How did the Chinese billionaires make their money?

15 Feb 2016 Leave a comment

in applied price theory, development economics, economic history, entrepreneurship, growth miracles, human capital, industrial organisation, labour economics Tags: billionaires, China, entrepreneurial alertness, superstars, top 1%

Percentage of billionaires who inherited their wealth

14 Feb 2016 Leave a comment

in applied welfare economics, entrepreneurship, labour economics, poverty and inequality Tags: entrepreneurial alertness, inherited wealth, superstar wages, superstars, top 1%

China has been capitalist for long enough for a billionaire to actually inherit his wealth.

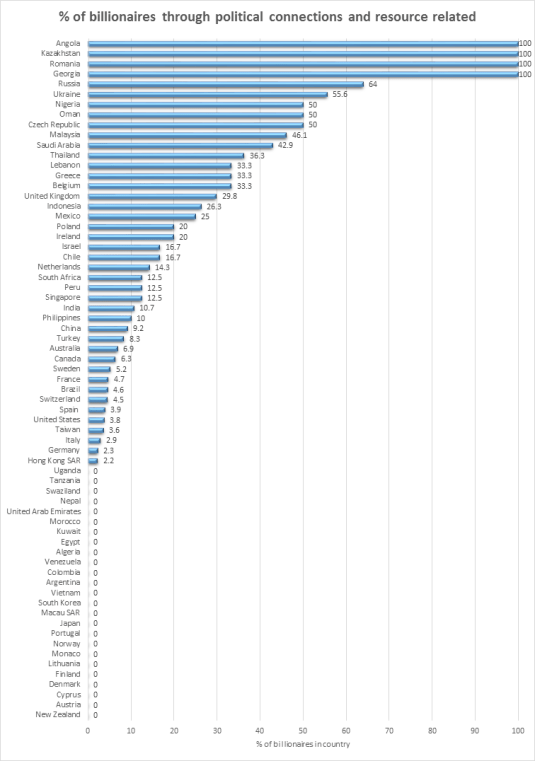

% billionaires who made their money through political connections or resource industries

13 Feb 2016 Leave a comment

in economics of bureaucracy, economics of regulation, energy economics, entrepreneurship, industrial organisation, poverty and inequality, privatisation, rentseeking, resource economics

The 1826 Billionaires in the Forbes 2015 list are classified as rich through political connections if they made their money through past political positions, close relatives or friends in government, or questionable licenses, privatisations or resource extraction industries.

All privatizations were included in the politically-connected/resource-related category despite my data source acknowledging the possibility that the new owners may have transformed the company. Resource billionaires were all deemed to be lucky or cronies by my data source rather than diligent as some most certainly were. This is something of a slur by my data source given the industriousness of some resource billionaires some of whom were even geologists.

Political cronyism is a path to billionaire wealth mainly in the developing countries. Less than 10% of Chinese billionaires made their money through political connections, which is surprising.

Cmon aussie c’mon original

13 Feb 2016 Leave a comment

in cricket, economic history, economics of information, economics of media and culture, entrepreneurship, industrial organisation, Ronald Coase, sports economics Tags: advertising, Australia, entrepreneurial alertness

Lynne Kiesling discusses Joseph Schumpeter

13 Feb 2016 Leave a comment

in entrepreneurship, history of economic thought, industrial organisation, Joseph Schumpeter

Colour films were initially thought to be uncompetitive on cost grounds

12 Feb 2016 Leave a comment

in economic history, entrepreneurship, industrial organisation Tags: creative destruction, Hollywood economics

How often does the human driver take over a self-driving car?

11 Feb 2016 Leave a comment

in entrepreneurship, technological progress, transport economics

@LivingWageUK documents the Achilles heel of the #livingwage

09 Feb 2016 1 Comment

in applied price theory, economics of bureaucracy, economics of regulation, entrepreneurship, managerial economics, minimum wage, organisational economics, personnel economics, politics - New Zealand, Ronald Coase, theory of the firm

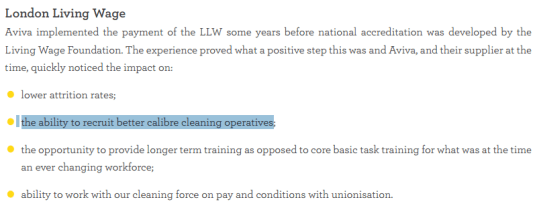

Research publicised by a Living Wage UK highlighted the Achilles heel of any living wage proposal. This Achilles heel applies to the voluntary adoption of the living wage and a living wage mandated through minimum wage laws.

