Recurrent business cycles without shocks – the role of lumpy investments

11 Aug 2015 Leave a comment

in business cycles, economic growth, Edward Prescott, entrepreneurship, financial economics, fiscal policy, industrial organisation, macroeconomics, Milton Friedman, monetarism, monetary economics Tags: Edward Prescott, mega sports events, mega-projects, Mexico, Norway, prosperity and depression, R&D, real business cycles, Richard Rogerson, Robert Barro, technology diffusion lags

Think it is time for a re-post of @LHSummers' brilliant, brilliant paper on RBC from 1986. minneapolisfed.org/research/qr/qr… http://t.co/S7tGIjEebI—

Simon H (@simonhinrichsen) August 10, 2015

The brilliant monetary economist Scott Freeman was one of the 1st to show the existence of real business cycles without the need of shocks to drive the ups and downs of the economy. He did this when taking time off from showing that much of the apparent correlation between the nominal and the real side of the economy is due to the endogenous response of money created by banks to fluctuations in real activity.

In 1999, Scott Freeman co-wrote Endogenous Cycles and Growth with Indivisible Technological Developments. The paper was about large, discrete technological improvements that required the accumulation of research or infrastructural investment over time before any benefits for realised in terms of increased output. With these lead-times for research or infrastructure investments, growth paths display cyclical patterns even in the absence of any shocks.

This lumpiness over time implied that a costly process such as research or construction must be completed on a large scale before the greatest part of a project’s benefits in output can be realized as Freeman and co. argue:

There are numerous examples of big research or infrastructural projects that are characterized by huge investments and relatively long development periods, where most of the benefits occur only after the project is complete.

Freeman and his co-authors gave as examples space research and satellite programs and major medical research. These are examples of prolonged and costly R & D whose benefits come primarily at the conclusion of the project.

Lags in the development of a new drug between the commencement of the R&D project and any revenues received is routinely now more than a decade. The Human Genome Project seems to be going on without end with few initial benefits.

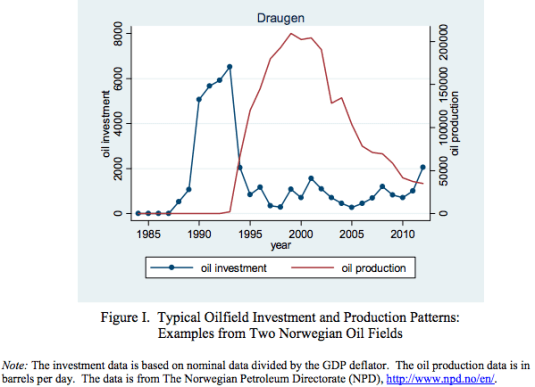

Infrastructural examples given by Freeman and his co-authors included the installation of telephone, the internet, transportation shipping canals, interregional highways, railroads, mass transit or electricity transmission projects. All of these projects with long lead times, once completed that may increase the productivity of many economic sectors in addition to increasing output in the area concerned. In many cases there are no benefits whatsoever of the project and to after it is completed many years in the future. Oil pipelines can take up to a decade to build.

The 1973 oil price crisis launched a research and development program into alternative sources of energy and alternative sources of oil and gas supply that has lasted to this day.

Classic further examples of long lead times are mega sports events such as the World Cup and Olympic Games. Years of planning, development and construction for any benefits or revenues are obtained.

What is important in terms of the random shocks that drive the business cycle as championed by Ed Prescott is there are a range of sectors within the economy where there are long lead times before the investment leads to any outputs. Not surprisingly the first article in the real business cycle literature included in its title “time to build“.

Rabah Arezki, Valerie Ramey, and Liugang Sheng in “News Shocks in Open Economies: Evidence from Giant Oil Discoveries” explore a related theme of real business cycles without shocks. In particular, they investigate news of productivity enhancements. They look at what happens to economies that discover oil. An oil discovery is a well identified “news shock.”

An oil discovery is well publicised and creates an incentive to invest in oil drilling. More importantly, there is news of greater income in the future but no change in current labour productivity or technological opportunities.

