sophisticated and subtle versions of the theory, this simple version contains the essence of its great appeal to non-economists and especially governments.

A well-functioning economy should have no business cycles – no bouts of high inflation or persistent unemployment as Richard Rogerson explained:

So if there are cycles, that’s an indication of a malfunctioning economy. That idea permeated thinking for many years and was deeply ingrained. In effect, if an economy is in recession, someone should fix it.

The Keynesians only retreated as their empirical predictions were thoroughly discredited in the 1970s stagflation. Ad hoc auxiliary hypotheses were included about the supply-side in the Keynesian paradigm to prop up the old-time religion, not find new paths as Robert Barro put it:

At least Prescott and other real business cycle theorists accepted that they must eventually unpack productivity drops and name causes that can be explored further to be found persuasive or perhaps wanting. They argued that periods of temporarily low output growth need not be market failures, but could follow from temporarily slow improvements in production technologies.

As research progressed, real business cycles were viewed as recurrent fluctuations in an economy’s incomes, products, and factor inputs—especially labour—due to changes in technology, tax rates and government spending, tastes, government regulation, terms of trade, and energy prices.

Scott Freeman took this research further. He, his colleagues and his progeny showed that real business cycles can occur without any productivity rises and falls whatsoever. All that was needed was the ability to borrow and invest across time to finance lumpy investments. These lumpy investments can be anything from oil wells, dams to new drugs, anywhere involving time to build and capital accumulation:

HT: The Grumpy Economist: Arezki, Ramey, and Sheng on news shocks.

Greece’s GDP collapse is among the worst advanced economy falls since 1870

07 Aug 2015 Leave a comment

in currency unions, economic growth, economic history, Euro crisis, macroeconomics Tags: Eurosclerosis, Greece, prosperity and depression

Greece's GDP collapse is among the worst advanced economy falls since 1870. And most of those were war-related. http://t.co/QLp6fYN83u—

RBS Economics (@RBS_Economics) July 04, 2015

What is the trend growth rate of the USA?

31 May 2015 Leave a comment

in business cycles, economic growth, economic history, great depression, great recession, macroeconomics, politics - USA Tags: prosperity and depression

A volatile depressed neighbour? Real American and Canadian GDP growth detrended, 1955-2013 – updated

11 May 2015 Leave a comment

in business cycles, economic growth, economic history, macroeconomics, politics - USA Tags: Canada, prosperity and depression

Figure 1: Real GDP per American and Canadian aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1955-2013

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

Figure 2: Real GDP per American and Canadian aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1.9 per cent detrended, 1955-2013

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

A rising line in figure 2 is above trend rate growth; a flat line is trend growth of 1.9%; and a falling line is below trend growth.

Canada has a volatile ride in the post-war period after economic success up until 1975. Despite ups and downs the Canadian economy has been in a long-term decline since 1975. Growth as rarely being at trend and was often below, sometimes sharply below trend.

None of these depressed periods in the Canadian economy were long enough to count as a great depression. Instead there was just a long-term decline.

Canada is next door to the USA and a member of the North American Free Trade Area (NAFTA) and its antecedents so its cannot blame distance nor small size for its decline in economic performance as some do in New Zealand.

Relative to the USA, Rao et al. (2006) and Sharp (2003) attributed the gap between the USA and Canada to less capital per Canadian worker, an innovation gap as shown by lower R&D expenditure in Canada, a smaller and less dynamic high technology sector in Canada, less developed human capital at the top end of the Canadian labour market, and more limited scale and scope economies in Canada.

These factors have been put forward, at one time or another, as the proximate causes of the New Zealand productivity gap with the USA. Identifying the barriers to higher Canadian productivity may offer fresh insights into removing similar productivity barriers in New Zealand.

Figure 3 suggests that the increase in tax revenues as a percentage of GDP from 30% to 35% at the same time as the Canadian economic boom came to an end and its economic decline began is worthy of further scrutiny. The strong economic recovery from 1995 onwards also coincided with the decline tax revenues as a percentage of GDP.

Figure 3: tax revenue as a percentage of GDP

Source: OECD StatExtract

Where has all the productivity gone?

