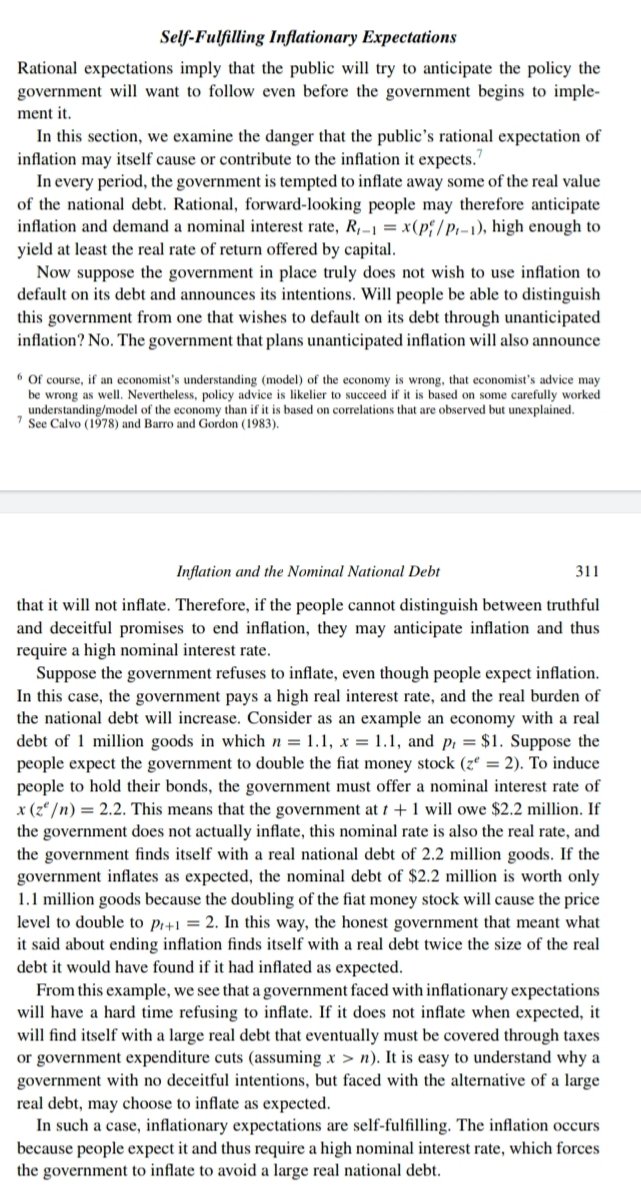

Monetary-Fiscal Interactions: Eric Leeper Interviewed by Jan Libich

09 Nov 2021 Leave a comment

in budget deficits, business cycles, economic growth, economic history, financial economics, fiscal policy, history of economic thought, macroeconomics, monetarism, monetary economics Tags: inflation, monetary policy, rational expectations

