via The Ten Pillars of Economic Wisdom, David Henderson | EconLog | Library of Economics and Liberty.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

10 May 2015 Leave a comment

in applied price theory, applied welfare economics, Austrian economics, comparative institutional analysis, constitutional political economy, development economics, economic history, economics of education, economics of information, economics of media and culture, economics of regulation, energy economics, entrepreneurship, financial economics, health economics, history of economic thought, industrial organisation, survivor principle Tags: David Anderson, evidence-based policy, offsetting behaviour, pretence to knowledge, The fatal conceit, unintended consequences

via The Ten Pillars of Economic Wisdom, David Henderson | EconLog | Library of Economics and Liberty.

09 May 2015 Leave a comment

in applied price theory, applied welfare economics, Austrian economics, comparative institutional analysis, constitutional political economy, economics of regulation, F.A. Hayek Tags: Constitution of Liberty, cost benefit analysis, evidence-based policy, offsetting behaviour, The fatal conceit, The pretence to knowledge, unintended consequences

Happy Birthday, F.A. Hayek!

(8 May 1899 – 23 March 1992) http://t.co/K431Kj9nok—

Screwed by State (@ScrewedbyState) May 09, 2015

09 May 2015 Leave a comment

in Austrian economics, F.A. Hayek Tags: FA Hayek

05 May 2015 1 Comment

in Austrian economics, entrepreneurship, Marxist economics, politics - New Zealand Tags: schools, state owned enterprises

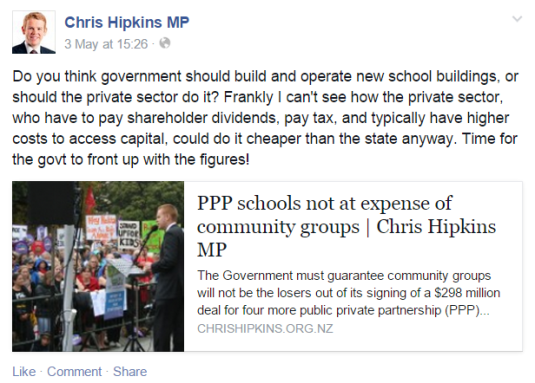

At least one Labour MP must have watched the other channel when the Berlin Wall fell. How else could Chris Hipkins, MP ever think that government provision is cheaper because they don’t have to make a profit? OK, he was a teenager when the Berlin Wall fell, but even teenagers watch the headline news or pick up the gist of the headlines from friends.

The tidiest of all Marxist arguments, the saddest of all Marxist arguments is government operation of businesses is cheaper because they don’t have to make a profit. At least we were spared the cliché “people not profits”.

Leaving to one side that government school buildings are built by private contractors to the Ministry of Education, let’s focus on whether government businesses will be cheaper because they don’t have to make a profit.

No cheap shots about how the portfolio of state owned enterprises are worth $30 billion returned a profit of $20 million to New Zealand taxpayers last year or of the inherent flaws of government ownership:

On the free market, in short, the consumer is king, and any business firm that wants to make profits and avoid losses tries its best to serve the consumer as efficiently and at as low a cost as possible.

In a government operation, in contrast, everything changes. Inherent in all government operation is a grave and fatal split between service and payment, between the providing of a service and the payment for receiving it.

The government bureau does not get its income as does the private firm, from serving the consumer well or from consumer purchases of its products exceeding its costs of operation.

No, the government bureau acquires its income from mulcting the long-suffering taxpayer. Its operations therefore become inefficient, and costs zoom, since government bureaus need not worry about losses or bankruptcy; they can make up their losses by additional extractions from the public till.

The accounting profit or loss of any firm combines two rather different concepts of profit:

Normal profit is simply at the cost of raising capital from investors. This capital can be borrowed in the form of a loan or can be equity.

Chris Hipkins, MP concedes a need to borrow capital when he talks about government typically having lower costs to access capital in the screenshot above. Both private and public builders of schools will have to pay to access capital.