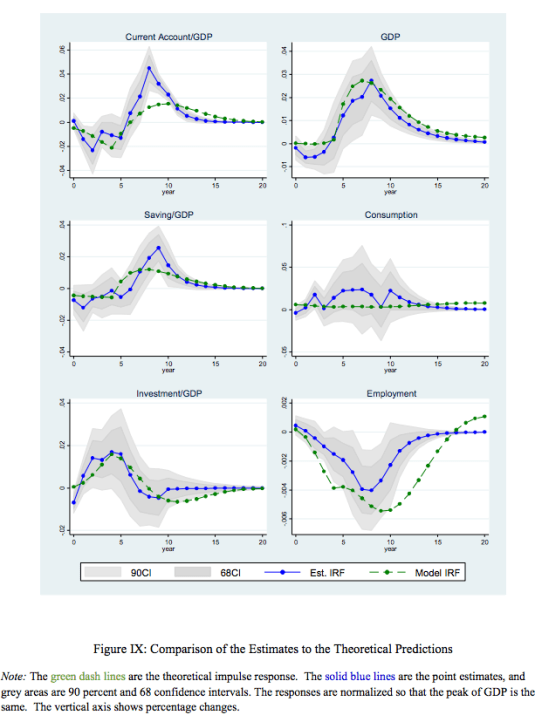

Rabah,Valerie, and Liugang found that after big oil discoveries, during the period of investment, the newly rich oil country borrows from abroad to build oil wells, oil pipelines and associated port infrastructure, obviously, but also borrows to finance higher consumption now. Consumption goes up and stays up in permanent income hypothesis fashion.

Interestingly, employment declines because of the wealth effect from the future income but there is no higher productivity of labour to encourage more work today. Investment rises soon after the news of the oil discovery arrives, while GDP does not increase for 5 years or more.

This is consistent with experience in the oil-rich Arab countries where there was increased consumption of leisure in anticipation of high future income is based on oil.

The same happened in Norway where massive investment was funded by foreign borrowing that led to annual current account deficits of up to 15% of GDP. Domestic savings fell away because Norwegians anticipated higher future incomes and started spending some of it now as predicted by the permanent income hypothesis. Norway now has a huge sovereign wealth fund able to fund a large part of its demographic burden from an ageing society.

After Mexico’s discovery of oil in the early 1970s, investment was high in oil and related industries. Consumption—by households and government—rose because of the increase in prospective real income. Since real GDP was not yet high, Mexico borrowed to pay for both the oil investment and the higher current consumption. Mexico’s foreign debt increased from $3.5 billion or 9% of GDP in 1971 to $61 billion or 26% of GDP in 1981. This boom in consumption and investment occurred without any productivity shock. All that was required was the ability to borrow.

Once the oil comes on line, the economy concern exports oil and pays back debt. This is when GDP including oil production finally rises a good five years and often more after the oil discovery. Consumption continues for its previous high rates while investment falls as the oil wells and pipelines have been built.

As with Scott Freeman, the long lead times not only can lead to large swings in investment, lumpy investments can also lead to increases in consumption, savings and employment without any productivity shocks.

Keynesian macroeconomics postulated that the economy slips into recessions for all sorts of reasons such as shifts and turns in the animal spirits and a loss of consumer confidence leading to a fall in autonomous investment and autonomous consumption. A collapse in autonomous investment and autonomous consumption is the Keynesian explanation for the great depression.

Both Keynesian macroeconomics and real business cycle theories at least at the outset couldn’t explain why there were recessions. Both attributed to them to causes they were yet to explain.

Keynesian macroeconomics could not explain what drove the waves of optimism and pessimism that either sharply increased or reduced investment. At bottom, Keynesian macroeconomics makes an unjustified assumption that technological progress unfolds at a relatively smooth rate and it attributes volatility in the economy to fluctuations in investment unrelated to trends in productivity.

The key inside of Keynesian macroeconomics was that inflation and unemployment were inversely correlated, so as one went up, the other went down as Milton Friedman explains.

Marvellously simple. A key that apparently unlocks the mystery of long-continued unemployment: inadequate autonomous spending or too low a propensity to consume. Increase either, or both, being careful simply not to go too far, and full employment could be attained.

