Tom Sargent’s Keynote Address BYU CPEC 2012 on taxation and redistribution

11 Dec 2014 Leave a comment

in fiscal policy, labour economics, labour supply, macroeconomics, public economics Tags: taxation and the labour supply, Tom Sargent

Is welfare dependence optimal for whom – part 4: In-work tax credits and labour supply

10 Dec 2014 3 Comments

in labour economics, labour supply, public economics, welfare reform Tags: Labour leisure trade-off, welfare dependency, welfare reform

In-work tax credits were introduced in many countries including New Zealand to encourage movement into employment by breadwinners. By linking a large payment with full-time and semi-full-time work, the rewards for working are increased for single parents and families. These in work tax credits combined child tax credit with an in work tax credit for the sole mother or couple.

These in-work benefits can phase-in when a minimum income level is reach such as with the Earned Income Tax Credit (EITC) in the USA, or a paid in full when a minimum number of hours are worked. The Working for Families in-work tax credit in New Zealand and the UK family tax credit are two examples where there is a large cash payment with no phasing-in:

- Working for Families in New Zealand is paid if 30 hours are worked by New Zealand families or 20 hours are worked by sole parents; and

- The British family tax credit was paid if 16 hours are worked, initially 24 hours per week.

Figure 1 shows the impact of the introduction of an in-work tax credit paid in full to families and sole parents if a minimum number of hours per week are worked by a family or sole parent. There is no phase-in region such as with the earned income tax credit (EITC) in the USA.

Figure 1: In work tax credits and labour supply

The in-work tax credit phases-out after once the family’s income increases past an income threshold. This income threshold is usually linked to the number of children as well.

An in-work family tax credit linked to a high number of minimum number of hours worked provides an incentive for those not in work to increase their hours worked by a large amount and leave welfare, as is shown by arrow 1 in Figure 1.

For those already work, the income and substitution effect cut against each other and their net effect depend on the number of hours currently worked.

- Those working a low number of hours, hours less per week than the minimum to qualify for the in-work tax-credit have an incentive to increase their hours to the minimum to qualify and leave welfare is shown by arrow 2 in Figure 1.

- Arrows 3 and 4 in Figure 1 both represent reduction in hours worked.

- Some workers can take-home more pay and work fewer hours per week or per year as shown by arrow 3.

- Other high working hours worker can enjoy more leisure time at the expense of a slightly reduced take-home pay as shown by arrow 4.

The net labour supply effects of an in-work tax credit are therefore ambiguous because of these multiplicity of labour supply effects with some people working more another’s work in letters.

There will also be a bunching of hours worked at around the eligibility point for paying the in-work tax credit. The eligibility point is usually grouped around working a minimum of three or four days per week part or full-time that sum to 30 hours for families and 20 hours for sole parents.

Workers working less that the weekly working hour minimums will increase to the minimum to qualify for the family tax credit. Workers working more than the minimum required to qualify for the family tax credit might cut back to the working hours minimum because of the superior labour leisure trade-off. The number of people on welfare will fall because workers leave part and full benefit dependence to qualify for the in-work tax credit.

Whether labour supply on net actually increases or decreases depends on the relative numbers of individuals at different points on the budget constraint working full-time, not working and working part-time and on the magnitudes of their responses. Some will stay as they are working full-time, not working and working part-time.

To summarise, the static labour–leisure trade-off model of labour supply suggests that increases in either benefit abatement thresholds or a reduction in benefit abatement rates will increase the numbers entering the benefit and see none leave. No one will leave.

A hours worked per week based in-work tax credit will move people who are not working and working a low number of hours to work and into a higher number of work hours respectively, with bunching around the eligibility point. An in-work tax credit will also cause some to cut back their hours so the net labour supply effect is ambiguous.

The net fiscal cost of an in-work tax credit depends on the phase-in and phased out particulars of the tax credit programme and the increase in paid employment and the number of taxpaying workers as a result of the in-work tax credit. The Working for Families tax credits in New Zealand and the United Kingdom are famous for clustering of labour supply around the eligibility point for the in work tax credit.

For example, in the UK, a lot of people used to work exactly 24 hours week. When the eligibility point was reduced to 16 per week, a new word had to be invented. This new word was mini-jobs to describe the large number of part-time workers in the UK who cut-back to exactly 16 hours per week. The family tax credit for workers is twice as generous in the UK as in New Zealand.

The blogs so far

part-one-the-labour-leisure-trade-off-and-the-rewards-for-working

part-two-the-labour-supply-effects-of-welfare-benefit-abatement-rate-changes

part-3-abatement-free-income-thresholds-and-labour-supply

part-4-in-work-tax-credits-and-labour-supply

part-5-higher-abatement-rates-and-labour-supply

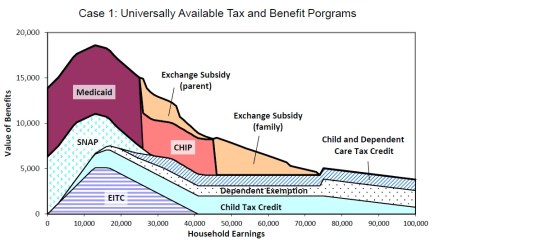

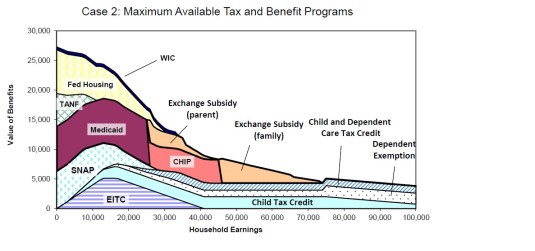

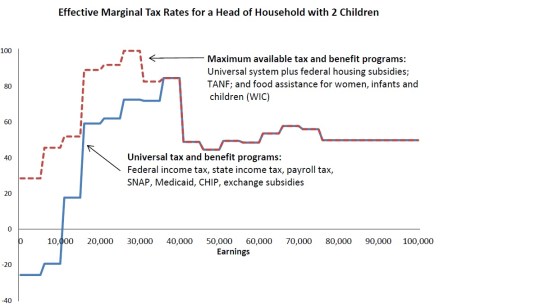

The shape of the welfare state in the USA

08 Dec 2014 Leave a comment

in fiscal policy, income redistribution, labour economics, labour supply, politics - USA, public economics, welfare reform Tags: effective marginal tax rates, Obama care, poverty traps, welfare reform

One in five Americans on Medicaid; this image does not include those on Medicare –those over 65 who get their healthcare paid by the government.

