I didn’t really read the housing section of last week’s Reserve Bank MPS – housing isn’t their responsibility and their analysis of it has rarely been up to much, often lurching unpredictably from one story to another. And their new material on house prices in each MPS only stems from the Remit change Grant Robertson foisted on them early in the year, knowing it would make no substantive difference to anything, but designed to look as though the government cared.

So it was only when the Herald’s Thomas Coughlan tweeted this chart yesterday that I noticed it.

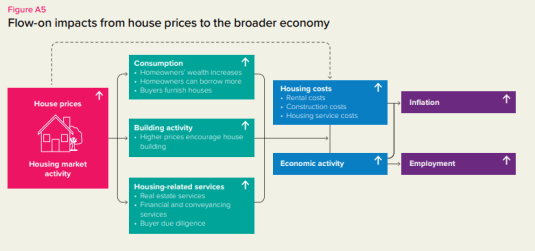

The chart is prefaced with this text

The MPC sets monetary policy to achieve its inflation and employment objectives in the Remit. It considers the outlook for the housing market because house prices can influence broader economic activity, employment, and consumer price inflation (figure A5).

So we are presumably supposed to take this…

View original post 2,099 more words

Recent Comments