Sums up modern monetary theory too

23 Jan 2020 Leave a comment

in business cycles, economic history, economics of information, financial economics, fiscal policy, macroeconomics, monetary economics Tags: hyperinflation, monetary cranks, monetary policy

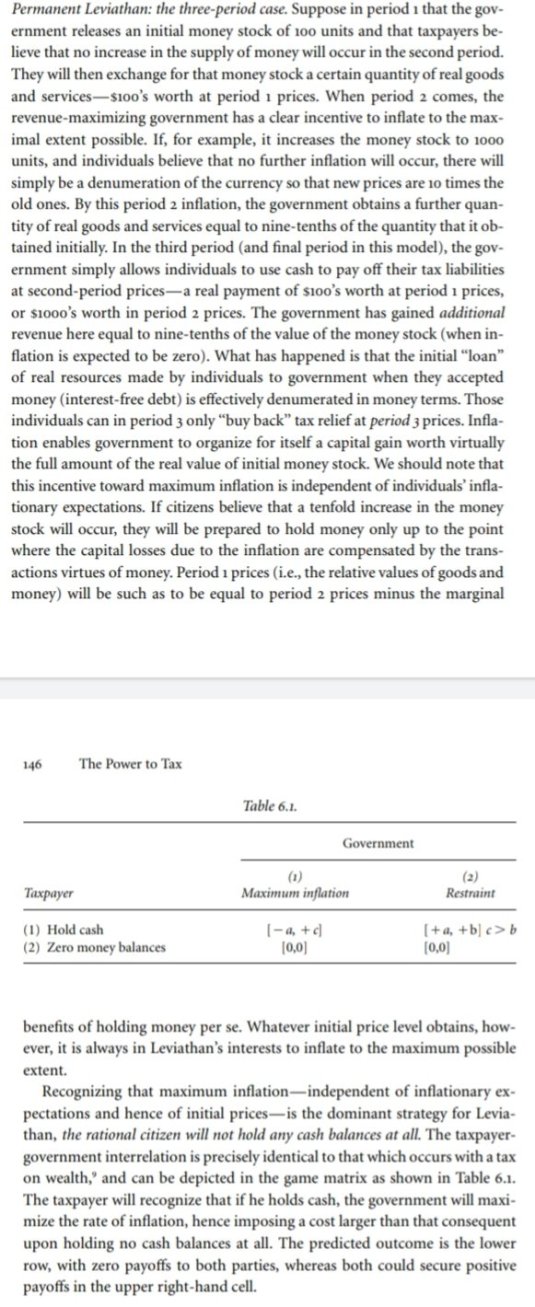

Brennan and Buchanan explain modern monetary theory in The Power to Tax (1980)

03 Jan 2020 Leave a comment

Champ and Freeman on modern monetary theory in action @AOC @BernieSanders

01 Jan 2020 Leave a comment

Champ and Freeman on modern monetary theory

31 Dec 2019 Leave a comment

in applied price theory, budget deficits, business cycles, economic history, fiscal policy, law and economics, macroeconomics, monetary economics, politics - USA, property rights Tags: 2020 presidential election, hyperinflation, monetary cranks, monetary policy

Maybe Freeman and Champ are explaining and refuting Modern Monetary Theory too

26 Aug 2019 Leave a comment

Declan Trott debunking debunker @ProfSteveKeen

08 Aug 2018 Leave a comment

in applied price theory, economics of information, economics of regulation, financial economics, history of economic thought, labour economics Tags: monetary cranks

Wouldn’t hold much hope for investors in a hedge fund founded by Steve Keen to put other’s money where his mouth is all the time

28 Apr 2018 Leave a comment

in business cycles, entrepreneurship, Euro crisis, financial economics, fiscal policy, global financial crisis (GFC), macroeconomics, monetary economics Tags: active investing, monetary cranks, revealed preference