What a wonderful prescription: for consumers, spend more out of your income, and your income will rise; for governments, spend more, and aggregate income will rise by a multiple of your additional spending; tax less, and consumers will spend more with the same result.

Though Keynes himself, and even more, his disciples, produced much more sophisticated and subtle versions of the theory, this simple version contains the essence of its great appeal to non-economists and especially governments.

A well-functioning economy should have no business cycles – no bouts of high inflation or persistent unemployment as Richard Rogerson explained:

So if there are cycles, that’s an indication of a malfunctioning economy. That idea permeated thinking for many years and was deeply ingrained. In effect, if an economy is in recession, someone should fix it.

The Keynesians only retreated as their empirical predictions were thoroughly discredited in the 1970s stagflation. Ad hoc auxiliary hypotheses were included about the supply-side in the Keynesian paradigm to prop up the old-time religion, not find new paths as Robert Barro put it:

At least Prescott and other real business cycle theorists accepted that they must eventually unpack productivity drops and name causes that can be explored further to be found persuasive or perhaps wanting. They argued that periods of temporarily low output growth need not be market failures, but could follow from temporarily slow improvements in production technologies.

As research progressed, real business cycles were viewed as recurrent fluctuations in an economy’s incomes, products, and factor inputs—especially labour—due to changes in technology, tax rates and government spending, tastes, government regulation, terms of trade, and energy prices.

Scott Freeman took this research further. He, his colleagues and his progeny showed that real business cycles can occur without any productivity rises and falls whatsoever. All that was needed was the ability to borrow and invest across time to finance lumpy investments. These lumpy investments can be anything from oil wells, dams to new drugs, anywhere involving time to build and capital accumulation:

HT: The Grumpy Economist: Arezki, Ramey, and Sheng on news shocks.

Is unemployment voluntary or involuntary?

27 Jun 2014 Leave a comment

in business cycles, job search and matching, labour economics, macroeconomics, unemployment Tags: Alan Manning, Armen Alchian, Robert Barro, Robert Lucas, unemployment

Robert Lucas in a famous 1978 paper argued that all unemployment was voluntary because involuntary unemployment was a meaningless concept. He said as follows:

The worker who loses a good job in prosperous time does not volunteer to be in this situation: he has suffered a capital loss. Similarly, the firm which loses an experienced employee in depressed times suffers an undesirable capital loss.

Nevertheless the unemployed worker at any time can always find some job at once, and a firm can always fill a vacancy instantaneously. That neither typically does so by choice is not difficult to understand given the quality of the jobs and the employees which are easiest to find.

Thus there is an involuntary element in all unemployment, in the sense that no one chooses bad luck over good; there is also a voluntary element in all unemployment, in the sense that however miserable one’s current work options, one can always choose to accept them.

I agree that we all make choices subject to constraints. To say that a choice is involuntary because it is constrained by a scarcity of job-opportunities information is to say that choices are involuntary because there is scarcity.

Alchian said there are always plenty of jobs because to suppose the contrary suggests that scarcity has been abolished. Lucas elaborated further in 1987 in Models of Business Cycles:

A theory that does deal successfully with unemployment needs to address two quite distinct problems.

One is the fact that job separations tend to take the form of unilateral decisions – a worker quits, or is laid off or fired – in which negotiations over wage rates play no explicit role.

The second is that workers who lose jobs, for whatever reason, typically pass through a period of unemployment instead of taking temporary work on the ‘spot’ labour market jobs that are readily available in any economy.

Of these, the second seems to me much the more important: it does not ‘explain’ why someone is unemployed to explain why he does not have a job with company X. After all, most employed people do not have jobs with company X either.

To explain why people allocate time to a particular activity – like unemployment – we need to know why they prefer it to all other available activities: to say that I am allergic to strawberries does not ‘explain’ why I drink coffee. Neither of these puzzles is easy to understand within a Walrasian framework, and it would be good to understand both of them better, but I suggest we begin by focusing on the second of the two.

