Unemployment, job search, search and matching

Unemployment, job search, search and matching

WH Hutt on job search

14 Dec 2014 Leave a comment

in job search and matching, labour economics, macroeconomics, unemployment Tags: job search, search and matching, unemployment, voluntary unemployment

Second law of supply and demand alert: There is no such thing as a skills shortage – updated

01 Dec 2014 Leave a comment

in applied price theory, labour economics, unemployment Tags: Alfred Marshall, Armen Alchian, comparative statics, labour market shortages, search and matching, second law of demand, second law of supply, skill shortages, unemployment

Could you define both a severe skills shortage and a skills shortage?

- How do these concepts differ from concepts such as rising demand, rapidly rising demand, and reduced and sharply reduced supply?

- Are the phrases severe skills shortage and a skills shortage more precise than the phrases rising demand, rapidly rising demand, and reduced and sharply reduced supply?

- Are the phrases severe skill shortage and a skill shortage more informative than referring to the short and long run elasticity of demand and supply as summed up in the second laws of demand and supply?

- Why are rising demand, rapidly rising demand, and reduced and sharply reduced supply considered to be social problems. What causes rising demand, rapidly rising demand, and reduced and sharply reduced supply?

- For whom are rising demand, rapidly rising demand, and reduced and sharply reduced supply considered to be problems? Employers? Employees? Others?

- Should governments intervene to stop employers from competing to set wages to reflect increases in the marginal revenue product of labour?

- Is not the purpose of short and long-term upward changes in relative prices or wages to induce people to buy less of a now scarcer resource and search for substitutes and additional sources of supply, and for new suppliers to enter the market in response to the higher prices or wages?

As a starter, I thought I would update Alchian and Arrow’s timeless 1958 analysis for the Rand Corporation of the purported shortage of engineers and scientists at the height of the missile gap in the cold war.

Alchian and Arrow tested the robustness of claims of a labour market shortage of scientists and engineers by investigating the sudden appearance of a servant shortage during World War II.

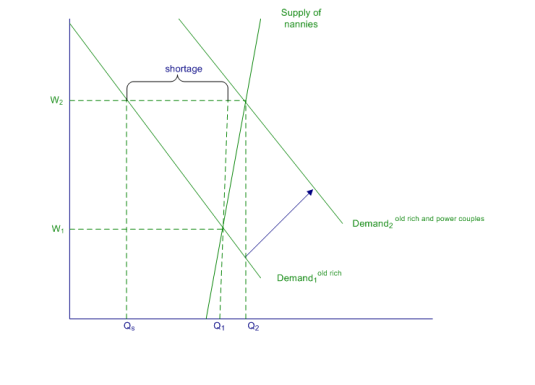

I will update this idea of a servant shortage to a purported shortage of nannies, as shown in figure 1 below which sets out the initial equilibrium and then an increase in demand.

Figure 1: the demand and supply for nannies by the old rich and power couples

In the diagram above, the initial equilibrium has the old rich hiring Q1 nannies at a wage W1 with demand curve D1, and the supply curve for nannies.

- Power couples then enter the nannies market pushing total demand out to D2 with wages increasing to W2 and quantity supplied increasing a little to Q2;

- The old rich can now afforded to buy only Qs in nannies and power couples hire (Q2 – Qs) in nannies.

By construction, the quantity of nannies supplied increases slightly in the short-run, with a large increase in wages for nannies! (Q2 – Q1) new nannies enter the market, lured in by the higher wages.

The old rich now face a shortage of nannies equal to the quantity (Q1 – Qs). These nannies having switched to work for power couples on much better pay. (In the case of the original analysis Alchian and Arrow analysis, they switched into defence work or backfilled jobs of those that moved into defence work).

As with the wartime servant shortage, the old rich are unwilling to admit they are no longer able to keep themselves in the style they were accustomed too because the demand for domestic labour has increased.

Better to blame their loss of social status on a skills shortage in a poorly functioning market rather than accept the rise of middle class power couples outbidding them in the hire of domestic help. As Alchian and Arrow (1958, pp. 39-40) explain:

… Many people who formerly consumed some of the commodity or service in question and now find the price so high that they no longer want as much (or any) would describe the situation is one of “shortage”.

Actually, this is merely one way of saying that they can’t get the given commodity at its old price.

We can think of many examples of this use of the word “shortage”. For example, the “servant shortage” during World War II was a case in point.

Those with whom the increase in household servants wages were more than they could afford to pay, apparently found it more convenient to describe their change in circumstances as a result of a “shortage” than to admit baldly that they couldn’t afford to keep the servants…

It seems reasonable to explain a good deal of the current complaint about a shortage of scientists and engineers is a variant of the “servant shortage” phenomena.