11 May 2015 Leave a comment

in business cycles, economic growth, Euro crisis, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics Tags: labour productivity, prosperity and depression, TFP

Britain has led most of the rich world in job creation, but badly lagged in productivity. on.wsj.com/1IiEjli http://t.co/URIFuFS9Il—

Sudeep Reddy (@Reddy) May 07, 2015

Unemployment isn’t much of an issue for the well educated in recessions

09 May 2015 Leave a comment

in business cycles, economic growth, economics of education, human capital, job search and matching, labour economics, labour supply, macroeconomics, occupational choice, unemployment Tags: labour demographics, prosperity and depression

#StayinSchool

April jobless rate for people 25+ with

B.A. or more: 2.7%

No h.s. diploma: 8.6%

on.wsj.com/1H63SHl http://t.co/UwzHjiaQz9—

Sudeep Reddy (@Reddy) May 08, 2015

April jobless rate by race/ethnicity:

Black 9.6%

Hispanic: 6.9%

White 4.7%

Asian 4.4%

on.wsj.com/1H619hg http://t.co/qgRWa7MB85—

Sudeep Reddy (@Reddy) May 08, 2015

The sick men of Europe? British and Irish unemployment rates, 1956–2013

09 May 2015 Leave a comment

in economic growth, economic history, great depression, job search and matching, labour economics, labour supply, macroeconomics, unemployment Tags: British economy, Celtic Tiger, Ireland, prosperity and depression, sick man of Europe, unemployment rates

Source: OECD StatExtract

Ireland and Britain justly earned the name the sick man of Europe in the 1980s. Irish unemployment was in the mid teens much of the 1980s because the Irish economy was in a great depression from 1973 to 1992.

Unemployed people are defined as those who report that they are without work, that they are available for work and that they have taken active steps to find work in the last four weeks. The ILO Guidelines specify what actions count as active steps to find work; these include answering vacancy notices, visiting factories, construction sites and other places of work, and placing advertisements in the press as well as registering with labour offices.

Two booms, two depressions: British and Irish real GDP detrended, 1955–2013

07 May 2015 1 Comment

in business cycles, economic growth, economic history, entrepreneurship, global financial crisis (GFC), great depression, macroeconomics Tags: British disease, British economy, Celtic Tiger, Ireland, prosperity and depression, sick man of Europe

Figure 1: Real GDP per British and Irish aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1955-2013

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

Figure 2 detrends British real GDP growth since 1955 by 1.9% and Irish real GDP growth by 3.6%. The US real GDP growth in the 20th century is used as the measure of the global technological frontier growing at trend rate of 1.9% in the 20th century. The Irish economy is more complicated story because its growth rate in figure 2 was detrended at a rate of 3.6% because it was catching up from a very low base. Trend GDP growth per working age Irish for 1960-73 was 3.6 per cent (Ahearne et al. 2006).

Figure 2: Real GDP per British and Irish aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1.9 per cent detrended UK, 3.6% detrended Ireland, 1955-2013

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

A flat line in figure 2 indicates growth at 1.9% for that year. A rising line in figure 2 means above-trend growth; a falling line means below trend growth for that year.

In the 1950s, Britain was growing quickly that the Prime Minister of the time campaigned on the slogan you never had it so good.

By the 1970s, and two spells of labour governments, Britain was the sick man of Europe culminating with the Winter of Discontent of 1978–1979. What happened? The British disease resulted in a 10% drop in output relative to trend in the 1970s, which counts as a depression – see figure 2 .

Prescott’s definition of a depression is when the economy is significantly below trend, the economy is in a depression. A great depression is a depression that is deep, rapid and enduring:

- There is at least one year in which output per working age person is at least 20 percent below trend; and

- there is at least one year in the first decade of the great depression in which output per working age person is at least 15 percent below trend; and

- There is no significant recovery during the period in the sense that there is no subperiod of a decade or longer in which the growth of output per working age person returns to rates of 2 percent or better.

The British disease in the 1970s bordered on a depression. There was then a strong recovery through the early-1980s with above trend growth from the early 1980s until 2006 with one recession in between in 1990. So much for the curse of Thatchernomics?

Figure 1 suggests a steady economic course in Ireland until the 1990s with a growth explosion growth with the Irish converged on British living standards up until the global financial crisis.

Figure 2 shows the power of detrending GDP growth and why Ireland was known as the sick man of Europe in the 1970s and 1980s with unemployment as high as 18% and mass migration again. The Irish population did not grow for about 60 years from 1926 because of mass migration.

