Hayek’s finest paper

16 Feb 2020 Leave a comment

in applied price theory, applied welfare economics, Austrian economics, comparative institutional analysis, economics of information, F.A. Hayek, history of economic thought, industrial organisation, property rights Tags: The fatal conceit, The meaning of competition, The pretence to knowledge

Angus Deaton Understanding and misunderstanding randomized controlled trials

16 Oct 2019 Leave a comment

in applied price theory, applied welfare economics, comparative institutional analysis, development economics, econometerics, economics of bureaucracy, economics of crime, economics of education, economics of information, growth disasters, health economics, labour economics, labour supply, law and economics, managerial economics, organisational economics, personnel economics, Public Choice, public economics, theory of the firm Tags: offsetting behaviour, The fatal conceit, The pretence to knowledge, unintended consequences

Tirole on the difficulties of network and utility regulation. Tradeoff between high cost, low profit firms v. low cost, high profit firms

16 Oct 2019 Leave a comment

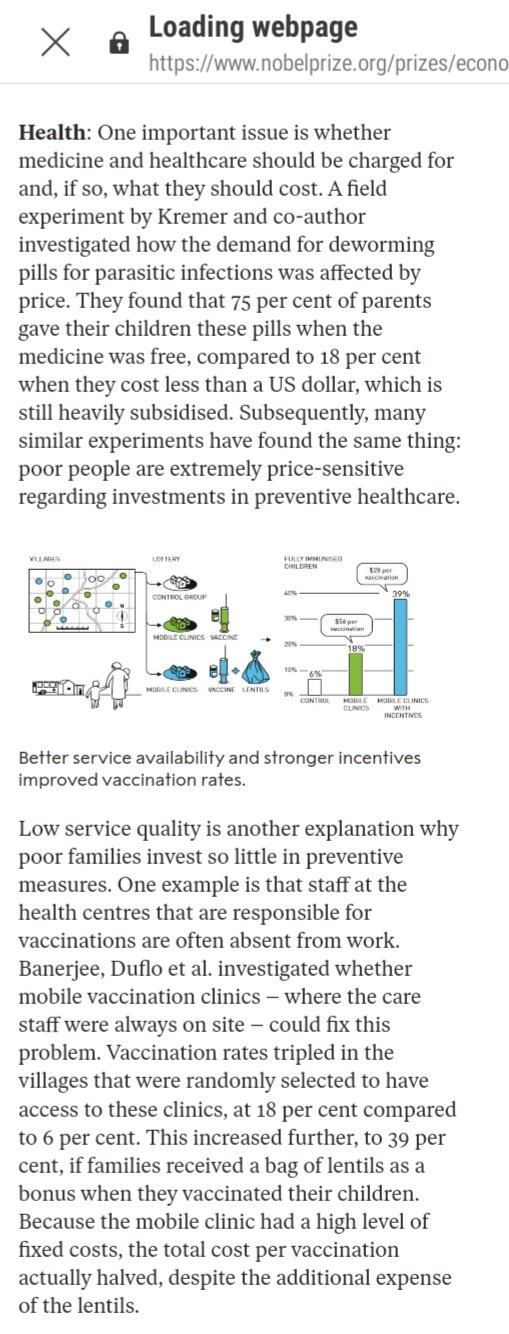

Nobel prize for discovering if you subsidise something, you see more of it!! Many years worth of randomized controlled trials just to make sure in dirt poor countries. Didn’t know child vaccination payoffs so marginal that you had to check.

15 Oct 2019 Leave a comment

in applied price theory, applied welfare economics, development economics, econometerics, economics of education, economics of information, growth disasters, growth miracles, health economics Tags: The fatal conceit, The pretence to knowledge

