“Economic Policy and Growth of Nation” – by Prof. Finn Kydland

24 Apr 2022 Leave a comment

in applied price theory, budget deficits, business cycles, economic growth, economic history, Euro crisis, fiscal policy, global financial crisis (GFC), great recession, growth disasters, history of economic thought, labour economics, labour supply, macroeconomics, monetary economics, public economics, unemployment Tags: real business cycles

Prescott shows a lot of contracting since the end of the tech bubble

27 Jan 2022 Leave a comment

in business cycles, economic growth, economic history, Edward Prescott, great recession, history of economic thought, macroeconomics, monetarism, monetary economics Tags: real business cycles

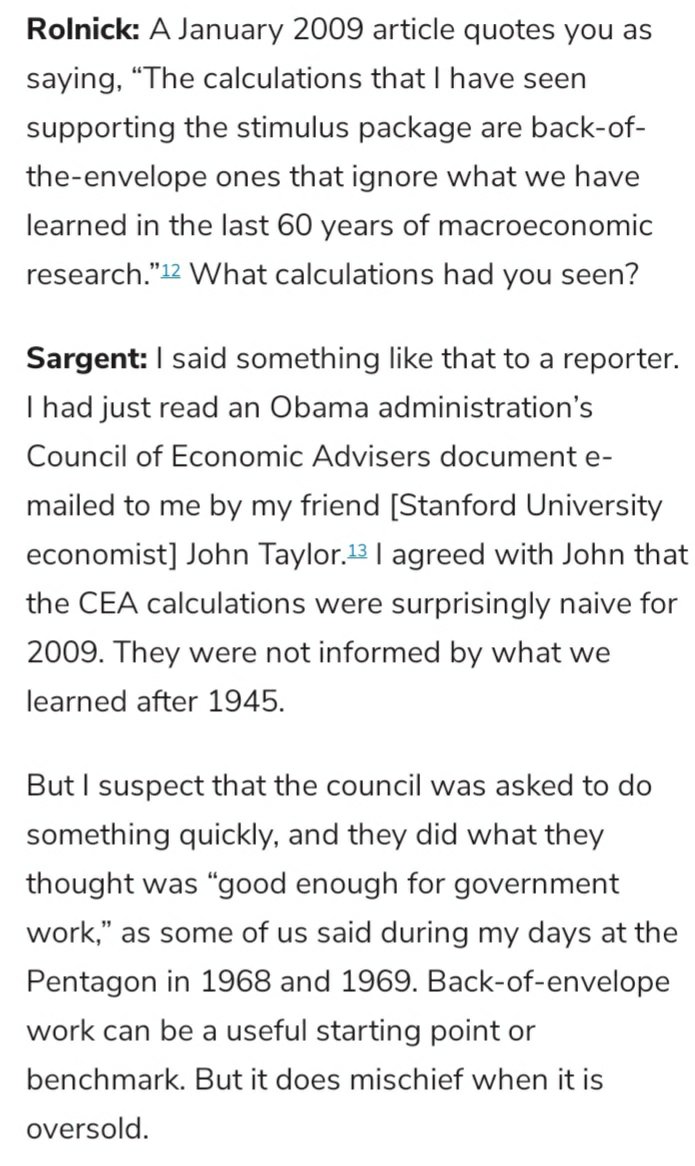

Ed Prescott Says ‘Partial’ Default Is Likely for Greece

22 Nov 2021 Leave a comment

in applied price theory, applied welfare economics, budget deficits, business cycles, comparative institutional analysis, currency unions, economic growth, economic history, Edward Prescott, Euro crisis, fiscal policy, global financial crisis (GFC), great recession, history of economic thought, labour economics, labour supply, macroeconomics, monetary economics, unemployment Tags: real business cycles