Employers who find themselves losing engineers to other firms and at the same time find it uneconomic to try and keep these employees by offering them substantial salary increases may see the situation as a “shortage” rather than recognise that other firms can put these skills to more valuable uses…

While we lack specific evidence, we have the impression that the firms who have complained most consistently about “shortage” have been those whose demand has not increased or at least not increased as rapidly as that of other firms in their industry.

Why are people priced out of any market? Given a fixed income and the many other alternative uses of their incomes, any rise in price makes buying the old quantity no longer the best bargain.

Who will admit that they can no longer keep themselves in the style they were accustomed to when they complain of market failure, skill shortages and lack of government investment in skill formation.

Alfred Marshall’s comparative statics of price adjustment

The analysis of the time path of price adjustment for any commodity was developed by Alfred Marshall in 1890. He was concerned that time was an important factor in how the markets adjusted to demand and supply changes:

… markets vary with regard to the period of time which is allowed to the forces of demand and supply to bring themselves into equilibrium with one another, as well as with regard to the area over which they extend. And this element of Time requires more careful attention just now than does that of Space.

For the nature of the equilibrium itself, and that of the causes by which it is determined, depend on the length of the period over which the market is taken to extend.

We shall find that if the period is short, the supply is limited to the stores which happen to be at hand: if the period is longer, the supply will be influenced, more or less, by the cost of producing the commodity in question; and if the period is very long, this cost will in its turn be influenced, more or less, by the cost of producing the labour and the material things required for producing the commodity.

Marshall divided the price adjustment process into the market period, the short run, and the long run.

In the market period, production is fixed; and all factors of production are fixed in supply during this time period. The burden of price adjustment is on the demand side.

As the supply is fixed in the market period, it is shown as a vertical line SMP. It is also called as inelastic supply curve. When demand increases from DD to D1 D1, price increases from P to P1. Similarly, a fall in demand from DD to D2 D2 pull the price down from P to P2.

In the short run, supply to be partially adaptable, in the sense that increased production can occur but capital equipment and certain other overhead items are held constant.

SSP is elastic implying that supply can be increased by changing a variable input. Note that the corresponding increase in price from P to P1 for a given increase in demand from D to D1 is less than in the market period. It is because the increase in demand is partially met by the increase in supply from q to q1.

The short run is the conceptual time period in which at least one factor of production is fixed in amount and others are variable in amount. In the short run, a profit-maximising firm will:

- increase production if marginal cost is less than marginal revenue;

- decrease production if marginal cost is greater than marginal revenue;

- continue producing if average variable cost is less than price per unit, even if average total cost is greater than price;

- Shut-down if average variable cost is greater than price at each level of output.

In the long run, supply is fully flexible – there are no fixed factors of production. The Marshallian long-run allows for optimal capital stock adjustment.

The long period supply curve SLP is more elastic and flatter than that of the SSP. This implies the greater extent of flexibility of the firms to change the supply.

The price increases from P to P2 in response to an increase in demand from D to D1 and it is less than that of the market period (P1) and short period (P2). It is because the increase in demand is fully met by the required increase in supply. Hence, supply plays a significant role in determining the lower equilibrium price in the long run.

The market is cleared in the long run within a framework in which supply can be considered to be fully adaptable because all factors have adjusted to the new situation. Alfred Marshall explains:

In long periods on the other hand all investments of capital and effort in providing the material plant and the organization of a business, and in acquiring trade knowledge and specialized ability, have time to be adjusted to the incomes which are expected to be earned by them: and the estimates of those incomes therefore directly govern supply, and are the true long-period normal supply price of the commodities produced.

In addition, in the market period, the short run, and the long run, foresight is not perfect, information is not free, and the cost of adjusting something is not independent of the speed in which you wish to do so.

The 2nd laws of supply and of demand

Another way to discuss how time interacts with responsiveness of supply and demand are the second laws of supply and demand.

The Second Law of Supply states that supply is more responsive to price in the long run. The Second Law of Supply relates to how flexible producers are in terms of how much of a good they produce.

Supply is more elastic in the long run because given more time, producers can more easily adapt to the change in the price.

Within shorter periods of time, producers cannot as easily change the amount of a good they produce (since changes in production often require adjustments within factories, with workers etc.)

The Second Law of Demand states that demand is more responsive to price in the long run than in the short run. Initially, when the price of a good increases or decreases, consumption does not change drastically. However, when consumers are given more time to react to the change in price, consumption can either increase or decrease more dramatically. Demand is not only determined by price but also factors such as: income, tastes, and the price of related goods.

In the market period, any adjustment must be made through changes in price. This means that there could be initially a large price increase.