Another way to understand unemployment is to use a device at the start of Alan Manning’s book on labour market monopsony:

What happens if an employer cuts the wage it pays its workers by one cent? Much of labour economics is built on the assumption that all existing workers immediately leave the firm as that is the implication of the assumption of perfect competition in the labour market.

In such a situation an employer faces a market wage for each type of labour determined by forces beyond its control at which any number of these workers can be hired but any attempt to pay a lower wage will result in the complete inability to hire any of them at all

Suppose workers offered to work for 1 cent. Would employers accept? Many do because they have intern and work experience programmes for students, but is this result of general application?

Understanding the reallocation of labour at the end of the recession requires careful attention to the 1980s writing of Alchian on the theory of the firm. Alchian and Woodward’s 1987 ‘Reflections on a theory of the firm’ says:

… the notion of a quickly equilibrating market price is baffling save in a very few markets. Imagine an employer and an employee. Will they renegotiate price every hour, or with every perceived change in circumstances?

If the employee is a waiter in a restaurant, would the waiter’s wage be renegotiated with every new customer? Would it be renegotiated to zero when no customers are present, and then back to a high level that would extract the entire customer value when a queue appears?

… But what is the right interval for renegotiation or change in price? The usual answer ‘as soon as demand or supply changes’ is uninformative.

Alchian and Woodward then go on to a long discussion of the role of protecting composite quasi-rents from dependent resources as the decider of the timing of wage and price revisions.

Alchian and Woodward explain unemployment as a side-effect of the purpose of wage and price rigidity, which is the prevention of hold-ups over dependent assets. They note that unemployment cannot be understood until an adequate theory of the firm explains the type of contracts the members of a firm make with one another.

My interpretation is the majority of employment relationships are capital intensive long-term contracts. Employers spend a lot of time searching and screening applicants to find those that will stay longer. In less skilled jobs, and in spot market jobs, employers will hire the best applicant quickly because job turnover costs are low. Back to Manning again:

That important frictions exist in the labour market seems undeniable: people go to the pub to celebrate when they get a job rather than greeting the news with the shrug of the shoulders that we might expect if labour markets were frictionless. And people go to the pub to drown their sorrows when they lose their job rather than picking up another one straight away. The importance of frictions has been recognized since at least the work of Stigler (1961, 1962).

Whatever may be among these frictions, wage rigidity is not one of them. Wages are flexible for job stayers and certainly new starters.

See What can wages and employment tell us about the UK’s productivity puzzle? by Richard Blundell, Claire Crawford and Wenchao Jin showing that in the recent UK recession 12% of employees in the same job as 12 months ago experienced wage freezes and 21% of workers in the same job as 12 months ago experienced wage cuts. Their data covered 80% of workers in the New Earnings Survey Panel Dataset.

Larger firms lay off workers; smaller firms tended to reduce wages. This British data showing widespread wage cuts dates back to the 1980s. Recent Irish data also shows extensive wage cuts among job stayers.

See too Chris Pissarides (2009), The Unemployment Volatility Puzzle: Is Wage Stickiness the Answer? arguing the wage stickiness is not the answer since wages in new job matches are highly flexible:

- wages of job changers are always substantially more procyclical than the wages of job stayers.

- the wages of job stayers, and even of those who remain in the same job with the same employer are still mildly procyclical.

- there is more procyclicality in the wages of stayers in Europe than in the United States.

- The procyclicality of job stayers’ wages is sometimes due to bonuses, and overtime pay but it still reflects a rise in the hourly cost of labour to the firm in cyclical peaks

How do existing firms who will not cut wages survive in competition with new firms who can start workers on lower wages? Industries with many short term jobs and seasonal jobs would suffer less from wage inflexibility.

Robert Barro (1977) pointed out that wage rigidity matters little because workers can, for example, agree in advance that they will work harder when there is more work to do—that is, when the demand for a firm’s product is high—and work less hard when there is little work. Stickiness of nominal wage rates does not necessarily cause errors in the determination of labour and production.

The ability to make long-term wage contracts and include clauses that guard against opportunistic wage cuts should make the parties better off. Workers will not sign these contracts if they are against their interests. Employers do not offer these contracts, and offer more flexible wage packages, will undercut employers who are more rigid. Furthermore many workers are on performance pay that link there must wages to the profitability of the company.

