Does tax reform lead to lower taxes?

14 May 2015 Leave a comment

in politics - Australia, politics - New Zealand, politics - USA, public economics, taxation Tags: efficient taxes, tax reform

In another neo-liberal victory, health and welfare spending shares have doubled in the last 50 years

24 Apr 2015 Leave a comment

in income redistribution, politics - USA, Public Choice, public economics Tags: Director's Law, Leftover Left, median voter theorem, neoliberalism, tax reform, welfare state

The social cost of high company tax rates is just too high

22 Apr 2015 Leave a comment

in economic growth, fiscal policy, human capital, income redistribution, labour economics, macroeconomics, Public Choice Tags: company tax rate, entrepreneurial alertness, tax reform

Average tax rates on consumption, investment, labour and capital in USA, UK and Canada, 1950-2013

17 Apr 2015 5 Comments

in business cycles, economic growth, economic history, fiscal policy, global financial crisis (GFC), great recession, macroeconomics, politics - USA, public economics Tags: British economy, Canada, sick man of Europe, tax incidence, tax reform

Income taxes in the USA and UK didn’t change all that much after the mid-70s. Prior to that, income tax rose quite steadily in the UK in the 1950s and 1960s and not surprisingly, Britain was the sick man of Europe in the 1970s. Income taxes rose quite steadily in Canada for most of the post-war period up until 1990 and then levelled out for most of that decade before a small tapered downwards.

Source: Cara McDaniel.

Taxes on consumption expenditure were very different stories across the Atlantic. There has been a tapering down in the average tax rate on American consumption expenditure since 1970 after modest increases before that. Canadian taxes on consumption expenditure rose steadily until the 1970s, then drop steadily in the 1970s and than rose in the 1980s and dropped again after 1992. British taxes on consumption expenditure rose sharply in the late 1960s, dropped sharply and then rose again in the 1970s and was pretty steady after that.

The sleeper tax in all three countries was payroll taxes to fund social security and the welfare state. These rose steadily in the USA, UK and Canada up until the 1990s.

Source: Cara McDaniel.

Despite all that nonsense about neoliberalism from the Left over Left, the average rate of tax on capital income did not appear to change much at all over the last 50 years. There was a modest taper in US capital income taxation from the mid-30s to the mid-20s over the entire post-war period. The average Canadian tax rate on income from capital rose steadily in the 60s, fell steadily in the 70s before rising again in the mid-1980s and fell again after 2000. The average British tax rate on capital income rose steadily in the 60s and 70s, coinciding with the emergence of Britain as a sick man of Europe, and then stabilised in the the 1980s onwards but with a dip in the late 80s before a rise in the early 1990s.. Despite the large cuts in the statutory corporate tax rate in the UK, there was only a mild taper in the average tax rate on capital income in the UK.

Source: Cara McDaniel.

The average tax rate on investment expenditures is pretty stable in the USA for the entire post-war period. The only significant increase in the average tax rate on investment expenditures in the UK coincided with the emergence of the sick man in Europe after a drop in the early 70s. The average tax rate on investment expenditures do not change at all in the UK after the 1970s. The Canadian average tax rate on investment expenditures is higher than elsewhere. It rose steadily in the 50s and 60s, dropped in the 70s and rose again in the 80s before tapering from 1992 onwards.

Source: Cara McDaniel.

These higher on rising taxes and the UK and Canada did nothing for either country in catching up with the USA. The figure 1 below shows real GDP per working age per American, Canadian and British.

Figure 1: Real GDP per Canadian, British and American aged 15-64, converted to 2013 price level, updated 2005 EKS purchasing power parities, 1950-2013

Source: Computed from OECD StatExtract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

The USA is pulling away from Canada and the UK in GDP per working age person. The exception is British economy from about 1990 onwards which caught up with Canada.

Figure 2, which is detrended GDP data, illustrates the British economic boom in the 1990s. Each country’s annual economic growth rate is detrended by 1.9%, the detrending value currently used by Ed Prescott. A flat line is growth at 1.9%, a rising line is above trend growth, a falling line is below trend growth.

Figure 2: Real GDP per Canadian, British and American aged 15-64, converted to 2013 price level, updated 2005 EKS purchasing power parities, detrended 1.9%, 1950-2013

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

Figure 2 shows that Canada has been in a long-term decline since the mid-1980s with much of this decline coinciding with periods of rising taxes on income from labour.

The British economy boomed in the 1990s, after the tax hikes of the 1970s and early 80s were reversed. This growth dividend was squandered by the Blair government in the 2000.

Figure 2 also shows that US growth was rather stable with some ups and downs up until 2007, expect during the productivity slowdown in the 1970s. The first major departure from trend growth of 1.9% was with the onset of the great recession.

Desperately seeking a neoliberal conspiracy to slash taxes to the bone in Australia and New Zealand

31 Mar 2015 Leave a comment

in politics - New Zealand, politics - USA, public economics Tags: neoliberalism, Rogernomics, tax reform

If our friends on the Left are to be believed, governments fell under the spell of a flying visit by Milton Friedman and his local neoliberal cronies and slashed taxes to the bone from about the mid-1980s in Australia and New Zealand.

Source: Revenue Statistics – Comparative tables.

In Australia’s case, the only time tax revenue as a percentage of GDP fell prior to the election of a Labour government in 2007 was during a deep recession in 1991. This was a recession bought on by irresponsible monetary policy by Paul Keating– the Keating recession.