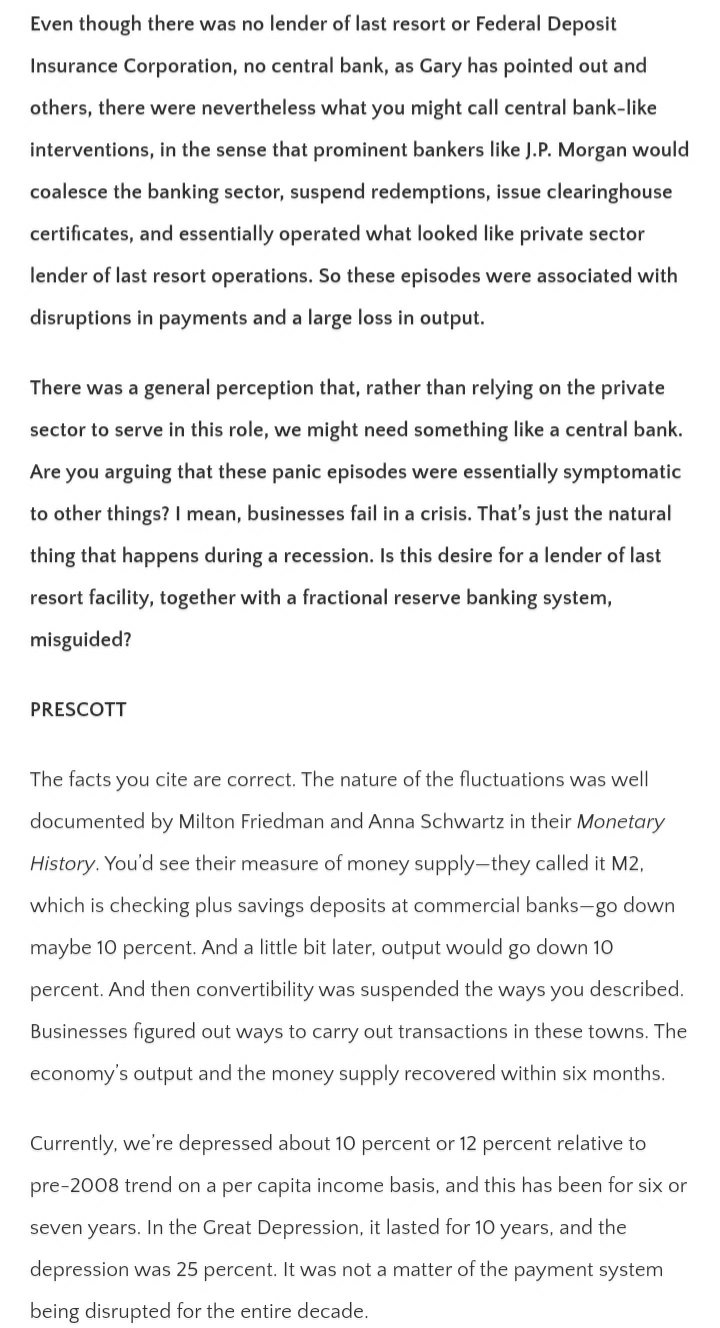

Edward C Prescott on the EU, business cycles and European economic research

20 Nov 2021 Leave a comment

in applied price theory, applied welfare economics, budget deficits, business cycles, economic history, Edward Prescott, Euro crisis, fiscal policy, global financial crisis (GFC), great recession, history of economic thought, industrial organisation, labour economics, labour supply, macroeconomics Tags: real business cycles

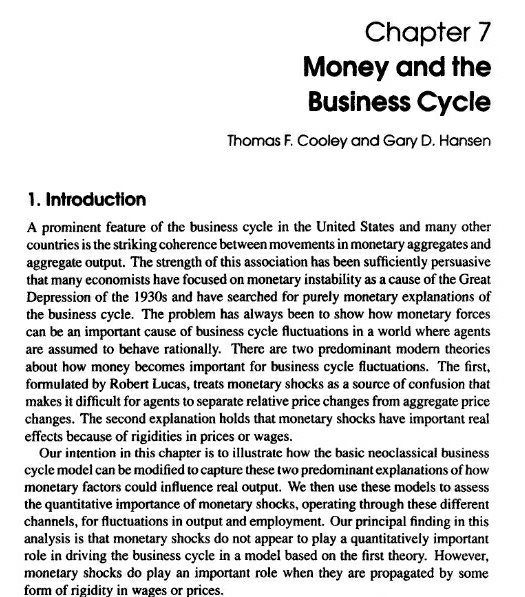

From Frontiers of Business Cycle Research 1995

07 Nov 2021 Leave a comment

in business cycles, econometerics, economic growth, economic history, Edward Prescott, labour economics, labour supply, macroeconomics, monetary economics, Robert E. Lucas Tags: monetary policy, real business cycles

Recent Comments