In the short run, there are some capability for more supply to come forward. This additional supply will temper the initial large price increase.

In the long run, producers are fully able to adapt their circumstances to the changing market conditions and higher prices. This will reduce prices as compared to the initial price spike when market conditions first changed.

In the long run, new firms can enter the industry and old firms can exit as required by the price change and their entrepreneurial expectations of the future of the industry.

Search and matching in a decentralised labour market

To cover off the bases, the simultaneous existence of vacancies and unemployed in a labour market is no evidence of either of surplus or shortage. It takes time for workers to locate vacancies and assess their competing job options. It takes time for employers to locate suitable workers to fill vacancies.

The simultaneous existence of vacancies and unemployed is the result of, as mentioned earlier, imperfect foresight, the fact that information is not free, nor freely available, and the costs of doing anything is not independent of the speed in which you wish to act. Searching for suitable vacancies, or suitable employees, is costly, and neither jobseeker nor employer knows whether any match will work out.

The one-price (one-wage) market that clears instantly will occur only where the cost of information about the prices (wages) offered by buyers and sellers is zero. As George Stigler observed in the opening paragraph of his famous 1961 paper The Economics of Information:

One should hardly have to tell academicians that information is a valuable resource: knowledge is power. And yet it occupies a slum dwelling in the town of economics.

Mostly it is ignored: the best technology is assumed to be known, the relationship of commodities to consumer preferences is a datum.

And one of the information producing industries, advertising, is treated with a hostility that economists normally reserve for tariffs or monopolists.

Job search cost are of two types: direct costs of gathering information about competing opportunities and the opportunity cost of being unemployed or staying in your current job at your current pay.

- The benefit from job search is the expected gain in earnings that will result from waiting for a better wage offer.

- The rational job searcher searches for better offers until the marginal benefit and cost of additional search are equal.

- A significant cost of continued job search is the earnings foregone by not taking the previous best opportunity.

Unemployment can be a cost-effective method of searching for better employment opportunities and higher wage offers as David Andolfatto observed:

One frequently reads that “unemployment represents wasted resources.”

But if job search is an information-gathering activity, designed to locate a high quality job match, in what sense does such an activity necessarily constitute wasted resources? (Does the existence of single people in the marriage market also represent wasted resources?)

If the unemployment rate were to suddenly plummet because a large number of workers aborted their job search activity–accepting crappy jobs, or exiting the labour force–is this a reason to celebrate?

The behavioural responses of employers and workers to change are so pronounced because the cost of acquiring new information is profound (Alchian 1969). Many such costs impede wages from instantly fluctuating to rebalance labour supply with demand. Hicks (1932) explained this uncertainty and state of flux as follows:

For although the industry as a whole is stationary, some firms in it will be closing down or contracting their sphere of operations, others will be arising or expanding to take their place.

Some firms then will be dismissing, others taking on, labour; and when they are not situated close together, so that knowledge of opportunities is imperfect, and transference is attended by all the difficulties of finding housing accommodation, and the uprooting and transplanting of social ties, it is not surprising that an interval of time elapses between dismissal and re-engagement, during which the workman is unemployed.

A job seeker does not initially know the location of suitable vacancies, the wages for various skills, differences in job security and other factors. Job seekers must search for this information, keep this knowledge current and forecast whether better vacancies may open soon. Employers must search to learn the location, availability and asking wages of applicants. There is a tendency for unpredicted wage changes to induce costly additional job search. Long-term contracts arise to share risks and curb opportunism over sunken investments in relationship-specific human and organisation capital. These factors all lead to queues, unemployment, spare capacity, layoffs, shortages, inventories and non-price rationing in conjunction with wage stability (Alchian 1969; Alchian and Allen 1967, 1973; Klein 1984; Hashimoto and Yu 1980; Hall and Lazear 1979).

By acquiring more information, a job seeker learns more about their options and can improve their prospects of finding better-paid job matches. Job seekers and employers invest time and resources to find one another, size each other up and form a job match or try their luck elsewhere. A job match is a pairing of a worker with a particular employer.

Job seekers will apply for a portfolio of job vacancies that reflect their asking wage and their known alternatives. An asking wage is the minimum that a job seeker is willing to accept given their options.

- The extent of job search depends on the costs of job-information production and acquisition, the income available to job seekers while searching, the frequency and the magnitude of shifts in the relative demand between different sectors, the costs of relocation and retraining, and the extent and frequency of declines in aggregate demand (Alchian and Allen 1967).

- The more varied will be the potential job opportunities and the greater will be the gains to job seekers from continued job search, the greater are the rate of change in tastes and demand, the greater are the differences in the skills of job seekers and the requirements of job vacancies, and the greater are the costs of moving (Alchian and Allen 1967).