The critique to follow accepts pretty much everything claimed by the living wage movement about the benefits of the living wage but simply traces out the consequence of this one promised benefit.

Source: New evidence of business case for adopting Living Wage Living Wage Foundation.

The living wage is substantially above the minimum wage. Offering the living wage will change the composition of the recruitment pool of low-wage employers. This is the Achilles heel of the living wage which Living Wage UK documents in its study it tweeted about and from which I have taken the above snapshot.

Jobseekers would not have considered vacancies by these employers will now apply because of the living wage increase. These better calibre applicants will win those jobs ahead of the jobseekers whose current productivity levels are less than that to justify the cost of the living wage.

Central to the living wage rhetoric is that somehow employees will be more productive because of the adoption of the living wage.

The simplest way of doing that for an employer is to hire more qualified, more productive employers are no longer a hire the type of people you currently hire. They will be unemployed or pushed into the non-living wage sector of the low-wage market.

Best 2 Minimum Wage Cartoons Ever, from Henry Payne, Updated for Seattle's $15 "Economic Death Wish" @HenryEPayne http://t.co/vatUzkHMss—

Mark J. Perry (@Mark_J_Perry) August 18, 2015

A living wage is an exclusionary policy where ordinary workers, often with families who are not productive enough to produce $19.25 per hour living wage plus overheads will never be interviewed.

The workers with the type of skills that currently win those jobs covered by a living wage increase will not be shortlisted because the quality of the recruitment pool will increase because of the living wage.

There will be an influx of more skilled workers attracted by the higher wages for living wage jobs. They will go to the head of the queue and displaced workers who currently apply for and win these jobs before the adoption of the living wage.

Any extra labour productivity from paying a living wage increase is in doubt because low skilled service sectors are notorious for their low potential for productivity gains. They are the bread-and-butter of Baumol’s disease.

The modern theories of the firm focus, in part or in full on reducing opportunistic behaviour, cheating and fraud in employment relationships. The cost of discovering prices and making and enforcing contracts and getting what you pay for are central to Coase’s theory of the firm put forward in 1937.

The profits of entrepreneurs for running a firm is directly linked from their successful policing of the efforts of employees and sub-contractors to ensure the team and each member perform as promised and individual rewards matched individual contributions (Alchian and Demsetz 1972; Barzel 1987). Alchian and Demsetz’s (1972) theory of the firm focused on moral hazard in team production. As they explain:

Two key demands are placed on an economic organization-metering input productivity and metering rewards.

The main rationale in personnel economics from everything ranging from employer funding of retirement pensions to the structure of promotions and executive pay including stock options is around better rewarding self-motivating employees who strive harder and reducing the costs of monitoring employee effort.

At bottom, the efficiency wage hypothesis is entrepreneurs are unaware of the higher quality and greater self-motivation of better paid recruits for vacancies but wise bureaucrats and farsighted politicians notice these gaps in the market. Bureaucrats and politicians notice these gaps in the market before those who gain from superior entrepreneur alertness to hitherto untapped opportunities for profit do so and instead leave that money on the table.

It’s kicking the living wage movement when it is down to mention that low paid workers with families will lose a considerable part of the living wage increase because of reductions in family tax credits and in-kind assistance from the government that are linked to their pay.

Their jobs are put at risk because of a large increase in the cost of employing them to their employers. Their take-home pay after taxes, family tax credits and other government assistance increases by much less. This is a pointless gamble with job security because of the much small increase in the take-home pay of many breadwinners on the living wage.