Economic profit is a far more complicated concept frequently misunderstood, especially by Marxists, the Left over Left and, of course, professional media commentators. As Mises explains:

If all people were to anticipate correctly the future state of the market, the entrepreneurs would neither earn any profits nor suffer any losses. They would have to buy the complementary factors of production at prices which would, already at the instant of the purchase, fully reflect the future prices of the products. No room would be left either for profit or for loss.

What makes profit emerge is the fact that the entrepreneur who judges the future prices of the products more correctly than other people do buys some or all of the factors of production at prices which, seen from the point of view of the future state of the market, are too low. Thus the total costs of production — including interest on the capital invested — lag behind the prices which the entrepreneur receives for the product. This difference is entrepreneurial profit.

Profits arise from the dynamism of the market and the ability of superior entrepreneur’s to anticipate the future better than others for which there is always only a temporary profit:

Profits are never normal. They appear only where there is a maladjustment, a divergence between actual production and production as it should be in order to utilize the available material and mental resources for the best possible satisfaction of the wishes of the public. They are the prize of those who remove this maladjustment; they disappear as soon as the maladjustment is entirely removed.

Frank Knight in Risk, Uncertainty, and Profit (1921) distinguished between interest on capital that is lend as either a loan or equity – long-run normal profits – and the short-run profits and losses earned by superior, or suffered by inferior entrepreneurs , respectively. This entrepreneurial superiority or inferiority flows from the ability to forecast the uncertain future. Those entrepreneurs “with superior knowledge and superior foresight,” wrote Frank Fetter, “are merchants, buying when they can in a cheaper and selling in a dearer capitalisation market, acting as the equalizers of rates and prices.”

Knight argued that entrepreneurs earn profits as a return for putting up with uncertainty and anticipating uncertainty faster than the rest. Many businesses are unprofitable because of rising costs or falling sales that were not anticipated. The Knightian concept is of the profit-seeking entrepreneur investing resources under uncertainty about market demand and costs in the future.

Alchian (1950) illustrated the unreliability of cost estimation with the range of bids made in government tendering processes. When contractors bid for the same project, these entrepreneurs routinely disagree over its likely cost by margins of 20 percent. These tenderers are predicting their own costs, about which they are knowledgeable, and they have an incentive to be truthful to win the initial tender.

Profits and losses, by rewarding and penalising the entrepreneurs who are not the quickest, ensures that only what consumers want is bought to the market as Henry Hazlett explains:

In a free economy, in which wages, costs, and prices are left to the free play of the competitive market, the prospect of profits decides what articles will be made, and in what quantities—and what articles will not be made at all.

If there is no profit in making an article, it is a sign that the labour and capital devoted to its production are misdirected: the value of the resources that must be used up in making the article is greater than the value of the article itself.

Profits arise as the reward for superior foresight into the future and innovation. Both of these concepts are not associated with government run businesses as Alfred Marshall explained:

A government could print a good edition of Shakespeare’s works, but it could not get them written.

As for Hipkins’ argument that governments can borrow at a cheaper rate than private firms, Bailey and Jensen (1972) said:

…we argue that efficient allocation of risk bearing is usually more difficult for government projects than it is for private ones. Therefore, if anything, the allowance for risk should be greater for government projects than it is for otherwise comparable private ones…

We find no support for the arguments in favor of using the government bond rate or any other such universally low rate for discounting costs and benefits of public projects.

We concur in Hirshleifer’s conclusion that a public project with given attributes (in terms of dispersion of possible future outcomes and of the covariance of these outcomes with those for existing portfolios) should he discounted with at least as high a rate as a similar private project.

This “same rate” should include the appropriate allowances for taxes and other distortions in private markets (as outlined by Harberger) as well as the appropriate allowances for risk, which we have outlined above.

Moreover, if private markets in risk are as “imperfect” as many have claimed, that merely tends to increase the rate that should be used, because the government is even less able to distribute risks than are these markets.