Figure 2 shows that real GDP growth per working age Irish dropped below its 3.6 per cent trend for nearly 20 years from 1974 , but more than bounced back after 1992. The deepest trough was 18 per cent below trend and the final trough was in 1992 – see Figure 2.

The deviation from trend economic growth made the Irish depression from 1973 to 1992 comparable in depth and length to the 1930s depressions (Ahearne et al. 2006).

The Irish depression of 1973 to 1992 can be attributed to large increases in taxes and government expenditure and reduced productivity (Ahearne et al. 2006). There were two oil price shocks in the 1970s and many suspect Irish policy choices from 1973 to 1987.

There were three fiscal approaches: an aggressive fiscal expansion from 1977; tax-and-spend from 1981; and aggressive fiscal cuts from 1987 onwards. In the early 1980s, Irish CPI inflation at 21 per cent, public sector borrowing reached 20 per cent of GNP.

To rein in budget deficits, taxes as a share of GNP rose by 10 percentage points in seven years. The unemployment rate reached 17 per cent despite a surge in emigration. The rising tax burden raised wage demands, worsening unemployment. Government debt grew on some measures to 130 per cent of GNP in 1986 (Honohan and Walsh 2002).

From 1992, Ireland rebounded to resume catching-up with the USA. The Celtic Tiger was a recovery from a depression that was preceded by large cuts in taxes and government spending from the late 1980s (Ahearne et al. 2006). Others reach similar conclusions but avoid the depression word. Fortin (2002, p. 13) labelled Irish public finances in the 1970s and to the mid-1980s as a ‘black hole’.

Fortin (2002) and Honohan and Walsh (2002) disentangle the Irish recovery into a long-term productivity boom that had dated from the 1950s and 1960s, and a sudden short-term output and employment boom since 1993 following the late 1980s fiscal and monetary reforms.

Honohan and Walsh (2002) wrote of belated income and productivity convergence. The delay in income and productivity convergence came from poor Irish economic and fiscal policies in the 1970s and 1980s.

This was after economic reforms in the late 1950s and the 1960s that started a process of rapid productivity convergence after decades of stagnation and mass emigration; Ireland’s population was the same in 1926 and 1971. During the 1950s, up to 10 per cent of the Irish population migrated in 10 years.

In the 1990s, many foreign investors started invested in Ireland as an export platform into the EU to take advantage of a 12.5 per cent company tax rate on trading profits. Between 1985 and 2001, the top Irish income tax rate fell from 65 to 42 per cent, the standard company tax from 50 to 16 per cent and the capital gains tax rate from 60 to 20 per cent (Honohan and Walsh 2002).

What happened after the onset of the global financial crisis in Ireland and the UK are for a future blog posts.

Has the USA moved to lower trend GDP growth path?

26 Jan 2015 Leave a comment

in business cycles, economic growth, great recession, macroeconomics, politics - USA Tags: great recession, Jagadeesh Gokhale, prosperity and depression

Paul Samuelson and Robert Lucas both agree that economists have solved the problem of economic depressions

24 Jan 2015 Leave a comment

in business cycles, fiscal policy, great depression, great recession, history of economic thought, macroeconomics, monetary economics, Robert E. Lucas Tags: Paul Samuelson, prosperity and depression, The fatal conceit, The pretence to knowledge

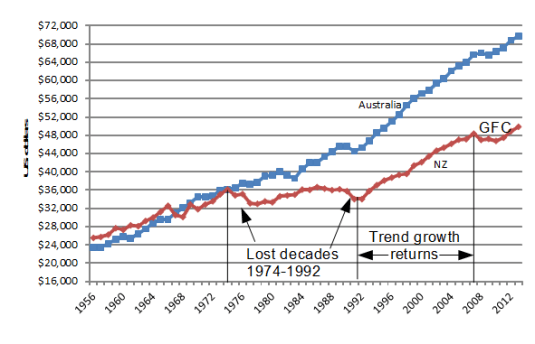

Real GDP per New Zealander and Australian aged 15-64, PPP, 1956-2013, $US

18 Nov 2014 1 Comment

in business cycles, economic growth, geography, global financial crisis (GFC), great recession, macroeconomics, politics - Australia, politics - New Zealand Tags: lost decades, prosperity and depression

Figure 1: Real GDP per New Zealander and Australian aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1956-2013, $US

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

Figure 1 shows that New Zealand lost two decades of growth between 1974 and 1992 after level pegging with Australia for the preceding two decades.

