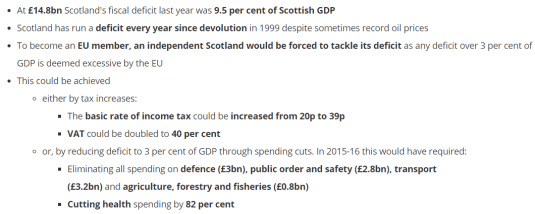

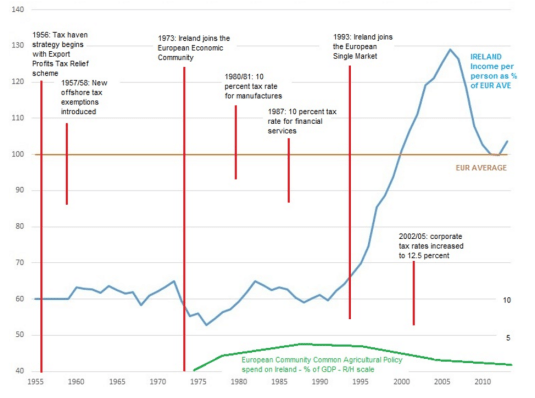

Source: Scottish deficit is twice that of the UK and higher than Greece – The TaxPayers’ Alliance.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

13 Oct 2016 Leave a comment

in constitutional political economy, fiscal policy

12 Oct 2016 Leave a comment

in business cycles, job search and matching, labour economics, macroeconomics, unemployment Tags: Australia, Canada, long-term unemployment, social insurance, unemployment duration

05 Oct 2016 Leave a comment

in job search and matching, labour economics, labour supply, macroeconomics, Robert E. Lucas, unemployment Tags: involuntary unemployment, job search, search and matching

Robert Lucas in a famous 1978 paper argued that all unemployment was voluntary because involuntary unemployment was a meaningless concept:

“The worker who loses a good job in prosperous time does not volunteer to be in this situation: he has suffered a capital loss. Similarly, the firm which loses an experienced employee in depressed times suffers an undesirable capital loss.

Nevertheless the unemployed worker at any time can always find some job at once, and a firm can always fill a vacancy instantaneously. That neither typically does so by choice is not difficult to understand given the quality of the jobs and the employees which are easiest to find.

Thus there is an involuntary element in all unemployment, in the sense that no one chooses bad luck over good; there is also a voluntary element in all unemployment, in the sense that however miserable one’s current work options, one can always choose to accept them.”

I agree that we all make choices subject to constraints. To say that a choice is involuntary because it is constrained by a scarcity of job-opportunities information is to say that choices are involuntary because there is scarcity. Alchian said there are always plenty of jobs because to suppose the contrary suggests that scarcity has been abolished.

Lucas elaborated further in 1987 in Models of Business Cycles:

A theory that does deal successfully with unemployment needs to address two quite distinct problems. One is the fact that job separations tend to take the form of unilateral decisions – a worker quits, or is laid off or fired – in which negotiations over wage rates play no explicit role.

The second is that workers who lose jobs, for whatever reason, typically pass through a period of unemployment instead of taking temporary work on the ‘spot’ labour market jobs that are readily available in any economy.

Of these, the second seems to me much the more important: it does not ‘explain’ why someone is unemployed to explain why he does not have a job with company X. After all, most employed people do not have jobs with company X either. To explain why people allocate time to a particular activity – like unemployment – we need to know why they prefer it to all other available activities: to say that I am allergic to strawberries does not ‘explain’ why I drink coffee.

Neither of these puzzles is easy to understand within a Walrasian framework, and it would be good to understand both of them better, but I suggest we begin by focusing on the second of the two.

03 Oct 2016 Leave a comment

in economic history, global financial crisis (GFC)

30 Sep 2016 Leave a comment

in business cycles, economic growth, macroeconomics, Milton Friedman, monetarism, monetary economics, politics - Australia Tags: central banks, conspiracy theories, lags on monetary policy, monetary policy, rules versus discretion, The fatal conceit, The pretense to knowledge

Milton Friedman visited Australia in 1975. He spoke with government officials and appeared on the TV show Monday Conference. Apparently, that was enough for him to take over Australian monetary policy setting for the foreseeable future.

When working at the next desk to the monetary policy section in the late 1980s, I heard not a word of Friedman’s Svengali influence:

See Ed Nelson’s (2005) Monetary Policy Neglect and the Great Inflation in Canada, Australia, and New Zealand who used contemporary news reports from 1970 to the early 1990s to uncover what was and was not ruling monetary policy. For example:

“As late as 1990, the governor of the Reserve Bank rejected central-bank inflation targeting as infeasible in Australia, and cited the need for other tools such as wages policy (AFR, October 18, 1990).”

