Intangible Capital and Measured Productivity

23 Sep 2025 Leave a comment

in business cycles, economic growth, economic history, global financial crisis (GFC), great recession, macroeconomics Tags: real business cycle theory

This kind of macro theory is underrated

01 Mar 2024 Leave a comment

in applied price theory, business cycles, fiscal policy, history of economic thought, job search and matching, macroeconomics, monetary economics Tags: real business cycle theory

Demand shocks as technology shocks: We provide a macroeconomic theory where demand for goods has a productive role. A search friction prevents perfect matching between producers and potential customers. Larger demand induces more search, which in turn increases GDP and measured TFP. We embed the product-market friction in a standard neoclassical model and estimate it […]

This kind of macro theory is underrated

Edward Prescott on the Great Recession

31 May 2020 Leave a comment

in business cycles, Edward Prescott, financial economics, global financial crisis (GFC), great recession, macroeconomics, monetary economics Tags: real business cycle theory

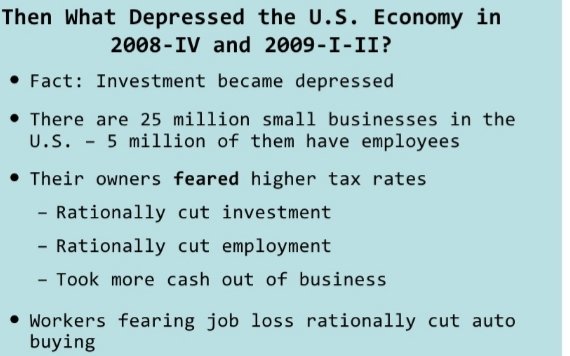

Will taxes stall the #COVID19 recovery?

18 May 2020 Leave a comment

in applied price theory, budget deficits, business cycles, econometerics, economic growth, economic history, fiscal policy, global financial crisis (GFC), great recession, labour economics, labour supply, macroeconomics, Public Choice, public economics Tags: real business cycle theory, taxation and investment