Employers face an information dilemma as well. If they wait a bit longer, hold a job vacancy open, a better job applicant may come a long and a more profitable and longer lasting job match may result.

Of course, the employer is taking a chance here on the job applicant pool improving with time. There are elements of luck involved for both employers and job seekers when filling vacancies and finding jobs.

The employer must balance the costs of holding the vacancy open with his estimation of the value and probability of a better applicant applying at a later date if he searches further the prospective recruits. But reducing your ignorance has costs as Stigler (1961) explained:

Ignorance is like sub-zero weather: by a significant expenditure its effects upon people can be kept within tolerable or even comfortable bounds, but it would be wholly uneconomical entirely to eliminate all its effects.

The rate at which job vacancies are filled and the rate at which people leave unemployment and change jobs is determined by the job search decisions of job seekers and the recruitment decisions of employers. The way in which the process works is well explained by Andolfatto’s analogy to the marriage market:

In many ways, the labour market resembles a matching market for couples.

That is, one is generally aware that the opposite side of the market consists of better and worse matches (we seldom take the view that there are no potential matches).

The exact location of the better matches is unknown, but may be discovered with some effort.

In the meantime, it may make sense to refrain from matching with ‘substandard’ opportunities that are currently available.

But since search is costly, it will generally not be optimal to wait for ones “soul mate” to come along. Furthermore, since relationships are not perfectly durable, there is no reason to expect the stock of singles to converge to zero over time

As in the labour market, there are marriages and divorces and young people come of age and look for the first time; people also link up for short-term relationships; and some relationships do better than others.

To say there is involuntary unemployment is to say there is also involuntarily unmarried people. But we can always marry the first person we meet in the street, if they’ll have us. Search and matching is a two sided affair. I doubt that our first encounter in the street would accept this offer of marriage from a stranger. I doubt that anyone would want to marry a stranger who would so willingly marry a stranger. I think both sides suspect that such a random pairing would not last long because the pairing occurred after so little mutual scrutiny and measured assessment of alternatives, current and prospective. The same principles apply to search and matching in the labour market.

Is unemployment voluntary or involuntary?

27 Jun 2014 Leave a comment

in business cycles, job search and matching, labour economics, macroeconomics, unemployment Tags: Alan Manning, Armen Alchian, Robert Barro, Robert Lucas, unemployment

Robert Lucas in a famous 1978 paper argued that all unemployment was voluntary because involuntary unemployment was a meaningless concept. He said as follows:

The worker who loses a good job in prosperous time does not volunteer to be in this situation: he has suffered a capital loss. Similarly, the firm which loses an experienced employee in depressed times suffers an undesirable capital loss.

Nevertheless the unemployed worker at any time can always find some job at once, and a firm can always fill a vacancy instantaneously. That neither typically does so by choice is not difficult to understand given the quality of the jobs and the employees which are easiest to find.

Thus there is an involuntary element in all unemployment, in the sense that no one chooses bad luck over good; there is also a voluntary element in all unemployment, in the sense that however miserable one’s current work options, one can always choose to accept them.

I agree that we all make choices subject to constraints. To say that a choice is involuntary because it is constrained by a scarcity of job-opportunities information is to say that choices are involuntary because there is scarcity.

Alchian said there are always plenty of jobs because to suppose the contrary suggests that scarcity has been abolished. Lucas elaborated further in 1987 in Models of Business Cycles:

A theory that does deal successfully with unemployment needs to address two quite distinct problems.

One is the fact that job separations tend to take the form of unilateral decisions – a worker quits, or is laid off or fired – in which negotiations over wage rates play no explicit role.

The second is that workers who lose jobs, for whatever reason, typically pass through a period of unemployment instead of taking temporary work on the ‘spot’ labour market jobs that are readily available in any economy.

Of these, the second seems to me much the more important: it does not ‘explain’ why someone is unemployed to explain why he does not have a job with company X. After all, most employed people do not have jobs with company X either.

To explain why people allocate time to a particular activity – like unemployment – we need to know why they prefer it to all other available activities: to say that I am allergic to strawberries does not ‘explain’ why I drink coffee. Neither of these puzzles is easy to understand within a Walrasian framework, and it would be good to understand both of them better, but I suggest we begin by focusing on the second of the two.

Another way to understand unemployment is to use a device at the start of Alan Manning’s book on labour market monopsony:

What happens if an employer cuts the wage it pays its workers by one cent? Much of labour economics is built on the assumption that all existing workers immediately leave the firm as that is the implication of the assumption of perfect competition in the labour market.