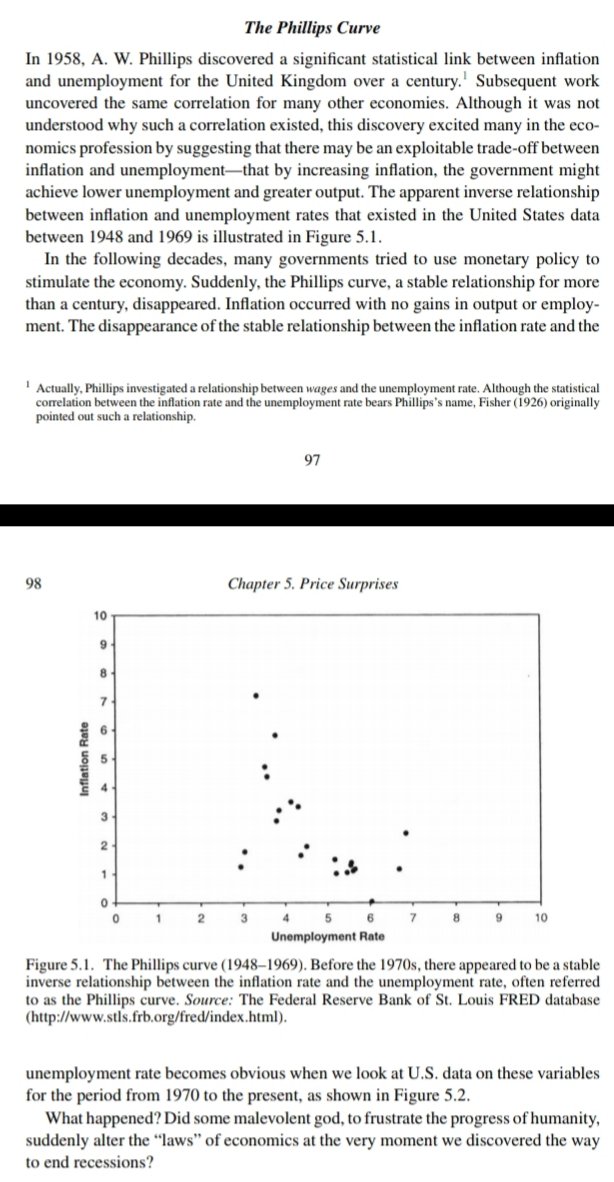

Scott Freeman and Bruce Champ on the Phillips Curve

07 Aug 2019 Leave a comment

in business cycles, economic history, macroeconomics, monetary economics, Robert E. Lucas, unemployment Tags: The pretence to knowledge

The Unfulfilled Promise of the Anti-Discrimination Laws

28 Jun 2019 Leave a comment

in applied price theory, comparative institutional analysis, constitutional political economy, discrimination, economic history, entrepreneurship, industrial organisation, labour supply, law and economics, politics - USA, Richard Epstein, survivor principle Tags: racial discrimination, sex discrimination, The fatal conceit, The pretence to knowledge

Hayek and Robert Bork Part II on intellectuals, the impossibility of sociology and generality

25 May 2019 Leave a comment

in Austrian economics, economic history, economics of education, economics of information, economics of regulation, F.A. Hayek, history of economic thought, law and economics, occupational choice, politics - USA, property rights, Public Choice, Rawls and Nozick Tags: The fatal conceit, The pretence to knowledge

Central planning on steroids

13 Nov 2018 Leave a comment

in economics of education, human capital, labour economics, Marxist economics, occupational choice Tags: China, economics of central planning, The fatal conceit, The pretence to knowledge

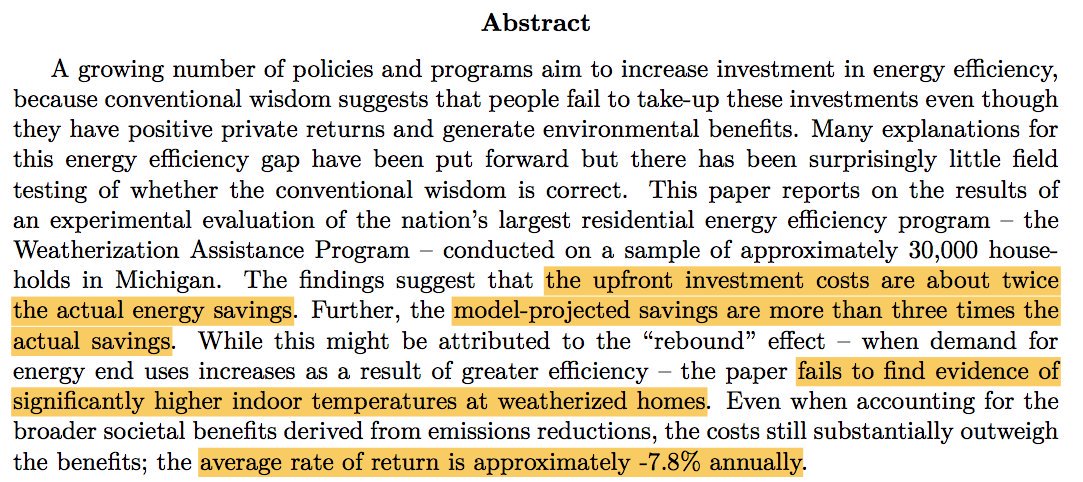

Energy efficiency investments are inefficient

29 Aug 2018 Leave a comment

in applied price theory, applied welfare economics, energy economics, environmental economics Tags: offsetting behaviour, The fatal conceit, The pretence to knowledge, unintended consequences