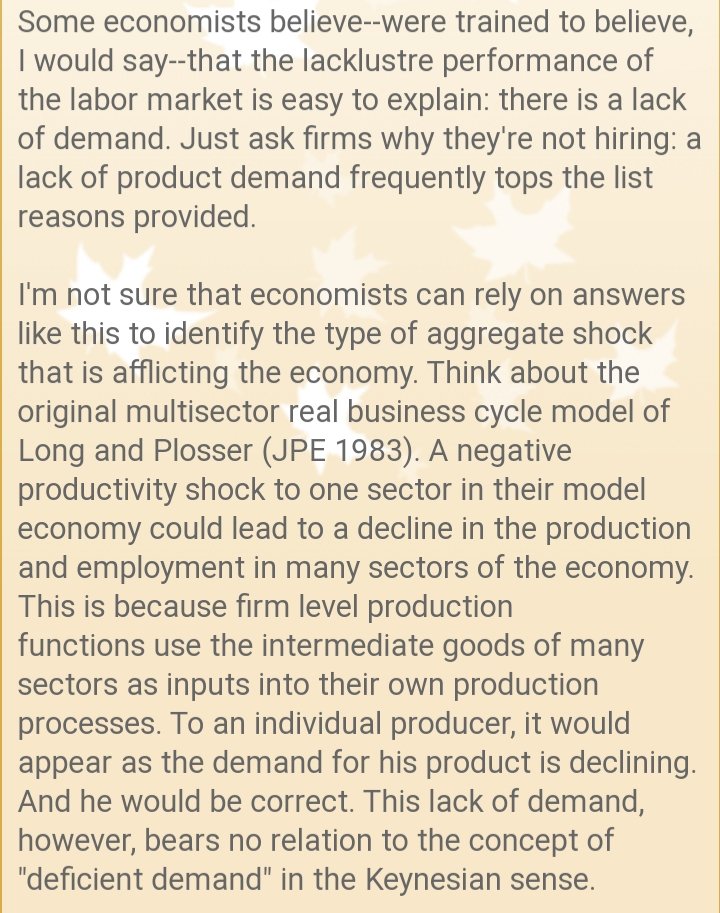

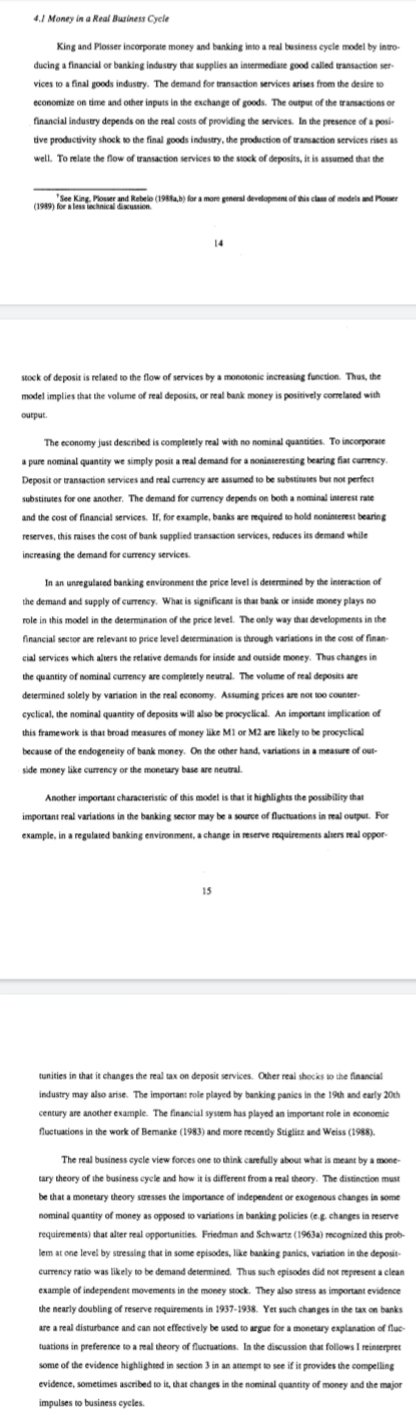

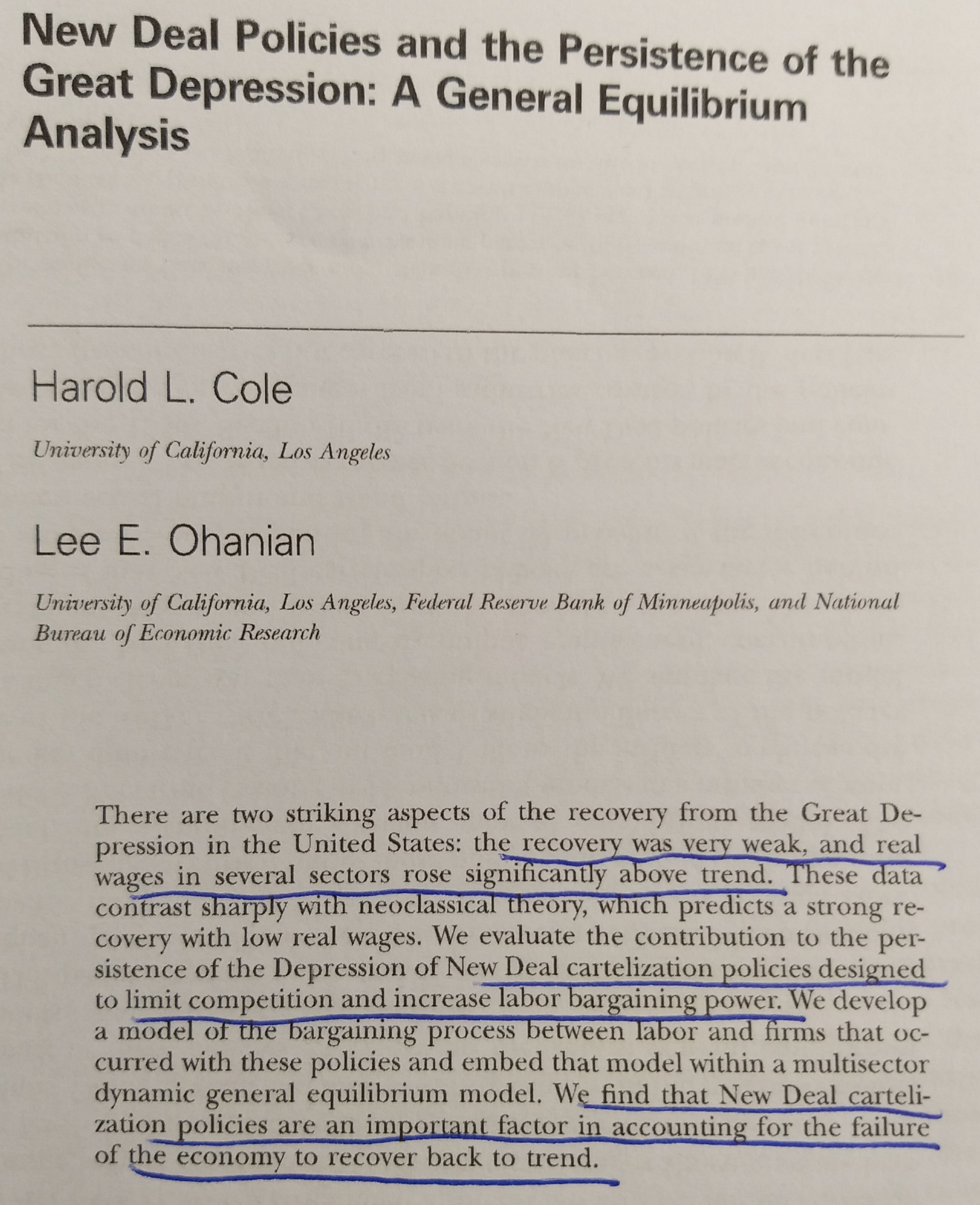

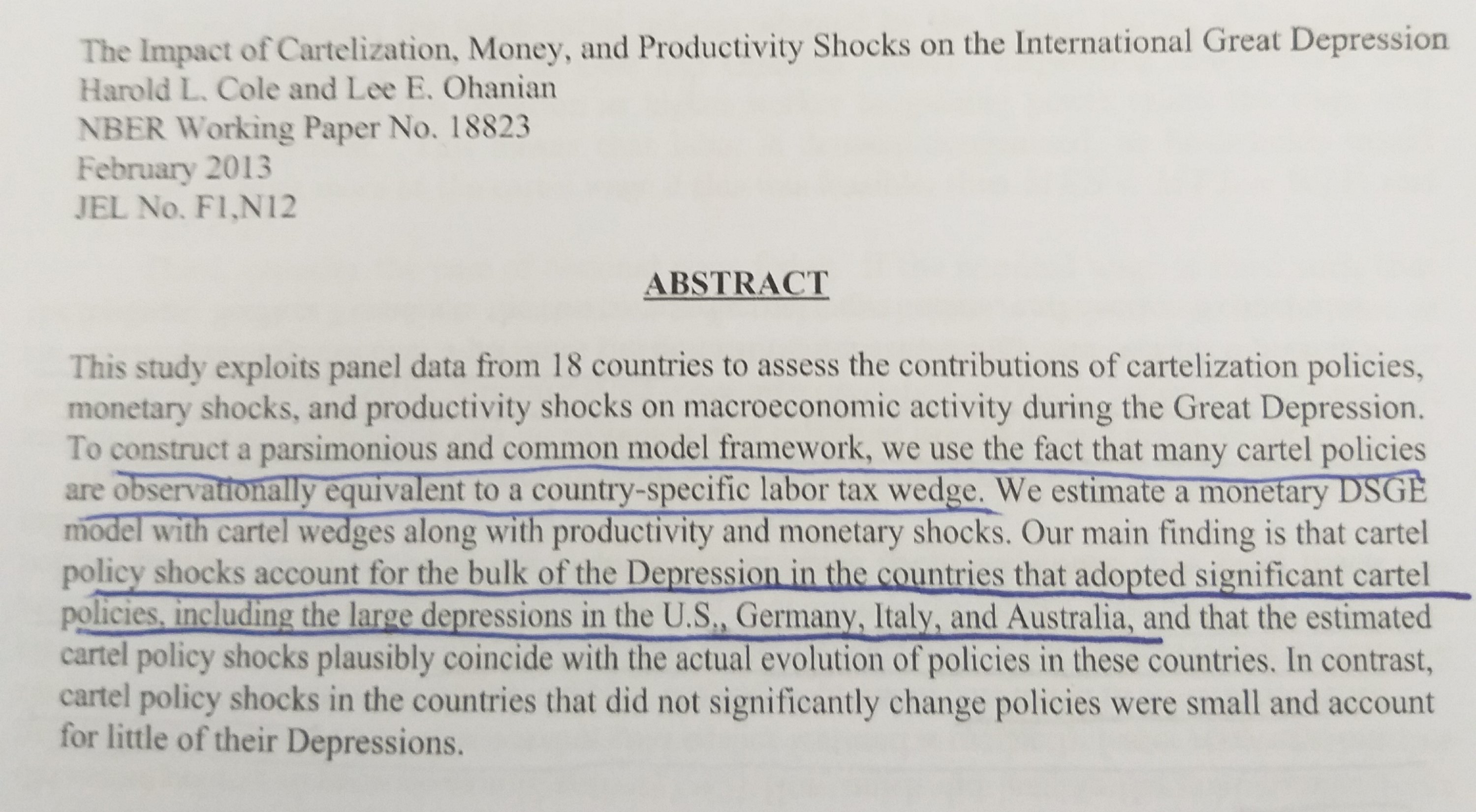

What is deficient aggregate demand?

20 Apr 2020 Leave a comment