It’s not just Ed Miliband. Labour’s on the wrong side of history » The Spectator

21 Nov 2014 Leave a comment

in applied price theory, applied welfare economics, comparative institutional analysis, constitutional political economy, election campaigns, liberalism, macroeconomics, Marxist economics, political change, politics - Australia, politics - New Zealand, politics - USA, public economics, technological progress Tags: free trade, globalisation, market augmenting governments

Politicians can’t be heroes any more. Instead, they have to operate within the tightly drawn tramlines of the global economy.

This is true for those on the left and the right, but the pressure that this places on countries to adopt a low-tax, light-regulation regime is something with which the right is far more comfortable.

via It’s not just Ed Miliband. Labour’s on the wrong side of history » The Spectator.

Net and average tax in NZ | Kiwiblog

17 Nov 2014 Leave a comment

Tax Burdens: Some Facts (For a Change) | Pundit 2011

16 Nov 2014 Leave a comment

in income redistribution, liberalism, politics - New Zealand, Public Choice, public economics Tags: tax burdens, tax incidence

The 47% is bigger than you think

16 Nov 2014 2 Comments

in politics - USA, public economics, Rawls and Nozick Tags: 47%, tax incidence, who pays taxes

What if We’re Looking at Inequality the Wrong Way? – NYTimes.com

16 Nov 2014 Leave a comment

in applied welfare economics, entrepreneurship, human capital, labour economics, labour supply, liberalism, Marxist economics, occupational choice, politics - USA, poverty and inequality, public economics, Rawls and Nozick, technological progress Tags: Piketty, poverty and inequality

Is Growth of Government Inevitable? | Sam Peltzman video

12 Nov 2014 Leave a comment

in economics of regulation, income redistribution, liberalism, Public Choice, public economics, rentseeking, Sam Peltzman Tags: growth of government, Sam Peltzman

State owned enterprises continue to be a bad investment for the NZ taxpayer

12 Nov 2014 2 Comments

in industrial organisation, Marxist economics, politics - New Zealand, public economics Tags: privatisation, state owned enterprises

In a Briefing to the Incoming Minister just released, the Treasury said that in 2013, total shareholder return from state owned enterprises to the taxpayer was just 3 per cent. This is a little bit better than leaving the money in the bank.

Note: KiwiRail is excluded because of significant changes in its valuation methodologies over the past few years, including the significant write down in its asset values in 2012. . Total shareholder return for 2012 has been restated to include Solid Energy.

KiwiRail lost $248 million in 2013, after a $174.4 million loss a year earlier. Solid Energy lost $182 million last year last year. This $182m loss follows a $335.4m loss in the June 2013 year and a $40m loss the year before that.

Working for Families and work incentives

08 Nov 2014 Leave a comment

in labour economics, labour supply, politics - New Zealand, public economics, taxation, welfare reform Tags: effective marginal tax rates, tax – welfare system interactions

There are 3.38 million individual taxpayers. Of these, about 120,000 (3.4 percent) face EMTRs over 60%, 120,000 (3.4 percent) face EMTRs between 50% and 60%, and 160,000 (4.5 percent) face EMTRs between 40% and 50%. Slightly more than 88 percent of taxpayers face EMTRs below 40%.

HT: New-Zealand-tax-system-and-how-it-compares-internationally

The left-wing bias of economists alert: How textbooks are biased toward favouring tax hikes

03 Oct 2014 Leave a comment

The Economics of Europe’s Insane History of Putting Animals on Trial and Executing Them

02 Oct 2014 Leave a comment

in applied price theory, economics of religion, law and economics, Public Choice, public economics, rentseeking, taxation Tags: economics of religion, follow the money, Peter Leeson, rent seeking

The fantastically creative and insightful Peter Leeson published an article in the Journal of Law and Economics in 2013 on the practice of putting animals on trial in the Medieval ages.

Abstract

For 250 years insects and rodents accused of committing property crimes were tried as legal persons in French, Italian, and Swiss ecclesiastic courts under the same laws and according to the same procedures used to try actual persons.I argue that the Catholic Church used vermin trials to increase tithe revenues where tithe evasion threatened to erode them.

Vermin trials achieved this by bolstering citizens’ belief in the validity of Church punishments for tithe evasion: estrangement from God through sin, excommunication, and anathema.

Vermin trials permitted ecclesiastics to evidence their supernatural sanctions’ legitimacy by producing outcomes that supported those sanctions’ validity. These outcomes strengthened citizens’ belief that the Church’s imprecations were real, which allowed ecclesiastics to reclaim jeopardized tithe revenue

Leeson’s paper is also closely connected to Ekelund, Herbert, and Tollison’s (1989, 2002, 2006) and Ekelund et al.’s (1996) work. They study the medieval Catholic Church as a firm. They discuss how ecclesiastics used supernatural sanctions to protect the Church’s monopoly on spiritual services against heretical competition.

HT: Wired – fantastically-wrong-europes-insane-history-putting-animals-trial-executing/

Recent Comments