New Zealand returned to trend growth between 1992 and 2007. New Zealand did not make up the lost growth of the previous two decades to catch up to Australia.

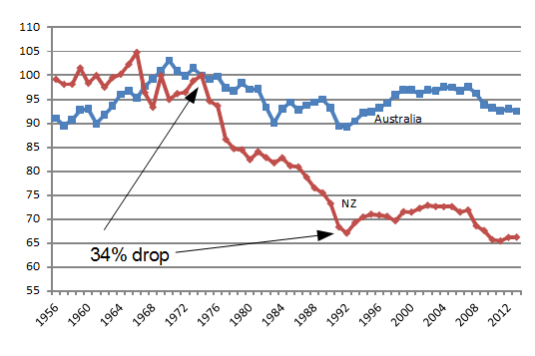

Figure 2: Real GDP per New Zealander and Australian aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1.9 per cent detrended, base 100 = 1974, 1956-2013, $US

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

In Figure 2, a flat line equates to a 1.9% GDP annual growth rate; a falling line is a below trend growth rate; a rising line is an above 1.9% growth rate.

Figure 2 shows that there was a 34% drop against trend between 1974 and 1992; a return to trend growth and slightly better between 1992 and 2007; and then a recession to 2010.

Australia had its ups and downs since 1956 but essentially grew at the trend growth rate of 1.85% since 1970. The so-called resources boom in Australia does not show up in Figures 1 or 2.

There was no growth rebound in New Zealand to recover the lost ground, either in the lost decades between 1974 and 1992, or after the Global Financial Crisis. The strong GDP growth in Australia after that Keating recession in 1991 is an example of the country recovering lost ground after a recession – See Figure 2.

A trend growth rate of 1.9% is the 20th century trend growth rate that Edward Prescott currently estimates for the global industrial leader, which is the United States of America.

The Top 1% of income earners in NZ are lazy – the Occupy Movement have nothing to protest about – updated

25 Oct 2014 Leave a comment

in applied welfare economics, income redistribution, Marxist economics, politics - New Zealand, rentseeking Tags: lost decades, occupy movement, poverty and inequality, prosperity and depression, top 1%

The NZ top 1% share has been steady at 8-9% since the mid-1990s. The top 1%’s share rose strongly in the USA in recent decades, from 13% in the mid-1980s to 19% in 2012.

Figure 1: Top 1% income shares, USA, New Zealand and Sweden, 1970-2012

Source: The World Top Income Database at http://topincomes.g-mond.parisschoolofeconomics.eu/#Database

The top 1% in New Zealand is so lazy that Sweden is overtaking it – See figure 1.

The Occupy crowd blame everything from the global financial crisis to a bad environment on growing inequality and the top 1%. Such an argument has no foundation in fact in New Zealand.

Income inequality as measured by the Gini coefficient has not risen much in New Zealand for 20 years – See figure 2. How can the poor be getting getting poorer, ground under by the yoke of capitalism, if the rich are not getting richer. The occupy movement should apply for unemployment benefits and seek career guidance.

Figure 2: Gini coefficient New Zealand 1980-2015

![clip_image002[7]](https://utopiayouarestandinginit.com/wp-content/uploads/2014/10/clip_image00271.png "clip_image002[7]")

Source: Bryan Perry, Household incomes in New Zealand: Trends in indicators of inequality and hardship 1982 to 2013. Ministry of Social Development (July 2014).

The last major increase in income inequality in New Zealand was in the late 1980s and early 1990s and that was followed by a long economic boom – See figure 3 .

Figure 3: Real GDP per New Zealander and Australian aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1956-2012

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics .

This long boom was after two decades of next to no economic growth in the 1970s and 1980s in New Zealand – see figure 3 . This depression between 1974 and 1992 was New Zealand’s lost decades.

Figure 4 shows that both the lost decades of economic growth in New Zealand and the emergence of the trans-Tasman income gap the seemed to somewhat coincide with the top 1% of earners in Australia increasing their share of income from 6% to 10% of total incomes while the New Zealand top 1% sat on their hands. They are such lazy devils.

Figure 4: Top 1% income shares, USA, New Zealand and Australia, 1970-2012

Source: The World Top Income Database at http://topincomes.g-mond.parisschoolofeconomics.eu/#Database

Recent Comments