in business cycles, economic growth, Edward Prescott, fiscal policy, macroeconomics, monetary economics Tags: real business cycle theory

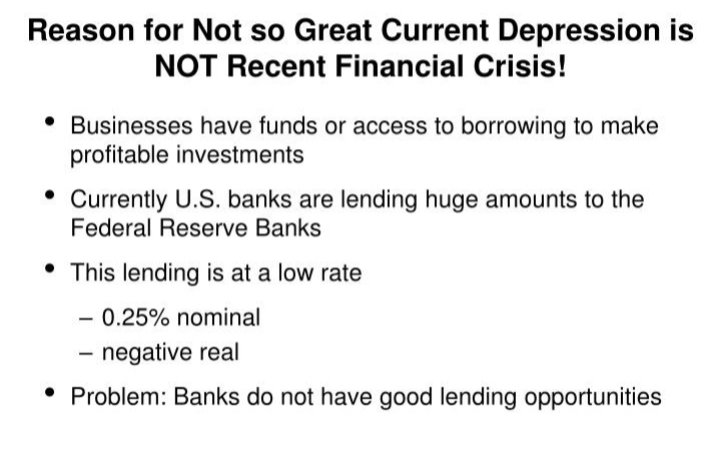

Edward Prescott on the #GFC

24 Mar 2020 Leave a comment

in budget deficits, business cycles, economic growth, Edward Prescott, fiscal policy, global financial crisis (GFC), great recession, labour economics, labour supply, macroeconomics, public economics Tags: real business cycle theory, taxation and entrepreneurship, taxation and investment, taxation and labour supply

Recent Comments