Macros With Mythili – With Nobel Prize Winning Economist Finn Kydland

08 Jun 2019 Leave a comment

in budget deficits, business cycles, comparative institutional analysis, economic growth, history of economic thought, macroeconomics, monetary economics, Public Choice Tags: game theory, time inconsistency

Finn E. Kydland, Economic Policy and Sustainable Growth

09 May 2019 Leave a comment

in budget deficits, business cycles, comparative institutional analysis, development economics, economic growth, fiscal policy, law and economics, macroeconomics, property rights Tags: time inconsistency

Prescott Says ‘Partial’ Default Is Likely for Greece”

23 Nov 2018 Leave a comment

in budget deficits, business cycles, economic growth, Edward Prescott, Euro crisis, fiscal policy, global financial crisis (GFC), great recession, macroeconomics, Public Choice, public economics Tags: time inconsistency

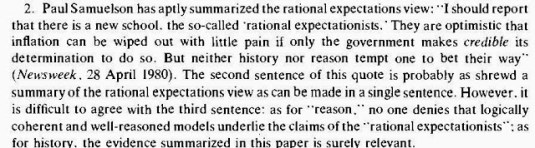

The shrewdest summary of rational expectations economic policy was by Paul Samuelson

02 Feb 2015 Leave a comment

in business cycles, fiscal policy, inflation targeting, macroeconomics, monetary economics Tags: new classical macroeconomics, Paul Samuelson, policy credibility, rational expectations, regime uncertainty, Stephen Williamson, time inconsistency, Tom Sargent

Many people are far too smart to save for their retirements

01 May 2014 Leave a comment

in applied welfare economics, macroeconomics Tags: Edward Prescott, fatal conceit, offsetting behavior, Other people are stupid fallacy, pretense to knowledge, retirement savings, time inconsistency

Which is better? Save for your retirement through the share market or save to own your own home and then present yourself at the local social security office to collect your taxpayer funded old-age pension?

Under this fine game of bluff, you bleed the taxpayer in your old age and pass on your debt-free home to your children.

This strategy is rational for the less well-paid. The family home is exempt from Income and asset testing for social security. If you lose you bet, sell your house and live off the capital.

For ordinary workers, this is a good bet. The middle class might prefer to live in a more luxurious retirement.

For ordinary workers, whose wages are not a lot more than their old age pension from the government, a government funded pension is a good political gamble. The old-age pension for a couple in New Zealand is set at no less that 60% of average earnings.

Compulsory savings for retirement requires the middle class to do what they can afford to do and would have done anyway.

Compulsory savings for retirement requires the working class to do what they can less afford to do.

Instead compulsory retirement savings deprives them of an old-age pension paid for by the taxes of the middle class.

In Australia, ordinary workers are required by law to save 9% of their wages for their retirements at 65 before they have had a chance to save for a car or a house or the rest of the condiments of life the middle class take for granted.

Edward Prescott argues for compulsory retirement savings account albeit with important twists because it is otherwise irrational for many to save for their retirement:

The reason we need to have mandatory retirement accounts is not because people are irrational, but precisely because they are perfectly rational — they know exactly what they are doing.

If, for example, somebody knows that they will be cared for in old age — even if they don’t save a nickel — then what is their incentive to save that nickel? Wouldn’t it be rational to spend that nickel instead?

…Without mandatory savings accounts we will not solve the time-inconsistency problem of people under-saving and becoming a welfare burden on their families and on the taxpayers. That’s exactly where we are now.

Prescott’s proposals are age specific. Those younger than 25 are not required to save anything because they are more pressing priorities such as buying cars and other consumer durables:

- Before age 25, workers would have no mandatory government retirement savings.

- Beginning at age 25, workers would contribute 3% vis-à-vis the current 10.6%.

- At age 30, that rate would increase to 5.3 percent.

- At 35, the rate would equal the full 10.6 percent.

- Upon retirement, there would be an annuity over the remaining lives of the individual and spouse

Most of all, the retirement savings must go into private savings accounts. These savings remain assets of the individual and therefore the compulsory savings requirements is not a tax and does not discourage labour supply, as Prescott explains:

Any system that taxes people when they are young and gives it back when they are old will have a negative impact on labour supply. People will simply work less.

Put another way: If people are in control of their own savings, and if their retirement is funded by savings rather than transfers, they will work more.

Prescott’s Nobel Prize jointly with Finn Kydland was for showing that policies are often plagued by problems of time inconsistency. They demonstrated that society could gain from prior commitment to economic policies.

Of course, as Tyler Cowen observed, forced savings schemes are easily offset by people rearranging their affairs, and they have their entire adult life to do so:

How much can our government force people to save in the first place?

You can make them lock up funds in an account, but they can respond by borrowing more on their credit cards, taking out a bigger mortgage, and in general investing less in their future.

People do not save for their retirements not because they are short-sighted, but because they are far-sighted. They know that governments will not carry out their threats and other big talk about not providing an adequate old-age pension.

The only way that governments can commit to not bailing people out who retire with no savings is to make them save for their own retirements over their working lives.

Some will be against this compulsion. Their opposition to compulsion cannot be based on opposition to the nanny state because that is faulty reasoning.

These opponents of compulsion and everyone else in the retirement income policy debate are playing in a far more complicated, decades long dynamic political game where ordinary people time and again out-smart conceited governments who pretend they know better:

The government has strategies.

The people have counter-strategies.

Ancient Chinese proverb

Tom Sargent’s 12 lessons from economics for public policy

17 Apr 2014 Leave a comment

in applied welfare economics, entrepreneurship, industrial organisation, macroeconomics, market efficiency, politics, Public Choice Tags: Thomas Sargent, time inconsistency, trade-offs

Tom Sargent is a life-long Democrat who is old enough to remember when Democrats were fiscal conservatives.

At a graduation speech at Berkeley, Sargent listed these lessons:

-

Many things that are desirable are not feasible.

-

Individuals and communities face trade-offs.

-

Other people have more information about their abilities, their efforts, and their preferences than you do.

-

Everyone responds to incentives, including people you want to help. That is why social safety nets don’t always end up working as intended.

-

There are trade-offs between equality and efficiency.

-

In an equilibrium of a game or an economy, people are satisfied with their choices. That is why it is difficult for well-meaning outsiders to change things for better or worse.

-

In the future, you too will respond to incentives. That is why there are some promises that you’d like to make but can’t. No one will believe those promises because they know that later it will not be in your interest to deliver. The lesson here is this: before you make a promise, think about whether you will want to keep it if and when your circumstances change. This is how you earn a reputation.

-

Governments and voters respond to incentives too. That is why governments sometimes default on loans and other promises that they have made.

-

It is feasible for one generation to shift costs to subsequent ones. That is what national government debts and the U.S. social security system do (but not the social security system of Singapore).

-

When a government spends, its citizens eventually pay, either today or tomorrow, either through explicit taxes or implicit ones like inflation.

-

Most people want other people to pay for public goods and government transfers (especially transfers to themselves).

- Because market prices aggregate traders’ information, it is difficult to forecast stock prices and interest rates and exchange rates

Recent Comments