Creative destruction in smart phone market shares

09 Feb 2016 Leave a comment

in economics of media and culture, entrepreneurship, industrial organisation, survivor principle Tags: cell phones, creative destruction, Iphone, smart phones

Here’s where Republicans and Democrats differ on the role of government

08 Feb 2016 Leave a comment

in defence economics, economics of bureaucracy, economics of education, economics of information, economics of media and culture, economics of regulation, energy economics, entrepreneurship, environmental economics, income redistribution, politics - USA, Public Choice, rentseeking Tags: 2016 presidential election Republican Party, Democratic Party, votor demographics

@OwenJones84 @K_Niemietz Venezuelan, Chilean and Chinese index of economic freedom rankings 2016

06 Feb 2016 Leave a comment

in development economics, economics of regulation, entrepreneurship, fiscal policy, growth disasters, growth miracles, industrial organisation, labour economics, law and economics, macroeconomics, monetary economics, property rights, public economics Tags: capitalism and freedom, Chile, China, The Great Escape, Venezuela

Much more than a high minimum wage – Puerto Rican, Mexican and U.S. Doing Business rankings 2015

05 Feb 2016 Leave a comment

in economics of religion, entrepreneurship, industrial organisation, law and economics, politics - USA, property rights Tags: doing business, Mexico, Puerto Rico

Having a high minimum wage is the least of the problems that the US territory of Porto Rico has when you consider reasons from its recent sovereign default. It owes about US$70 billion. It is a terrible place to do do business – worse than Mexico! Mexicans find it easier to export to the USA!

@RusselNorman @JulieAnneGenter a hedge fund specialises in shorting renewable energy shares @Greenpeace

03 Feb 2016 Leave a comment

in defence economics, economic history, economics of regulation, energy economics, entrepreneurship, environmental economics, financial economics, global warming Tags: active investing, disinvestment, entrepreneurial alertness, ethical investing, Fossil Fuels, green rentseeking, hedge funds, passive investing, renewable energy, solar power, Vice Fund, wind power

Just as the Vice Fund specialises in investing in tobacco, alcohol, gaming and defence shares, Cool Futures Funds Management is starting-up to specialise in betting against global warming by shorting green stocks:

…instead of renewables being our energy future, they’re betting on the subsidies drying up and the whole industry collapsing; instead of fossil fuels being left in the ground as “stranded assets”.

An example of the nice little earners this hedge fund can come across is anticipating when particular investors will want to disinvest from fossil fuels.

When institutional investors ranging from universities to sovereign investment funds such as the New Zealand Superannuation Fund seek to disinvest from fossil fuels, that will be a good time to buy cheap shares.The

YouTube The Geography of Genius: How Place and Culture Shape Creativity

02 Feb 2016 Leave a comment

in entrepreneurship Tags: superstars

Review of #TheBigShort including of the movie

02 Feb 2016 Leave a comment

in applied price theory, business cycles, economic history, entrepreneurship, financial economics, global financial crisis (GFC), great recession, macroeconomics, monetary economics, movies Tags: bank runs, financial crises

About the only time the Hollywood Left oozes with patriotism is when getting stuck into Wall Street. Hollywood must get its revenge for all those times investors did not back their film pitches, trimmed budgets and get the lion’s share of merchandising royalties and syndication profits. As Larry Ribstein explained:

American films have long presented a negative view of business…. it is not business that filmmakers dislike, but rather the control of firms by profit-maximizing capitalists… this dislike stems from filmmakers’ resentment of capitalists’ constraints on their artistic vision.

The Big Short is still a good film despite the left-wing populism, worth going to see. Its limitations in not discussing the monetary policy of The Fed or regulations that encouraged lending to high risk borrowers are justified poetic license and editing.

The film is already 120+ minutes long despite frequent resorts to breaking the fourth wall to explain technical terms, who was what and what they were doing, past and present. The Big Short is a film designed it make money at the box office, not a semester long documentary.

The Big Short is well acted, funny, insightful and still a good story despite the documentary element that was impossible to do without.

The Big Short highlights that its protagonists had skin in the game. They were investing in mortgages or shorting the same in the expectation of a crash. There were no windbags and armchair critics in The Big Short talking gloom and doom on the horizon without investing their own money to profit from their forecasts. That said, the protagonists betting on a sub-prime mortgages crash, bar two of them, were a little bit nutty.

I do not know any of the critics of the economics of the film’s explanation of the sub-prime crisis who suggested how they could fix these gaps in its economics without making the film much, much longer.