In such a situation an employer faces a market wage for each type of labour determined by forces beyond its control at which any number of these workers can be hired but any attempt to pay a lower wage will result in the complete inability to hire any of them at all

Suppose workers offered to work for 1 cent. Would employers accept? Many do because they have intern and work experience programmes for students, but is this result of general application?

Understanding the reallocation of labour at the end of the recession requires careful attention to the 1980s writing of Alchian on the theory of the firm. Alchian and Woodward’s 1987 ‘Reflections on a theory of the firm’ says:

… the notion of a quickly equilibrating market price is baffling save in a very few markets. Imagine an employer and an employee. Will they renegotiate price every hour, or with every perceived change in circumstances?

If the employee is a waiter in a restaurant, would the waiter’s wage be renegotiated with every new customer? Would it be renegotiated to zero when no customers are present, and then back to a high level that would extract the entire customer value when a queue appears?

… But what is the right interval for renegotiation or change in price? The usual answer ‘as soon as demand or supply changes’ is uninformative.

Alchian and Woodward then go on to a long discussion of the role of protecting composite quasi-rents from dependent resources as the decider of the timing of wage and price revisions.

Alchian and Woodward explain unemployment as a side-effect of the purpose of wage and price rigidity, which is the prevention of hold-ups over dependent assets. They note that unemployment cannot be understood until an adequate theory of the firm explains the type of contracts the members of a firm make with one another.

My interpretation is the majority of employment relationships are capital intensive long-term contracts. Employers spend a lot of time searching and screening applicants to find those that will stay longer. In less skilled jobs, and in spot market jobs, employers will hire the best applicant quickly because job turnover costs are low. Back to Manning again:

That important frictions exist in the labour market seems undeniable: people go to the pub to celebrate when they get a job rather than greeting the news with the shrug of the shoulders that we might expect if labour markets were frictionless. And people go to the pub to drown their sorrows when they lose their job rather than picking up another one straight away. The importance of frictions has been recognized since at least the work of Stigler (1961, 1962).

Whatever may be among these frictions, wage rigidity is not one of them. Wages are flexible for job stayers and certainly new starters.

See What can wages and employment tell us about the UK’s productivity puzzle? by Richard Blundell, Claire Crawford and Wenchao Jin showing that in the recent UK recession 12% of employees in the same job as 12 months ago experienced wage freezes and 21% of workers in the same job as 12 months ago experienced wage cuts. Their data covered 80% of workers in the New Earnings Survey Panel Dataset.

Larger firms lay off workers; smaller firms tended to reduce wages. This British data showing widespread wage cuts dates back to the 1980s. Recent Irish data also shows extensive wage cuts among job stayers.

See too Chris Pissarides (2009), The Unemployment Volatility Puzzle: Is Wage Stickiness the Answer? arguing the wage stickiness is not the answer since wages in new job matches are highly flexible:

- wages of job changers are always substantially more procyclical than the wages of job stayers.

- the wages of job stayers, and even of those who remain in the same job with the same employer are still mildly procyclical.

- there is more procyclicality in the wages of stayers in Europe than in the United States.

- The procyclicality of job stayers’ wages is sometimes due to bonuses, and overtime pay but it still reflects a rise in the hourly cost of labour to the firm in cyclical peaks

How do existing firms who will not cut wages survive in competition with new firms who can start workers on lower wages? Industries with many short term jobs and seasonal jobs would suffer less from wage inflexibility.

Robert Barro (1977) pointed out that wage rigidity matters little because workers can, for example, agree in advance that they will work harder when there is more work to do—that is, when the demand for a firm’s product is high—and work less hard when there is little work. Stickiness of nominal wage rates does not necessarily cause errors in the determination of labour and production.

The ability to make long-term wage contracts and include clauses that guard against opportunistic wage cuts should make the parties better off. Workers will not sign these contracts if they are against their interests. Employers do not offer these contracts, and offer more flexible wage packages, will undercut employers who are more rigid. Furthermore many workers are on performance pay that link there must wages to the profitability of the company.

How can downward wage rigidity be a scientific hypothesis if extensive international evidence of widespread wage cuts since the 1980s and 30%+ of the workforce on performance bonuses is not enough to refute it?

Alchian and Kessel in “The Meaning and Validity of the Inflation-Induced Lag of Wages Behind Prices,” Amer. Econ. Rev. 50 [March 1960]:43-66) tested the hypothesis that workers suffered from money illusion by comparing the rates of return to firms in capital intensive industries with those of labour intensive industries. Labour intensive industries were not more profitable than capital intensive industries. Employers in labour intensive industries should profit from the misperceptions of workers about wages and future prices, but they did not. Alchian and Kessel found little evidence of a lag between wage and price changes.