Robert Lucas on the utopianism of most economic advisors

23 Aug 2018 Leave a comment

in applied price theory, applied welfare economics, comparative institutional analysis, economics of bureaucracy, history of economic thought, Public Choice, Robert E. Lucas Tags: The pretence to knowledge

Tough choice

23 Aug 2018 Leave a comment

in economics of regulation, environmental economics Tags: nanny state, The pretence to knowledge, unintended consequences

The Time France Used Metric Time

21 May 2018 Leave a comment

in economic history, economics of information, economics of religion Tags: metric system, The pretence to knowledge

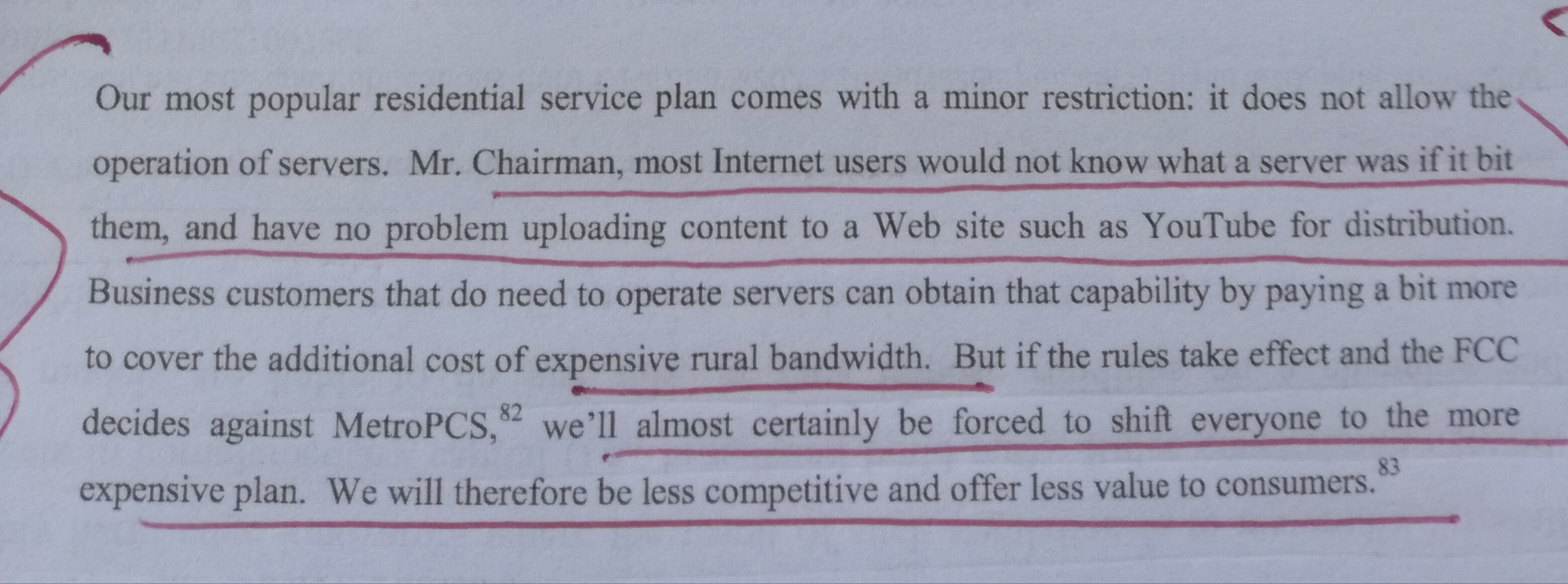

Co-op founder expains impact of net neutrality on a small ISP

17 Dec 2017 Leave a comment

in applied price theory, economics of media and culture, economics of regulation, industrial organisation, politics - New Zealand, politics - USA, survivor principle Tags: net neutrality, The fatal conceit, The pretence to knowledge, unintended consequences

Adam Smith and the Follies of Central Planning

20 Jun 2016 Leave a comment

in Adam Smith, applied price theory, applied welfare economics, Austrian economics, comparative institutional analysis, constitutional political economy, development economics, history of economic thought, Public Choice Tags: central planning, The fatal conceit, The pretence to knowledge

Recent Comments