How can downward wage rigidity be a scientific hypothesis if extensive international evidence of widespread wage cuts since the 1980s and 30%+ of the workforce on performance bonuses is not enough to refute it?

Alchian and Kessel in “The Meaning and Validity of the Inflation-Induced Lag of Wages Behind Prices,” Amer. Econ. Rev. 50 [March 1960]:43-66) tested the hypothesis that workers suffered from money illusion by comparing the rates of return to firms in capital intensive industries with those of labour intensive industries. Labour intensive industries were not more profitable than capital intensive industries. Employers in labour intensive industries should profit from the misperceptions of workers about wages and future prices, but they did not. Alchian and Kessel found little evidence of a lag between wage and price changes.

In Canadian industries in the 1960s and 1970s, wage indexation ranged from zero to nearly 100%. Industries with little indexation should show substantial responses of real wage rates, employment and output to nominal shocks. Industries with lots of indexation would be affected little by nominal disturbances. Monetary shocks had positive effects but an industry’s response to these shocks bore no relation to the amount of indexation in the industry. Shaghil Ahmed (1987) found that those industries with lots of indexation were as likely as those with little indexation to respond to shocks.

If the signing of new wage contracts was important to wage rigidity, there should be unusual behaviour of employment and real wage rates just after these signings, but the results are mixed. Olivei and Tenreyro (2010) used the tendency of contracts to be signed at the start of years to show that monetary policy had significant effects in January but little effect in December because the effects were quickly undone.

Alchian (1969) lists three ways to adjust to unanticipated demand fluctuations:

• output adjustments;

• wage and price adjustments; and

• Inventories and queues (including reservations).

Alchian (1969) suggests that there is no reason for wage and price changes to be used regardless of the relative cost of these other options:

• The cost of output adjustment stems from the fact that marginal costs rise with output;

• The cost of price adjustment arises because uncertain prices and wages induce costly search by buyers and sellers seeking the best offer; and

• The third method of adjustment has holding and queuing costs.

There is a tendency for unpredicted price and wage changes to induce costly additional search. Long-term contracts including implicit contracts arise to share risks and curb opportunism over relationship-specific capital. These factors lead to queues, unemployment, spare capacity, layoffs, shortages, inventories and non-price rationing in conjunction with wage stability.

What did fiscal policy do in World War II?

23 Jun 2014 Leave a comment

in fiscal policy, macroeconomics Tags: fiscal policy, Lee Ohanian, Robert Barro

It is ironic that both camps use World War II as evidence that the fiscal policy might work (Keynesian macroeconomics) or it does not work (Barro and Ohanian).

The nature of the new spending and how it was financed both matter, as does whether the new spending was a public good, a private good or a general or contingent income transfer matter, and whether the new spending was tax or bond financed all matter to the income and substitution effects of taxes and the additional public debt.

World War II was a temporary increase in government military purchases that will be followed by a long period of primary budget surpluses and perhaps surprise spikes in price inflation to pay down the massive wartime debt.

- A military build-up financed by debt lowers consumer wealth which induces households to consume less leisure and work more while the temporary nature of the fiscal shock increases labour input through inter-temporal substitution of labour into the period of lower taxes.

- The increase in the supply of labour leads to a fall in productivity and real wages. Inter-temporal substitution of labour also raises the real interest rate and lowers private investment.

Barro found that World War II U.S. defence expenditures increased by $540 billion per year at the peak in 1943-44, amounting to 44% of real GDP. this increased real GDP by $430 billion per year in 1943-44 – a multiplier was 0.8 (430/540). The main declines were in private investment, non-military government purchases, and net exports. Wartime production was a dampener, rather than a multiplier.

The war-based multiplier of 0.8 overstates the multiplier that would apply to peacetime government purchases. Public spending crowds out private spending wartime because of intertemporal substitution of labour and consumption smoothing so private investment falls substantially.