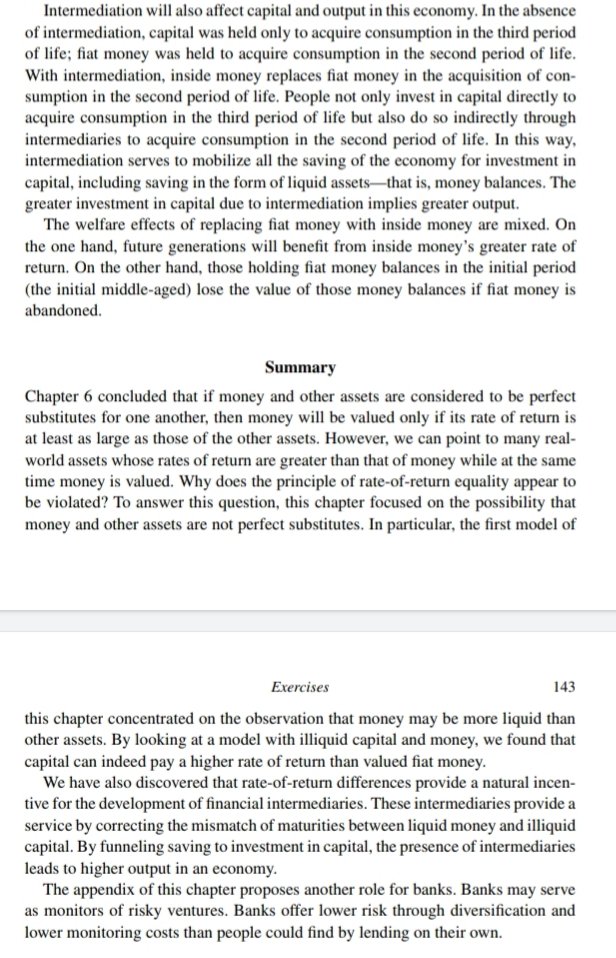

Champ and Freeman on financial intermediation

19 Feb 2020 Leave a comment

in applied price theory, economics of information, industrial organisation, macroeconomics, monetary economics Tags: adverse selection, asymmetric information, monetary policy, moral hazard, rational expectations