In Canadian industries in the 1960s and 1970s, wage indexation ranged from zero to nearly 100%. Industries with little indexation should show substantial responses of real wage rates, employment and output to nominal shocks. Industries with lots of indexation would be affected little by nominal disturbances. Monetary shocks had positive effects but an industry’s response to these shocks bore no relation to the amount of indexation in the industry. Shaghil Ahmed (1987) found that those industries with lots of indexation were as likely as those with little indexation to respond to shocks.

If the signing of new wage contracts was important to wage rigidity, there should be unusual behaviour of employment and real wage rates just after these signings, but the results are mixed. Olivei and Tenreyro (2010) used the tendency of contracts to be signed at the start of years to show that monetary policy had significant effects in January but little effect in December because the effects were quickly undone.

Alchian (1969) lists three ways to adjust to unanticipated demand fluctuations:

• output adjustments;

• wage and price adjustments; and

• Inventories and queues (including reservations).

Alchian (1969) suggests that there is no reason for wage and price changes to be used regardless of the relative cost of these other options:

• The cost of output adjustment stems from the fact that marginal costs rise with output;

• The cost of price adjustment arises because uncertain prices and wages induce costly search by buyers and sellers seeking the best offer; and

• The third method of adjustment has holding and queuing costs.

There is a tendency for unpredicted price and wage changes to induce costly additional search. Long-term contracts including implicit contracts arise to share risks and curb opportunism over relationship-specific capital. These factors lead to queues, unemployment, spare capacity, layoffs, shortages, inventories and non-price rationing in conjunction with wage stability.

Austrian economics, labour economics and the economics of unemployment

18 Jun 2014 Leave a comment

in Austrian economics, labour economics, macroeconomics, Murray Rothbard Tags: Armen Alchain, FA Hayek, Israel Kirzner, Ludwig von Mises, Murray Rothbard, unemployment

Austrian economists seem not to be as thorough as they could be in applying the concepts of dispersed knowledge, tendency to equilibrium and entrepreneurial appraisal, discovery and learning to the labour market.

In a nutshell, the position of Mises and Rothbard is the problem of unemployment is not jobs being fewer than workers. On some terms, a job is always available in an open market. But a wage and the hours of labour required to earn it can be so unrewarding that a person is rational to decline the job offer and remain unemployed. Of course, they acknowledge institutional unemployment that results from are laws and arrangements which inhibit adjustment of prices of labour services.

Kirzner and Rothbard argue that the market is a process that is always in disequilibrium. Does this disequilibrium not imply some unemployment in the labour market? Why should the tendency toward equilibrium be any stronger in the labour market that elsewhere? Bill Allen explained search unemployment this way:

…many officially counted as unemployed are heavily and rationally investing their resources in looking for work. They are sampling the market, seeking information on employment alternatives. That information is valuable, but it is not obtained either freely or instantaneously, and generally, the faster it is to be acquired, the more costly it will be…

as output falls [because of a demand or supply shock], there will be some rise in unemployment, for the economy’s adjustment to the new circumstances of supply and prices will not be made instantaneously, without frictions and lags.

Rothbard was well aware of search unemployment:

It might be objected that workers often do not know what job opportunities await them. This, however, applies to the owner of any goods up for sale. The very function of marketing is the acquisition and dissemination of information about the goods or services available for sale.

Except to those writers who posit a fantastic world where everyone has “perfect knowledge” of all relevant data, the marketing function is a vital aspect of the production structure.

The marketing function can be performed in the labour market, as well as in any other, through agencies or other means for the discovery of who or where the potential buyers and sellers of a particular service may be. In the labour market this has been done through “want ads” in the newspapers, employment agencies used by both employer and employee, etc.

Mises also spoke of search unemployment:

Unemployment is a phenomenon of a changing economy. The fact that a worker discharged on account of changes occurring in the arrangement of production processes does not instantly take advantage of every opportunity to get another job but waits for a more propitious opportunity is not a consequence of the tardiness of the adjustment to the change in conditions, but is one of the factors slowing down the pace of this adjustment.

It is not an automatic reaction to the changes which have occurred , independent of the will and the choices of the job-seekers concerned, but the effect of their intentional actions. It is speculative, not frictional

These are good discussions of search unemployment. But when discussing mismatch unemployment as identified by Hayek after a shortening of the production structure on the market where there might be temporary unemployment of workmen in the higher stages, lasting until the workers can be reabsorbed in the shorter processes of the later stages, Rothbard’s repost to this possible case of involuntary unemployment on the free market is:

It is also true that the shortening of the structure means that there is a transition period when, at final wage rates, there will be unemployment of the men displaced from the longer processes. However, during this transition period there is no reason why these workers cannot bid down wage rates until they are low enough to enable the employment of all the workers during the transition. This transition wage rate will be lower than the new equilibrium wage rate. But at no time is there a necessity for unemployment.