People expect the added wartime spending to be temporary so consumer demand will fall by less. Consumers saving less to smooth out the changes in consumption relative the changes in their current after-tax income if the war is expected to last no more than a few years and no major destruction of capital stock and population is anticipated.

Korean War expenditures were financed mostly by higher taxes resulted in a much lower output and welfare compared to the tax smoothing policy for World War II.

The US borrowed heavily to finance World War II as did for most of its previous wars. This means the tax rises necessary to pa for the war debt were spread over a much longer period of time and would in consequence have less effect on labour supply and investment.

In the Korean War, taxes were increased immediately to finance the war. In consequence,labour supply and investment dropped immediately during the period of high taxes

Britain taxed capital income at a much higher rate than the United States during the war and for much of the post-war period. Lee Ohanian explains what happened:

British capital income tax rates rose substantially during the war—they approached 90 per cent—and remained high after it.

Not surprisingly, savings and investment were close to zero over this period, reflecting the very low after-tax return to savings.

In time, London reduced tax rates on savings and investment—and, as a result, savings and investment began to rise, increasing from about 3 per cent of British GDP in the early 1950s to 20 per cent of GDP in the 1980s.

But before its capital income tax rates fell, the United Kingdom was among the slowest growing countries in the industrialized West.

The voter as a fiscal conservative

16 Jun 2014 Leave a comment

in budget deficits, macroeconomics Tags: Ricardian theory of budget deficits, Robert Barro

Now that every election policy must be fully costed, and every major party promises a return to surplus in a few years, the Ricardian theory of budget deficits is now an optimistic view of the power of fiscal policy.

By running a budget deficit, it shifts from collecting taxes today to collecting them tomorrow and fund the intervening shortfall was selling government bonds to the private sector. A finance minister may choose to lower taxes today (thereby increasing the deficit), but without any planned changes in the government’s expenditure program, such a policy must imply higher taxes at some point in the future.

The Ricardian theory of budget deficits is people are smart enough to recognise that today’s fiscal deficits mean tomorrow’s taxes must increase to to repay the debt so taxpayers cut back consumption dollar for dollar to save for those future taxes.

If you know your taxes will go up in the future, the right thing to do is save to pay those higher taxes. A fiscal stimulus is then completely offset by the reduction in private consumption. The stimulus has no effect on spending, prices, production, or interest rates because households know that deficit spending means future taxes: to smooth consumption, they save more now.

To make things worse, the lower taxes today and the higher taxes tomorrow encourage intertemporal substitution of labour. People will work more now because taxes are low but work less in the future when taxes are high. Investors also take into account that taxes on their investment income will be higher in the future so they will invest less now.

Notice below the mirror trends of net private and government savings as a per cent of U.S. GDP. Financing U.S. government consumption through deficits or through taxation is equivalent: households know net present value of taxation will rise and save to offset that.

HT: correctionspageone.blogspot

If you think a fiscal stimulus works by fooling people into ignoring the future tax hikes or spending cuts, then loudly announcing in an election campaign those tax hikes and spending cuts in a few year’s time that will pay for the current fiscal stimulus must undermine that stimulus even more!

When Robert Barro wrote in the 1970s and 1980s, he pointed out that there is no reason to assume that forecasting errors about future taxes are always biased in the direction of under-estimating the future taxes. People can over-estimate the future taxes. Individual uncertainty about their future tax liabilities does not normally induce them to save less, it induces them to save more.

The fact that much political debate surrounds government budget deficits clearly suggests that the voters understand the government budget constraint and that high budget deficits today signal higher taxes in the future and they change their behaviour accordingly.

Robert Barro likes to refer to Israel as a natural experiment in the Ricardian budget deficit theory. In 1983, the national saving rate of 13% of GDP corresponded to a private saving rate of 17% and a public saving rate of -4%. In 1984, the dramatic rise in the budget deficit reduced the public saving rate to -11%. Private saving rate rose to 26%, so that the national saving rate changed little. Then a stabilisation program in 1985 eliminated the budget deficit, so that the public saving rate rose to 0% in 1985-86 and -2% in 1987. The private saving rate declined dramatically to 19% in 1985 and 14% in 1986-87. The national saving rate remained relatively stable, going from 15% in 1984 to 18% in 1985, 14% in 1986, and 12% in 1987.