01 May 2015 Leave a comment

in applied price theory, Austrian economics, F.A. Hayek, labour supply, occupational choice, Public Choice, rentseeking Tags: consultants, rent seeking, The pretence to knowledge

The life of an economist. http://t.co/gvBLa9Tk3h—

Justin Wolfers (@JustinWolfers) March 02, 2015

27 Mar 2015 Leave a comment

in applied price theory, applied welfare economics, Austrian economics, comparative institutional analysis, constitutional political economy, F.A. Hayek, liberalism, Public Choice, rentseeking Tags: evidence-based policy, offsetting behaviour, science and public policy, The fatal conceit, The pretence to knowledge, unintended consequences

Scientists dream about what could be.

Economists remind you of price tags and unintended consequences

14 Mar 2015 Leave a comment

in applied price theory, Austrian economics Tags: market process, The meaning of competition

13 Mar 2015 Leave a comment

in applied price theory, Austrian economics, behavioural economics, comparative institutional analysis, entrepreneurship, industrial organisation, survivor principle Tags: efficient markets hypothesis, entrepreneurial alertness, Paul Samuelson

via Samuelson vs. Friedman, David Henderson | EconLog | Library of Economics and Liberty and An Interview With Paul Samuelson, Part One — The Atlantic.

04 Mar 2015 7 Comments

in applied price theory, Austrian economics, entrepreneurship, F.A. Hayek, George Stigler, human capital, industrial organisation, job search and matching, labour economics, law and economics, Ludwig von Mises, politics - New Zealand, survivor principle Tags: Armen Alchian, employment law, employment protection laws, entrepreneurial alertness, France, Israel Kirzner, The fatal conceit, The pretence to knowledge

As discussed yesterday, if the Employment Court had its way, New Zealand case law under the Employment Relations Act regarding redundancies and layoffs would be as job destroying as those in France.

The Employment Court’s war against jobs goes back more than 20 years. To 1991 and G N Hale & Son Ltd v Wellington etc Caretakers etc IUW where the Court held that a redundancy to be justifiable under law it must be ‘unavoidable’, as in redundancies could only arise where the employer’s capacity for business survival was threatened.

The Court of Appeal slapped that down and affirm the right of the employer to manage his business in no uncertain terms:

…this Court must now make it clear that an employer is entitled to make his business more efficient, as for example by automation, abandonment of unprofitable activities, re-organisation or other cost-saving steps, no matter whether or not the business would otherwise go to the wall…

The personal grievance provisions … should not be treated as derogating from the rights of employers to make management decisions genuinely on such grounds. Nor could it be right for the Labour Court to substitute its own opinion as to the wisdom or the expediency of the employer’s decision.

When a dismissal is based on redundancy, it is the good faith of that basis and the fairness of the procedure followed that may fall to be examined on a complaint of unjustifiable dismissal

… the Court and the grievance committees cannot properly be concerned with an examination of the employer’s accounts except in so far as it bears on the true reason for dismissal.

The Employment Court could only inquire as to the genuineness of the employer’s decision and the procedures adopted. The Court could not substitute their views on management decisions. No second-guessing.

In Brake v Grace Team Accounting Ltd, the Employment Court found its way back into second-guessing employer’s decisions about how to manage their business. The figures used by the employer to decide that a redundancy was required were in error. The employer miscalculated.

The Employment Court had previously held in Rittson-Thomas T/A Totara Hills Farm v Hamish Davidson that the statutory test of what a fair and reasonable employer could have done in all the circumstances applies to the substantive reasoning for redundancies. Some enquiry into the employer’s substantive decision is required to establish that a hypothetical fair and reasonable employer could also make the same decision in all of the circumstances.

Subsequently in Brake v Grace Team Accounting Ltd, the Employment Court found that the actions by the employer were “not what a fair and reasonable employer would have done in all the circumstances” and “failed to discharge the burden of showing that the plaintiff’s dismissal for redundancy was justified”.