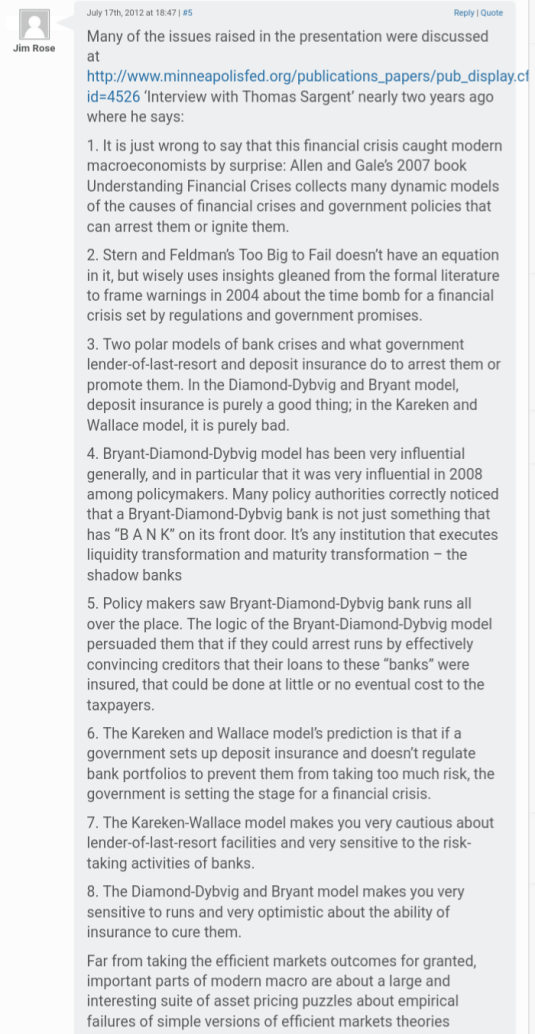

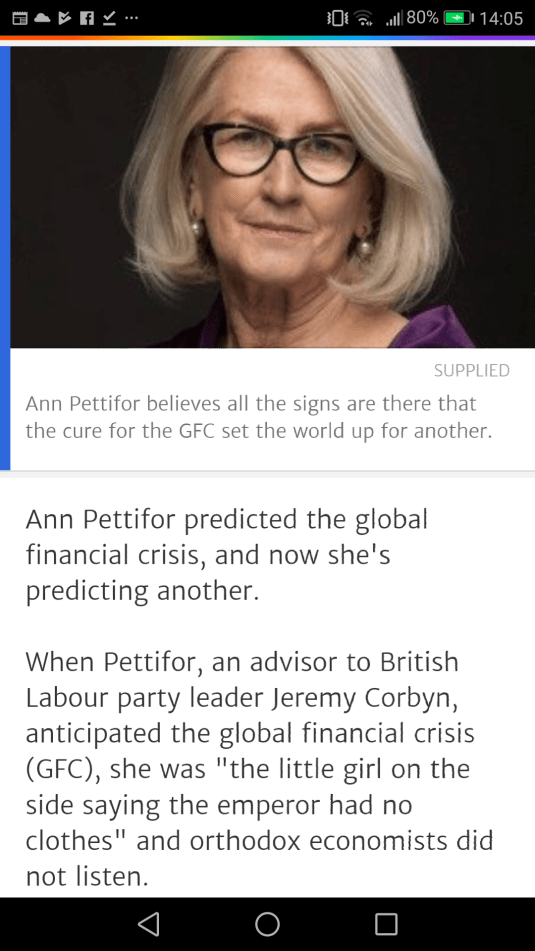

Thomas Sargent v. @AnnPettifor on macroeconomics before the #GFC

24 Apr 2018 Leave a comment

in budget deficits, business cycles, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics, monetary economics, Public Choice Tags: monetary cranks, Thomas Sargent

When will @AnnPettifor found a hedge fund to profit from putting other’s money where her mouth is rather than just her own retirement savings portfolio, which I am sure she did

23 Apr 2018 Leave a comment

in applied price theory, economics of information, entrepreneurship, fisheries economics, global financial crisis (GFC), macroeconomics, Marxist economics, monetary economics Tags: efficient markets hypothesis, entrepreneurial alertness, monetary cranks

The Tobin tax or @RobinHoodTax makes those monetary cranks in the social credit movement look credible!

31 Mar 2015 1 Comment

in macroeconomics, Milton Friedman, monetary economics Tags: monetary cranks, Robin Hood tax, Tobin tax

The Case for a RobinHoodTax.org on Financial Transactions goo.gl/sbL2JL #RobinHoodTaxUSA #RHT300B http://t.co/4lTAe1OMcU—

Robin Hood Tax (@RobinHoodTax) August 07, 2015

Sweden led the way with Tobin taxes in 1986: a 0.5% tax on the purchase or sale of an equity security. The revenues from the Tobin tax were initially expected to be 1,500 million Swedish kronor per year.

The actual revenues collected did not amount to more than 80 million Swedish kronor in any year and the average was closer to 50 million. Bond trading fell by more than 80 percent and the options market died. A lesson never learned by Tobin tax advocates. As taxable trading volumes fell, so did revenues from capital gains taxes, entirely offsetting the revenues from the equity transactions tax.