Bernie Fraser was still sufficiently deprogrammed in 1993 to say that “…I am rather wary of inflation targets.” Easy to then announce one in the same speech when inflation was already 2-3%.

When as a commentator on a Treasury seminar paper in 1986, Peter Boxhall – fresh from the US and 1970s Chicago educated – suggested using monetary policy to reduce the inflation rate quickly to zero, David Morgan and Chris Higgins almost fell off their chairs. They had never heard of such radical ideas.

In their breathless protestations, neither were sufficiently in-tune with their Keynesian educations to remember the role of sticky wages or even the need for the monetary growth reductions to be gradual and, more importantly, credible as per Milton Freidman and as per Tom Sargent’s End of 4 big and two moderate inflations papers.

I was far too junior to point to this gap in their analytical memories about the role of sticky wages, and I was having far too much fun watching the intellectual cream of the Treasury senior management in full flight. At a much later meeting, another high flying deputy secretary was mystified as to why 18% mortgage rates were not reining in the current account in 1989.

Friedman’s Svengali influence did not extend to brainwashing in the monetarist creed that the lags on monetary policy were long and variable. The 1988 or 1989 budget papers put the lag on monetary policy at 1 year, which is short and rapier, if you ask me.

29 Sep 2016 Leave a comment

in economic growth, economic history, economics of education, human capital, labour economics, macroeconomics Tags: education premium, endogenous growth theory, graduate premium

Some people get quite excited about the growth benefits and externalities from investing in more human capital such as more young people going to university. In New Zealand, the number of graduates quadrupled over the last 30 years but the trend GDP growth rate is unchanged. Please explain?

Source: Educational attainment of the adult population: The Social Report 2016 – Te pūrongo oranga tangata.

28 Sep 2016 Leave a comment

in applied price theory, development economics, economic growth, economic history, economics of education, human capital, labour economics, macroeconomics Tags: Thomas Sowell

27 Sep 2016 3 Comments

in business cycles, economic history, macroeconomics, monetarism, monetary economics, politics - Australia Tags: central banks, monetary policy, The Great Inflation

Australian policymakers from at least 1971 viewed inflation as not a consequence of their monetary policy decisions. There were repeated references by them to wage-price spirals and both unsuccessful (1977) and successful attempts (1981) at wage freezes.

The prices and incomes accord from 1983 onwards was just another 1970s wage tax trade-off. An Incomes policy attributes inflation to non-monetary factors, as did Fraser and Lynch regularly.

• It was not until 1980 that the Fraser government’s monetary policy became genuinely anti-inflationary. With a lag, these changes halved inflation to the mid-single digits by 1983. The implementation lag on the 1975 Monday conference programme must have been long and variable and lasted for a three year window!? Three years out of 20 is hardly a monetarist hegemony!

• Australia had lower CPI inflation in the 1980s than the 1970s, but this was marred by rebounds in 1985–86 and 1988–90 to near 9%.

The monetary policy regime change in the late 1980s was triggered by factors besides rising inflation: a demonic view of currant account.

After several years of high interest rates, the budget papers forecasted a moderate slowing:

• The budget GDP forecast for 1990-91 was 2% with an actual of minus 0.4%; for inflation the actual and forecast were 5.3% versus 6.5%; 1989-90 inflation rate was 8% with GDP growth of 3.3%.

• In 1991-92, the budget GDP forecast was 1.5% with an actual of 2.1%; for inflation the actual and forecast were 1.9% versus 3.8%.

• In 1992-93, the budget papers forecast for inflation 3% for an actual of 1%.

• In 1993-94, the budget forecast for inflation 3.5% for an actual of 1.8%.

The monetarists in the Treasury, entranced as they were by Friedman’s 1975 visit, still had not clicked to the link between a tight monetary policy and low inflation as late as 1993. Australia pursued a stop-go monetary policy from 1971 to the early 1990s.

I worked in the next desk to the monetary policy section in the Prime Minister’s Department in the 1980s. They were determined that market set interest rates, not monetary policy.

I suggest you read the biography of keating by john edwards(?) – his economic advisor in the late 1980s.

Edwards quotes from numerous Treasury briefings to Keating. the Treasury remembered their Keynesian educations well, as did those at DPMC. the prices and incomes accord was very Keynesian: inflation as a non-monetary phenomenon

Mentioning Friedman’s name in the 1980s at job interviews would have been extremely career limiting. Not much better in the early 1990s. Back in the late 1980s, Friedman was graduating from ‘a wild man in the wings’ to just a suspicious character in policy circles.