The Court found that the redundancy was “a genuine, but mistaken, dismissal”, but it still found that the dismissal was substantively unjustified. That is a major new development. Mistaken dismissals that are genuine are unlawful and grounds for compensation under the employment law.

The case was appealed where the issues were whether the correct test had been applied. The Court of Appeal, in a sad day for employers, job creation and the unemployed, found that the Employment Court was within its rights to do what it did and applied the statutory tests correctly:

GTA acted precipitously and did not exercise proper care in its evaluation of its business situation and it made its decision about Ms Brake’s redundancy on a false premise.

So it never turned its mind to what its proper business needs were but rather proceeded to evaluate its options based on incorrect information. We can see no error in the finding by the Employment Court that a fair and reasonable employer would not do this.

The test is now that fair and reasonable employers in New Zealand do not make mistakes. A much greater burden is now laid upon employers to show that not only that redundancies are justified, but they have made careful calculations and no mistakes.

No more seat of your pants entrepreneurship in New Zealand. No more entrepreneurial hunches – the essence of entrepreneurship is acting on hunches and other judgements that are incapable of being articulated to others and about which there is mighty disagreement in many cases. As Lavoie (1991) states:

…most acts of entrepreneurship are not like an isolated individual finding things on beaches; they require efforts of the creative imagination, skillful judgments of future costs and revenue possibilities, and an ability to read the significance of complex social situations.

The essence of entrepreneurship is your hunches are better than the next guy’s and you survive in competition by backing that hunch often to the consternation of the crowd. As Mises explains:

[Economics] also calls entrepreneurs those who are especially eager to profit from adjusting production to the expected changes in conditions, those who have more initiative, more venturesomeness, and a quicker eye than the crowd, the pushing and promoting pioneers of economic improvement…

The entrepreneurial idea that carries on and brings profits is precisely that idea which did not occur to the majority… The prize goes only to those dissenters who do not let themselves be misled by the errors accepted by the multitude

In many cases, those entrepreneurial hunches are sorted, sifted and selected on the basis of trial and error in the marketplace. Central to Hayek’s conception of the meaning of competition is it is a process of trial and error with many errors:

Although the result would, of course, within fairly wide margins be indeterminate, the market would still bring about a set of prices at which each commodity sold just cheap enough to outbid its potential close substitutes — and this in itself is no small thing when we consider the insurmountable difficulties of discovering even such a system of prices by any other method except that of trial and error in the market, with the individual participants gradually learning the relevant circumstances.

Remember Hayek’s conception of competition as a discovery procedure where prices and production emerge through the clash of entrepreneurial judgements and competitive rivalry:

…competition is important only because and insofar as its outcomes are unpredictable and on the whole different from those that anyone would have been able to consciously strive for; and that its salutary effects must manifest themselves by frustrating certain intentions and disappointing certain expectations

Errors are no longer permitted in the New Zealand labour market by the Employment Court. The Court has outlawed error in redundancy decisions.

This is despite the fact that the conception by Kirzner of the market process is that it is an error correction procedure without rival and a central role of entrepreneurial alertness is to correct errors in pricing and production:

It is important to notice the role played in this process of market discovery by pure entrepreneurial profit. Pure profit opportunities emerge continually as errors are made by market participants in a changing world. The inevitably fleeting character of these opportunities arises from the powerful market tendency for entrepreneurs to notice, exploit, and then eliminate these pure price differentials.

The paradox of pure profit opportunities is precisely that they are at the same time both continually emerging and yet continually disappearing. It is this incessant process of the creation and the destruction of opportunities for pure profit that makes up the discovery procedure of the market. It is this process that keeps entrepreneurs reasonably abreast of changes in consumer preferences, in available technologies, and in resource availabilities.