During the first week of the Swedish tax, the volume of bond trading fell by 85%; futures trading fell by 98%; and the options trading market disappeared. Trading for over 50% of Swedish equities moved to London by 1990. A true Robin Hood tax: the Tobin tax robbed from the Swedish capital gains taxman and gave to the British stamp duty taxman.

The Tobin tax is named after U.S. economist James Tobin who in 1972 suggested taxing foreign-exchange trades to limit currency speculation.

The Tobin tax on foreign-exchange transactions was to provide a disincentive for traders to make so many international transfers of money. Tobin in 1978 wrote that currency speculation can have ‘serious and painful internal economic consequences’. Tobin said his Tobin tax idea was unfeasible in practice.

Tobin and his idea of taxing of currency speculation improves market efficiency is total nonsense in theory as Milton Friedman explained:

The empirical generalization about the prevalence of destabilizing speculation, which is what gives the theoretical proposition its interest, seems to be one of those propositions that has gained currency the way a rumour does— each man believes it because the next man does, and despite the absence of any substantial body of well documented evidence for it.

Is the Tobin tax designed to raise 35 billion euros in revenue, as promised by EU Tax Commissioner Algirdas Semeta, or is it designed to curb speculation as was the original motivation by James Tobin to propose this tax?

Many have extolled such a tax as a potential source of earmarked revenues for a variety of purposes. Both left-wing and right wing populists have advocated the Tobin tax or Robin Hood tax to replace existing taxes or raise additional revenue.

Both types of populist advocate replacing or augmenting the income tax with a stamp duty. Enough people are familiar when stamp duties to realise that such a tax won’t raise much revenue. But if you call the stamp duty a Robin Hood tax, the media release suspends critical judgement and cheers them on.

Advocates of the Robin Hood tax blithely assert that the revenue raised will approximately equal 0.5% of the existing share and foreign exchange market turnover with few changes in behaviour or speculative activity, despite the imposition of a tax designed to curb speculation and reduce the total number of transactions significantly.

The $3.7 trillion-a-year Eurobond market came into being after JFK imposed an interest-equalization tax in 1963 to reduce investment in foreign securities by U.S. investors and to ease a so called balance of payments deficit.

What is the point of a Tobin tax if you already have a capital gains tax?. New Zealand doesn’t have a capital gains tax but it does have a tax on assets bought with the intention of resale rather than long-term income.

Why do share markets fall after the announcement of a Tobin tax? Trading in a more stable market should be value enhancing and increase share prices? Ditto exporters and more stable currency prices etc.? Exporter share prices should increase because of less need to hedge? Numerous studies find a significant reduction in equity turnover following a stamp duty introduction.

I am sure that with the City of London as a global financial centre, the British are cheering on efforts of other EU members to sabotage their own financial markets with a Tobin tax. FX turnover in the City of London reached over $1.8 trillion every day in 2010, accounting for 36.7% of the global total. About half of European investment banking activity is conducted through London.

Ed Prescott estimates a large quantity of intermediated borrowing-lending between households – several times GDP. A large amount of resources is used in this intermediation – a conservative estimate is 4% of GNP.

Prescott also argued that the cost of transferring financial assets has fallen dramatically – from 2% towards zero on Vanguards Indexed ETF. The spread between borrowing and lending by households down – the spread on home mortgages was 3% in 1960s – now about 2%. None of these trends bode well for either a large tax base or growing tax base.

Another way to think about a Tobin tax is to consider it to be a tax on ATM withdrawals. There was such a debits tax on bank withdrawals of $.20 in my home State of Tasmania in the 1980s.

Naturally, a Tobin tax on ATM withdrawals is not a tax on any sort of real economic activity. People would simply make fewer ATM withdrawals and look for other ways to not use ATMs. It is routine for cash balances to respond to the time and other costs of replenishing money balances, and the fixed cost of using deposits for purchases.

Time I want back on my deathbed: listening to social credit and other monetary cranks