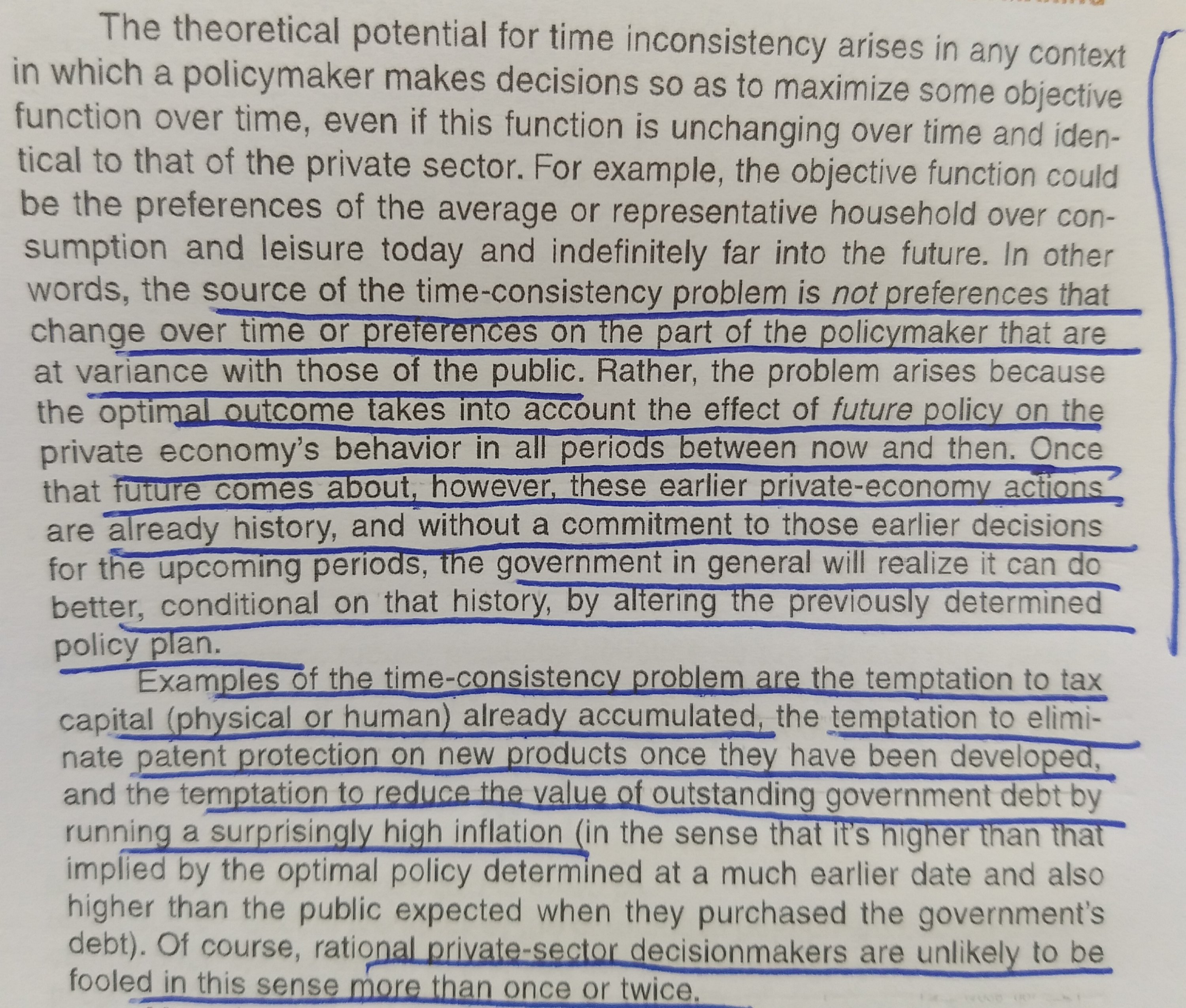

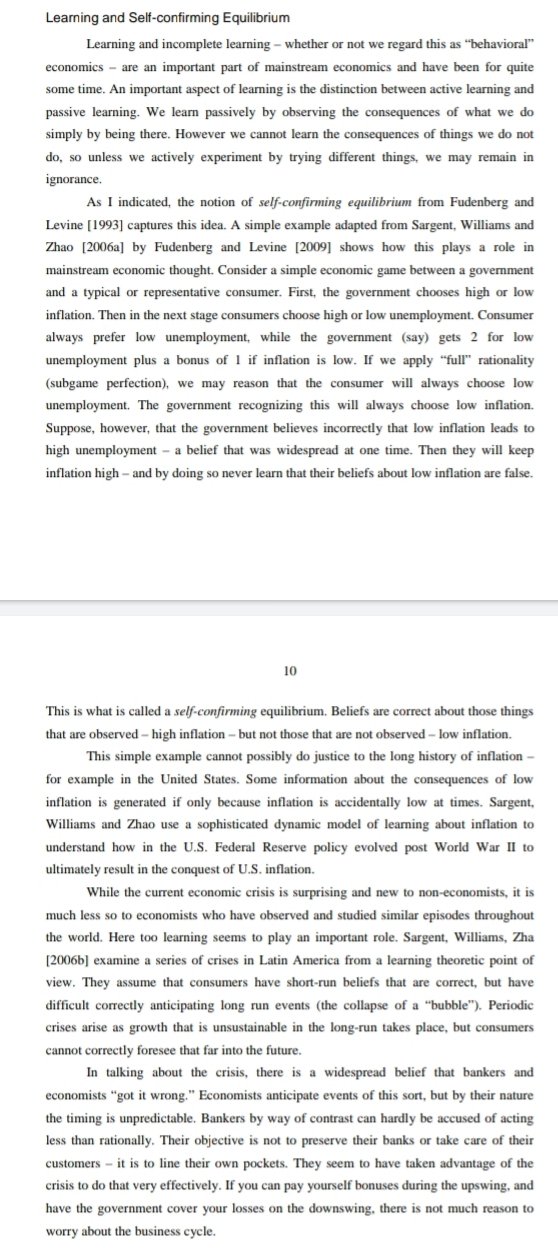

David Levine on self-confirming equilibriums

12 Jan 2020 Leave a comment

in applied price theory, business cycles, economics of information, global financial crisis (GFC), great recession, labour economics, labour supply, macroeconomics, monetary economics, unemployment Tags: rational expectations

Eugene Fama on share market bubbles

02 Jan 2020 Leave a comment

in business cycles, economic history, economics of information, entrepreneurship, financial economics, global financial crisis (GFC), great depression, great recession, industrial organisation, macroeconomics, monetary economics, survivor principle Tags: efficient markets hypothesis, pessimism bias, rational expectations

Kydland on the Great Recession and fiscal sentiment

01 Jan 2020 3 Comments

in budget deficits, business cycles, econometerics, economic growth, economic history, fiscal policy, great recession, income redistribution, macroeconomics, politics - USA, Public Choice, public economics Tags: rational expectations, real business cycles

Recent Comments