The labour market is a process just as is any other market: it is a communication network that mobilises dispersed knowledge to overcoming ignorance. Why should knowledge unfold in the labour market process through entrepreneurial discovery any faster than elsewhere? There should be disequilibrium wages, entrepreneurial errors, unemployed and mispriced resources, and a process of entrepreneurial learning and error correction. Hayek held that unemployment is always a pricing problem:

The normal cause of recurrent waves of widespread unemployment is … a discrepancy between the way in which demand is distributed between products and services, and the proportions in which resources are devoted to producing them.

Unemployment is the result of divergent changes in the direction of demand and the techniques of production. If labour is not deployed according to demand for products, there is unemployment…

It is the continuous change of relative market prices and particularly wages which can alone bring about that steady adjustment of the proportions of the different efforts to the distribution of demand, and thus a steady flow of the stream of products.

True, but the correction of erroneous wage rates and the reallocation of labour and other resources to new jobs, new firms and new industries is neither instantaneous nor a free process. Kirzner explains:

The entrepreneurial forces acting on the market for any one commodity are thus continually pushing that market toward the market-clearing point—that is, to where (a) the quantity produced is such that (only) all units “worth producing” are indeed produced, and (b) the market price for this commodity is just high enough to make it, as a practical matter, worthwhile for producers to produce this quantity, and is just low enough to make it worthwhile for consumers to buy it…

The process through which the market tends to generate the “right” quantity of a commodity, and the “right” price for it, can be seen as a series of steps during which market participants gradually tend to discover the gaps or errors in the information on which they had previously been basing their erroneous production and/or buying decisions…

The market process is one in which, driven by the entrepreneurial sense for grasping at pure profit opportunities (and for avoiding entrepreneurial losses), market participants, learning more accurate assessments of the attitudes of other market participants, tend toward the market-clearing price-quantity combination.

Alchian, Demsetz and Barzel were on the mark when they pointed out that too frequently the process of change and reaching a new equilibrium is assumed to be a free good, having no resource costs. Hayek also spoke of the time that is takes to reach a new equilibrium because the new constellation of prices and wages must emerge through the free-play of the market:

The primary cause of the appearance of extensive unemployment, however, is a deviation of the actual structure of prices and wages from its equilibrium structure. Remember, please: that is the crucial concept. The point I want to make is that this equilibrium structure of prices is something which we cannot know beforehand because the only way to discover it is to give the market free play; by definition, therefore, the divergence of actual prices from the equilibrium structure is something that can never be statistically measured.

As Kirzner has well argued, entrepreneurs thrive on alertness to disequilibrium prices and they buy and sell to profit from their discoveries, thereby correcting the mispricing, but this takes time. The knowledge and intentions of the different members of society both across all markets and in the labour market about how to match workers to new jobs must come into agreement through a process of discovery and mutual learning that takes time. Phelps (1969) put forward a fine metaphor for how this process of learning and discovery takes place:

I have found it instructive to picture the economy as a group of islands between which information flows are costly: to learn the wage paid on an adjacent island, the worker must spend the day travelling to that island to sample its wage instead of spending the day at work.

Beveridge has similar views of a multiplicity of markets in 1912:

Why should it be the normal condition of the labour market to have more sellers than buyers, two men to every job and at least as often two jobs for every man? The explanation of the paradox is really a very simple one … that there is no one labour market but only an infinite number of separate labour markets.

Gary Becker drew a parallel between the theory of marriage and the theory of job search and matching. In both cases, it takes time to sort among the options and find a suitable pairing. Some are clearly unacceptable. Good matches will often take a long time to find unless people are just plain lucky. Involuntary unemployment is like saying you are involuntarily unmarried. You could marry the first person you meet, if they will have you, but few would say that is wise.

Workers must search for and discover each other. Both are entrepreneurs. The information, knowledge and forecasts of future wages and prices each needs to improve co-ordination of supply and demand will not be discovered immediately:

- The behavioural responses of employers and workers to change are so pronounced because the cost of acquiring new information is profound (Alchian 1969). Many such costs impede wages from instantly fluctuating to rebalance labour supply with demand.

- A job seeker does not initially know the location of suitable vacancies, the wages for various skills, differences in job security and other factors. Job seekers must search for this information, keep this knowledge current and forecast whether better vacancies may open soon.

- Employers must search to learn the location, availability and asking wages of applicants.