Rothbard made similar arguments about the centrality of discrepancies and error in entrepreneurship:

The capitalist-entrepreneur buys factors or factor services in the present; his product must be sold in the future. He is always on the alert, then, for discrepancies, for areas where he can earn more than the going rate of interest.

In Frank Knight’s conception of profit, there were temporary profits that arise from the correction of error:

In the theory of competition, all adjustments “tend” to be made correctly, through the correction of errors on the basis of experience, and pure profit accordingly tends to be temporary.

The Employment Court misunderstands the market process as a process of error correction. Those errors are identified through entrepreneurial alertness and trial and error. These errors are both of over-optimism and over-pessimism as Kirzner explains:

Errors of over-pessimism are those in which superior opportunities have been overlooked. They manifest themselves in the emergence of more than one price for a product which these resources can create. They generate pure profit opportunities which attract entrepreneurs who, by grasping them, correct these over-pessimistic errors.

The other kind of error, error due to over-optimism, has a different source and plays a different role in the entrepreneurial discovery process. Over-optimistic error occurs when a market participant expects to be able to complete a plan which cannot, in fact, be completed.

A considerable part of entrepreneurial alertness arises from the business opportunities created by sheer ignorance and pure error as Kirzner explains:

What distinguishes discovery (relevant to hitherto unknown profit opportunities) from successful search (relevant to the deliberate production of information which one knew one had lacked) is that the former (unlike the latter) involves that surprise which accompanies the realization that one had overlooked something in fact readily available. (“It was under my very nose!”)

The market process is a selection procedure where the more efficient survive for reasons that may be unknown to the entrepreneurs directly concerned as well as to observers and officious judges. Alchian pointed out the evolutionary struggle for survival in the face of market competition ensured that only the profit maximising firms survived:

The surviving firms may not know why they are successful, but they have survived and will keep surviving until overtaken by a better rival. All business needs to know is a practice is successful.

One method of organising production and supplying to the market will supplant another when it can supply at a lower price (Marshall 1920, Stigler 1958). Gary Becker (1962) argued that firms cannot survive for long in the market with inferior product and production methods regardless of what their motives are. They will not cover their costs.

The more efficient sized firms are the firm sizes that are currently expanding their market shares in the face of competition; the less efficient sized are those firms that are currently losing market share (Stigler 1958; Alchian 1950; Demsetz 1973, 1976). Business vitality and capacity for growth and innovation are only weakly related to cost conditions and often depends on many factors that are subtle and difficult to observe (Stigler 1958, 1987). The Employment Court pretends to know better than the outcome of the competitive struggle in the market for survival.

The Employment Court also believes employers have something akin to academic tenure. In 2010, the Court found that an employee’s redundancy was unjustified because the employer did not offer redeployment and there is no requirement that the right of the redeployment be written into the employment agreement (Wang v Hamilton Multicultural Services Trust). The particulars of this case were quite interesting:

In the case at hand, the Employment Court held that the employer was obliged to look for alternatives to making the employee redundant. Given that he would be able to perform the new finance manager position with some up-skilling, the employer should have offered him the position rather than simply inviting him to apply for it.

The notion that an employee through training can quickly increase their marginal productivity by 50% to fill a more senior role contradicts the modern labour economics of human capital. A 50% salary increase through a bit of training would imply extraordinary annual returns on other forms of on-the-job training and formal education as well as the training at hand in the Employment Court case.

I would very much like to be in the position where I can get a 50% salary increase after a bit of training. As I recall, I required about 5-10 years of on-the-job human capital acquisition before my starting salary as a graduate was 50% higher through promotion and transfers.

In summary, the Employment Court stands apart from the modern labour economics of human capital and job search and matching as well as the modern theory of entrepreneurial alertness, and the market as a discovery procedure and an error correction mechanism. The Employment Court has fallen for both the pretence to knowledge and the fatal conceit.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Economics, public policy, monetary policy, financial regulation, with a New Zealand perspective

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Restraining Government in America and Around the World

Recent Comments