These critics fall into the exact same trap that the Big Short was not about. The Big Short was about investors to put their money where their mouth is. The critics of the film should put their script doctoring skills where their mouths are at least of The Big Short.

Source: What ‘The Big Short’ Gets Right, and Wrong, About the Housing Bubble – The New York Times.

Getting stuck into the role of the Fed and regulatory mandates on the banks regarding their level of sub-prime mortgages is for another film. Plenty of people warned of dark days ahead. An essay anyone can read with profit is Ross Levine’s “An Autopsy of the U.S. Financial System: Accident, Suicide, or Negligent Homicide?“

Other films, correctly documentaries, place the blame for the sub-prime crisis and the Great Recession directly on the Fed:

The financial mess we’re still climbing out of can be laid directly at the feet of the Fed, whose misguided advocacy, under Greenspan, of a borrow-and-spend economy rather than a focus on savings and investment has created a situation where, as the title implies, money is disconnected from any underlying value.

There are plenty of points that could be added to the economics of The Big Short if it was a film of more or less unlimited length:

Krugman and friends like the film because it leaves out any discussion of the main culprit behind the financial crisis, which was not Wall Street “greed” but bad monetary and credit policies from the Federal Reserve and the federal government. The movie barely hints at any exogenous factors behind the boom or bust. (This FEE report by Peter Boettke and Steven Horwitz fills in the missing information.) So the pro-regulation crowd is cheering. Viewers are given no understanding of the real causal factors and hence fill in the missing data with a feeling that banks just love ripping people off. To be sure, if you approach this movie with some knowledge of economics and monetary policy, the rest of the narrative makes sense. Of course Wall Street got it wrong, given Washington’s policies on mortgage lending!

To add to the brew, Edward Prescott points out the Great Recession can be explained through productivity shocks. Specifically, a collapse in investment and in particular investment in intangibles such as intellectual property in 2007 in anticipation of more taxes and more regulation.

The Great Recession had many of the same features of the 1990s technology boom but in reverse. The boom in the 1990s and bust in 2007 were somewhat inexplicable because major sources of volatility were unmeasured, specifically, investment in intangible capital.

V.V. Chari also points out that the extent of the financial crisis was overstated. This is because the typical firm can finance its capital expenditures from retained earnings so it was hard to see how financial market disruptions could directly affect investment.

What Chari disputed was that bank lending to non-financial corporations and individuals has declined sharply, that interbank lending is essentially non-existent; and commercial paper issuance by non-financial corporations declined sharply, and rates have risen to unprecedented levels.

John Taylor argues that we should consider macroeconomic performance since the 1960: There was a move toward more discretionary policies in the 1960s and 1970s; A move to more rules-based policies in the 1980s and 1990s; and back again toward discretion in recent years.

These policy swings are correlated with economic performance—unemployment, inflation, economic and financial stability, the frequency and depths of recessions, the length and strength of recoveries. Less predictable, more interventionist, and more fine-tuning type macroeconomic policies have caused, deepened and prolonged the current recession. Robert Hetzel puts it this way:

The alternative explanation offered here for the intensification of the recession emphasizes propagation of the original real shocks through contractionary monetary policy. The intensification of the recession followed the pattern of recessions in the stop-go period of the late 1960s and 1970s, in which the Fed introduced cyclical inertia in the funds relative to changes in economic activity.

Finn Kydland considers fiscal policy to be at the heart of the slow recovery. Instead of restructuring and investing more prudently, Western countries faced with budget shortfalls will seek to increase taxes:

- The U.S. economy isn’t recovering from the Great Recession of 2008-2009 with the anticipated strength.

- A widespread conjecture is that this weakness can be traced to perceptions of an imminent switch to a regime of higher taxes.

- The fiscal sentiment hypothesis can account for a significant fraction of the decline in investment and labor supply in the aftermath of the Great Recession, relative to their pre-recession trends.

- The perceived higher taxes must fall almost exclusively on capital income. People must suspect that the tax structure that will be implemented to address large fiscal imbalances will be far from optimal.

Now imagine trying to incorporate all the above points into a film and keeping it at its current two-hour length?

Recent Comments