The time consumed in labour market search is why Rothbard’s views below that wages just adjust to clear the market has been over taken by developments in economic thinking:

To talk of unemployment or employment without reference to a wage rate is as meaningless as talking of “supply” or “demand” without reference to a price. And it is precisely analogous. The demand for a commodity makes sense only with reference to a certain price.

In a market for goods, it is obvious that whatever stock is offered as supply, it will be “cleared,” i.e., sold, at a price determined by the demand of the consumers…

Whatever supply of labour service is brought to market can be sold, but only if wages are set at whatever rate will clear the market…

We conclude that there can never be, on the free market, an unemployment problem. If a man wishes to be employed, he will be, provided the wage rate is adjusted according.

Mises in the quote below treated unemployment as a investment in prospecting for a better wage offer very much along the lines of W.H. Hutt:

If a job-seeker cannot obtain the position he prefers, he must look for another kind of job. If he cannot find an employer ready to pay him as much as he would like to earn, he must abate his pretensions. If he refuses, he will not get any job. He remains unemployed.

What causes unemployment is the fact that–contrary to the above-mentioned doctrine of the worker’s inability to wait–those eager to earn wages can and do wait. A job-seeker who does not want to wait will always get a job in the unhampered market economy in which there is always unused capacity of natural resources and very often also unused capacity of produced factors of production. It is only necessary for him either to reduce the amount of pay he is asking for or to alter his occupation or his place of work.

Alchian (1969) lists three ways to adjust to unanticipated demand fluctuations:

• output adjustments;

• wage and price adjustments; and

• Inventories and queues (including reservations).

Alchian (1969) suggests that there is no reason for wage and price changes to be used regardless of the relative cost of these other options:

• The cost of output adjustment stems from the fact that marginal costs rise with output;

• The cost of price adjustment arises because uncertain prices and wages induce costly search by buyers and sellers seeking the best offer; and

• The third method of adjustment has holding and queuing costs.

There is a tendency for unpredicted price and wage changes to induce costly additional search. Long-term contracts including implicit contracts arise to share risks and curb opportunism over sunken investments in relationship-specific capital such as firm-specific human capital and specialised machinery. These factors lead to queues, unemployment, spare capacity, layoffs, shortages, inventories and non-price rationing in conjunction with wage stability. Alchian and Woodward in their 1987 paper ‘Reflections on a theory of the firm’ say that :

… the notion of a quickly equilibrating market price is baffling save in a very few markets. Imagine an employer and an employee. Will they renegotiate price every hour, or with every perceived change in circumstances? If the employee is a waiter in a restaurant, would the waiter’s wage be renegotiated with every new customer? Would it be renegotiated to zero when no customers are present, and then back to a high level that would extract the entire customer value when a queue appears?

… But what is the right interval for renegotiation or change in price? The usual answer ‘as soon as demand or supply changes’ is uninformative.

Alchian and Woodward then go on to a long discussion of the role of protecting composite quasi-rents from dependent resources as the decider of the timing of wage and price revisions. Alchian and Woodward explain unemployment to the side effect of the purpose of wage and price rigidity, which is the prevention of hold-ups over dependent assets. They note that unemployment cannot be understood until an adequate theory of the firm that explains the type of contracts the members of a firm contract with one another.

Walter Oi has also written on slack capacity as being productive and he included references back to W.H. Hutt. Oi’s work on retailing and supermarkets spends a lot of time explaining how an empty store is efficient because the owners are waiting for a mass of customers to arrive at unpredictable time. Oi redeveloped the term the economies of massed reserves to describe this. Oi thought that this was a better term than Hutt’s pseudo-idleness. Oi argued that all resource idleness could, in principle, be eliminated, but to accomplish this, the synchronization of the arrival rates of customers, sales clerks, and just-in-time inventories would be prohibitively expensive.

Benjamin Klein’s theory of rigid wages in American Economic Review in 1984 is one of the few that explored rigid wages as an industrial organisation issue. Klein treated rigid wages as a response to opportunism and hold-up problems over specialised assets and are forms of exclusive dealership or take-or-pay contracts.

The labour market is better understood by forgetting it is the labour market and treating it as a market for long-term contracts for relationship-specific services, firm-specific human capital and mutually dependent assets owned by multiple parties.

Labour is more heterogeneous than capital. The notion that buyers and sellers in the labour market can pair up instantly contradicts the Austrian traditions that markets only tend to equilibrium and entrepreneurs are needed to move things along.

Morgan O. Reynolds makes a good point in his labour economics textbook about how labour markets are different from other markets because there are no speculators and no forward markets in labour to quickly clear the market and allow entrepreneurs to drive the market towards equilibrium through arbitrage as quickly as they do elsewhere.

Recent Comments