02 Sep 2014 1 Comment

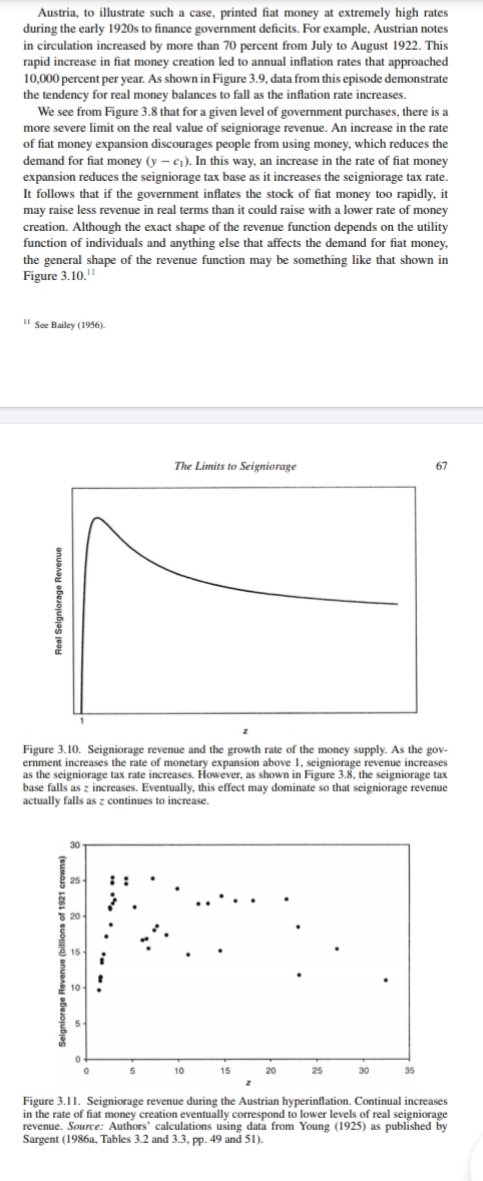

in Austrian economics, business cycles, economic growth, inflation targeting, monetarism, monetary economics, Murray Rothbard Tags: Austrian school of economics, business cycle, fractional reserve banking, hyperinflation, inflation, monetary business cycle, monetary cranks, quantity theory of money

I lost a good 15 minutes of my life that I will not get back on my deathbed listening to some monetary cranks at a Meet the Candidates forum last night for the New Zealand general election.

Monetary cranks advocate boundless inflation and credit expansion as the patent medicine for all our economic ills:

those who have Found the Light about Money take up their pens and write, with a conviction, a persistence and a devotion otherwise only found among the disciples of a new religion.

It is easy to scoff at these productions: it is not so easy always to see exactly where they go wrong. It is natural that practical bankers, vaguely conscious that the projects of monetary cranks are dangerous to society, should cling in self-defence to the solid rock, or what they believe to be so, of tradition and accepted practice. But it is not open to the detached student of economics to take refuge from dangerous innovation in blind conservatism.

D.H. Robertson (1928)

Listening to these monetary cranks in the audience last night rates with the worst movies I have ever ever seen for time I want back my deathbed. I think the worst movie I have ever seen was Absolute Beginners starring David Bowie. After that it, might be Last Tango in Paris.

These particular monetary cranks with their obsessions about factional reserve banking are from the social credit party in New Zealand. They are followers of Major C.H. Douglas, whom Keynes referred to as a:

private, perhaps, but not a major in the brave army of heretics

Social credit and other monetary cranks believe that all the world’s problems will be sold if the reserve bank prints money and they seem to think that was really easy because there is a fractional reserve banking system.

No one in the room who knew better wanted to lose more time that they wanted back on their deathbed explaining why printing money doesn’t make you richer. The “money is wealth” error is the defining affliction of the monetary crank.

The good economist will know that money creation is no short-cut to wealth. Only the production of valued goods and services in a market which reflects the consumer’s willingness to pay can relieve poverty and promote prosperity. A people are prosperous to the extent they possess goods and services, not money. All the money in the world—paper or metallic—will still leave one starving if goods and services are not available.

Obviously, none of them were persuaded by the quantity theory of money: if you increase the supply of money without a matching increase in the rate of real growth in the production of goods and services, you’ll have more money chasing the same amount of goods so prices will go up. It’s called inflation. Printing money creates inflation.

There is a school of thought in economic school, the Austrian school of economics, does get excited about fractional reserve banking. The reason it does is to explain how fractional reserve banking creates inflation and promotes the business cycle.

A cycle of booms and busts is not looked upon as a good thing by the Austrian school of economics.

The Austrian school wants to get rid of fractional reserve banking as a way of reducing inflation and reducing the possibility of a loose monetary policy causing booms and busts in the economy.

These monetary cranks from social credit party honestly believed that printing more money will make you wealthier. Thankfully no one asked them to explain their position.

A few supporters of the monetary cranks in the audience asked other members of their views on the ideas of these monetary cranks. Sensibly, they all gave short answers that did not provoke them further and waste more of their precious life listening to them talk nonsense.

If printing money was a winner, as with any populist policy that has a half a chance of working, the parties of the centre-left and centre right would be all over it like flies to s…

Recent Comments