If you name dropped Hayek in the 1980s and 1990s, any sign of name recognition would have indicated that you were been interviewed by people who were very widely read.

21 Sep 2016 1 Comment

in economic history, global financial crisis (GFC), macroeconomics, monetary economics

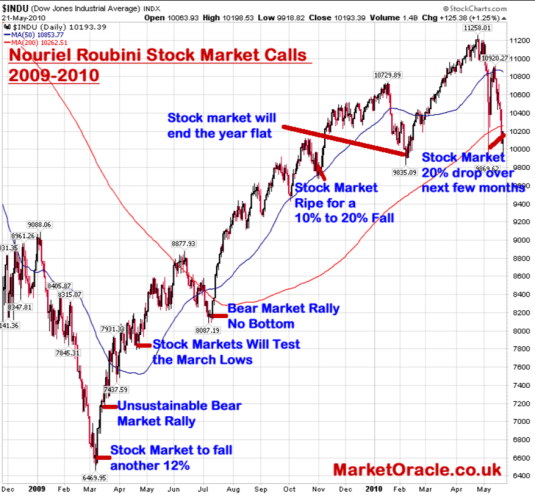

You are not much of a leftover Marxist if you are not predicting a crisis in capitalism is on the horizon.

https://twitter.com/PolicyObsAUT/status/778456702655995904

Capitalism is supposed to collapse under its own inner contradictions.

Professional stock market tipsters are notorious from specialising in predicting doom as well and they still get listened too despite terrible forecasting records.

Plenty of people warned of dark days ahead in the lead up to the global financial crisis. An essay anyone can read with profit is Ross Levine’s An Autopsy of the U.S. Financial System: Accident, Suicide, or Negligent Homicide? His abstract says

The evidence is inconsistent with the view that the collapse of the financial system was caused only by the popping of the housing bubble (“accident”) and the herding behavior of financiers rushing to create and market increasingly complex and questionable financial products (“suicide”).

Rather, the evidence indicates that senior policymakers repeatedly designed, implemented, and maintained policies that destabilized the global financial system in the decade before the crisis. Moreover, although the major regulatory agencies were aware of the growing fragility of the financial system due to their policies, they chose not to modify those policies, suggesting that “negligent homicide” contributed to the financial system’s collapse.

The New York Times warned in 1999 that Fannie Mae was taking on so much risk that an economic downturn could trigger a “rescue similar to that of the savings and loan industry in the 1980s,” and emphasised this point again in 2003. Greenspan testified before a Senate committee in 2004 that the increasingly large and risky Fannie Mae and Freddie Mac portfolios could have enormously adverse ramifications.

You predict a financial crisis by pointing to adjustments in your share portfolio to take advantage of shorting the market and then showing how big a profit you made afterwards.

The movie The Big Short highlights that its protagonists had skin in the game. They were investing in mortgages or shorting the same in the expectation of the crash they were predicting. Much of the drama in the film is about how long their foretelling of a crash took to come true.

There were no windbags and armchair critics in The Big Short talking gloom and doom on the horizon without investing their own money to profit from their forecasts.

15 Sep 2016 Leave a comment

in applied price theory, monetary economics Tags: Shawshank Redemption

13 Sep 2016 Leave a comment

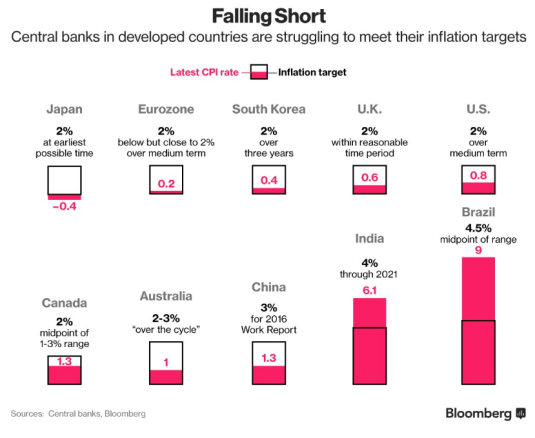

in economic history, inflation targeting, macroeconomics, monetary economics, politics - New Zealand Tags: CPI bias, inflation rate

The inflation rate is overstated by about 1% each year because of difficulties in measuring new goods entering the consumer price index and improvements in the quality of existing goods in the consumer price index. With that adjustment of 1% in the chart below, a common measure of that bias, New Zealand has had zero to negative inflation for four years

Source: Reserve Bank of New Zealand Key Statistics.

One of the reasons for an inflation target band of 1 to 3% is an inflation rate of 1% is actually an inflation rate of 0%.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A History of the Alt-Right

Econ Prof at George Mason University, Economic Historian, Québécois

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Recent Comments