The best evidence that people do take future taxes into account is the method in which old age pensions are financed in different countries. An expansion of social security pensions for the retired is analogous to a deficit-financed tax cut. People respond to more social security by shifting private intergenerational transfers, rather than by consuming more.

In the US, the growth of social security strongly diminished the tendency of children to support their aged parents because they are paying taxes now and in the future to support them. In countries were weak social security, children spend more of their money looking after their parents.

51% of nonretirees doubt they will receive Social Security… on.gallup.com/1NcwzEa #GallupDaily http://t.co/ZhKnHYtr1X—

(@GallupNews) August 13, 2015

It is certainly the case that most younger people think they have to provide for their own retirement and that government will not tax enough to support them in 20 to 30 years time.

People have relatively sophisticated views of both long-run government spending and taxing in an ageing society and that deficits must be paid for. The voter is a fiscal conservative.

Old macroeconomic fallacies never die, they just wait for the next recession

21 Apr 2014 1 Comment

in history of economic thought, macroeconomics Tags: cost-push fallacy, Murray Rothbard, Robert Barro, rules versus discretion, Thomas Humphrey, Thomas Kiuhn

Thomas Kuhn’s Structure of Scientific Revolutions showed that sciences do not march onwards and upwards towards the light. Kuhn found that once a central paradigm is selected, there is no testing or sifting, and tests of basic assumptions only take place after accumulated failures and anomalies in the ruling paradigm plunge the science into a crisis.

Scientists do not give up the failing paradigm until a new paradigm arrives, which resolves the failures and anomalies that caused the crisis. It takes a theory to beat a theory.

Murray Rothbard, when discussing Kuhn, pointed to economics is an example of a science which moves in a zigzag fashion, with old fallacies sometimes elbowing aside earlier but sounder paradigms.

Thomas Humphrey wrote an excellent 250-year long literature surveys of both the rules versus discretion debate and the cost-push theories of inflation in the 1998 and 1999 Richmond Fed Quarterly.

Humphrey wrote the reviews to see if economics was a progressive science in the sense that superior new ideas relentlessly supplant inferior old ones.

Humphrey showed that policy rules were popular in good times to contain inflation, and when unemployment was rising, discretionary policies returned to vogue. The policy debate keeps recycling because

- people forget the lessons of the past; and

- For better or worse, politicians and the public have tended to believe that central banks, the focus of his studies, have the power to boost output, employment, and growth permanently.

Mercantilists, with their fears of hoarding and scarcity of money together with their prescription of cheap (low interest rates) and plentiful cash as a stimulus to real activity, tend to gain the upper hand when unemployment is the dominant problem.

Classicals, chanting their mantra that inflation is always and everywhere a monetary phenomenon, tend to prevail when price stability is the chief policy concern.

Cost-push fallacies about inflation were even more resilient against repeated refutations.

There is nothing new under the sun in macroeconomics. The same issues that divided twentieth-century monetarists and non-monetarists as well as current macroeconomists were discussed by everyone from David Hume (1752) to Knut Wicksell (1898) and in the Bullionist-Anti-Bullionist and the Currency School-Banking School controversies:

- rules v. discretion,

- inflation as a monetary v. real cost push phenomenon,

- direct v. inverse money-to-price causality,

- central bank-determined v. market demand-determined money stocks,

- exogenous v. endogenous money, and

- backing v. supply-and-demand theories of money’s value

Current macroeconomists and monetary economists often unaware of the eighteenth and nineteenth-century origins of the ideas they employ.

Barro (1989) “New Classicals and New Keynesians, or the Good Guys and the Bad Guys”, made the point that Keynesian macroeconomics does not seek out new theoretical results for testing; rather the aim is to provide respectability for the basic viewpoints and policy stances of the old Keynesian models.

Bellante (1992) likewise, noted that the search in Keynesian economics for microeconomic foundations is to blunt criticism, rather than because it is otherwise useful. The analytical apparatus may change, but the policy conclusions remain the same.

Recent Comments