As for New Zealand, the tax take increase quite considerably under tax reforms of the Labour Government of the 1980s. Roger Douglas, far from being a neoliberal plant, seemed to be a double secret agent of a tax maximising Leviathan. Little wonder the New Zealand economy was sluggish in the late 1980s because of this large increases in the tax take.

Osborne won't rule out tax cut for top earners ind.pn/1JaeId4 http://t.co/LvO7vgmmX0 http://t.co/YU3600Sk5s—

Marcus Chown (@marcuschown) April 05, 2015

Tax reform leads to higher taxes – the evidence on the GST

31 Mar 2015 Leave a comment

in constitutional political economy, politics - Australia, politics - New Zealand, Public Choice, public economics, taxation Tags: Geoffrey Brennan, James Buchanan, tax reform

The GST increased from 10 to 15% in New Zealand; more than doubled in the UK; but GST rates were stable or went up and down in the remaining Anglo-Saxon countries.

As for a selection of other non-Anglo-Saxon countries , Brennan and Buchanan were right. Tax reforms such as a broad-based consumption tax leads to higher taxes through time.

ICYMI: How does Australia's GST compare with other nations? ab.co/1eBsdrS #factcheck http://t.co/QFP05xonEB—

ABC Fact Check (@ABCFactCheck) July 31, 2015

The GST (goods and services tax) in Europe is known as the value added tax (VAT).

Source: OECD Tax Database – OECD.

Trends in average marginal tax rates in the USA

05 Jan 2015 Leave a comment

in economic history, political change, politics - USA, public economics Tags: Marginal tax rates, tax reform, taxation and the labour supply

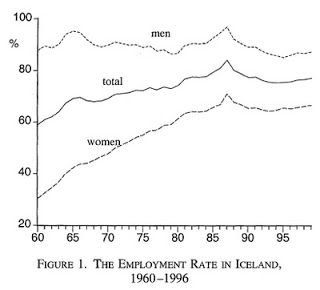

Supply-Side Economics in Iceland

15 May 2014 Leave a comment

in economic growth, labour economics Tags: Iceland, tax reform

The move to a pay-as-you-earn income tax system in Iceland in 1988 made income earned in 1987 tax-free.

- Icelandic GDP increased by 4.16% in 1987.

- Total labour supply rose by 6.7% in 1987 over the average of 1986 and 1988.

- This included an 8.6% increase in weeks of work supplied by those already in the labour market in 1986.

Notice in the graph the big kink in employment in 1987. A spike just for the year of no taxes. Labour supply then fell away.

Iceland in 1987 was a unique opportunity to study the labour supply response of individuals who were temporarily faced with a zero marginal-and average-income tax rate.

The path to higher U.S. prosperity

12 May 2014 Leave a comment

in applied welfare economics, economic growth, Edward Prescott, great recession, labour economics, macroeconomics Tags: capital taxation, Edward Prescott, retirement savings, tax reform

Suppose the USA:

- Had mandatory savings for retirement

- Eliminated capital income taxes

- Broadened tax base and lowered the marginal tax rate

- Phased in reforms so all birth-year cohorts are made better off

- Left welfare programs and local public good shares the same

- Savings not part of taxable income, saving withdrawals part of taxable income – with these changes U.S. income tax would be a consumption tax

US Detrended GDP per Capita

Source: Edward Prescott and Ellen McGrattan 2013.

Tax reforms lead to higher taxes

22 Mar 2014 3 Comments

in constitutional political economy, James Buchanan, Public Choice, public economics, taxation Tags: Casey Mulligan, efficient taxes, Gary Becker, growth of government, James M. Buchanan, tax reform, taxation in Nordic countries

After the 1970s tax revolts and California’s Proposition 13, Buchanan and Brennan wrote The Power to Tax. Their message was that if you don’t always trust governments, beware of efficient taxes.

More efficient taxes make it easier for government to extract more tax revenue from the population with less resistance. Taxes can be made more efficient by broadening tax bases and removing loopholes while lowering marginal rates. A GST that replaces a web of sales taxes is a common example. The GST always goes up over time, never down over time. Most tax reforms are revenue neutral.

When Brennan said at a tax reform conference in Australia 20 years or so ago that efficient taxes and tax reforms are both bad because they lead to higher taxes and a larger government, no one understood him.

Idealists all, the audience including me assumed they were advising a benevolent government, not a revenue-maximising leviathan government – a beast that needed to be staved with constitutional constraints on the number and size of tax bases and tax instruments.

Fiscal arrangements were analysed by Buchanan and Brennan in The Power to Tax in terms of the preferences of citizen-taxpayers who are permitted at some constitutional level of choice to select the fiscal institutions they are to be subject to over an uncertain future.

Those in elected office are assumed to exploit the power assigned to them to the maximum possible extent: government is a revenue-maximising leviathan.

Buchanan and Brennan were all for inefficient tax systems because they do not raise as much revenue. A government that cannot raise much revenue cannot grow very large.

Gary Becker and Casey Mulligan attributed the growth in the size of governments in the 20th century to demographic shifts, more efficient taxes, more efficient spending, a shift in the political power from the taxed to the subsidised, shifts in political power among taxed groups, and shifts in political power among the subsidised groups:

An improvement in the efficiency of either taxes or spending would reduce political pressure for suppressing the growth of government and thereby increase total tax revenue and spending.

Tax reform saved the late 20th century welfare state by raising the same or more revenue with less taxpayer resistance. Taxes are very efficient in the Nordic countries – high tax rates on labour income and consumption but lower on capital income. And light regulation too.

{kind=link}

Recent Comments