What if Apple had entered the Dow in 2008? http://t.co/xMuKHq2vRQ pic.twitter.com/6BEUeeuao2

— Bloomberg (@business) March 12, 2015

Digital market capitalisations

08 Mar 2015 Leave a comment

in financial economics Tags: amazon, Facebook, Google, market capitalisations

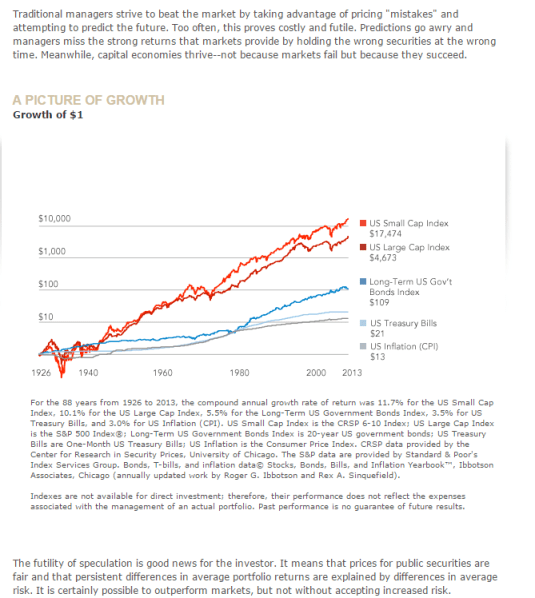

Markets have a history of rewarding investors for the capital they supply

02 Mar 2015 Leave a comment

in economic history, financial economics

HT: Markets Work.

Yet another way to beat the share market

24 Feb 2015 Leave a comment

in economics of bureaucracy, financial economics, Public Choice, rentseeking Tags: political connections, share price event studies

Over the ten trading days following the announcement of Timothy Geithner as Treasury Secretary, financial firms with a connection to Geithner experienced a cumulative abnormal return of about 12% relative to other financial sector firms. This reversed when his nomination ran into trouble due to unexpected tax issues.

That is what Daron Acemoglu, Simon Johnson, Amir Kermani, James Kwak, and Todd Mitton found recently.

Geithner had important social connections from his time as president of the Federal Reserve Bank of New York. He knew some people in finance very well – including those at large and small firms – but some others he did not know at all. This spike in share prices for connections to Tim Geithner was somewhat special as the authors explain:

when Henry (Hank) Paulson became Treasury Secretary in May 2006 – there is no evidence of a positive impact on the stock price of connected firms.

The argument put forward explaining the value of these connections had nothing to do with any suggestions of impropriety whatsoever. What happened was the value of connections spiked in a crisis such as the global financial crisis in 2008:

it was entirely reasonable for market participants to suppose that immediate action with limited oversight would have to be taken, and that officials would rely on a small network of established confidantes for advice and assistance. In fact, this is exactly what happened while Mr Geithner was at Treasury.

When the going gets tough, the tough only have time to ring friends and associates for advice and new staff.

Eugene Fama on it’s difficult, if not impossible, to distinguish luck from skill

24 Feb 2015 Leave a comment

John Bogle on the folly of share market speculation

24 Feb 2015 Leave a comment

in entrepreneurship, financial economics Tags: active investing, efficient markets hypothesis, entrepreneurial alertness, indexed linked investing, passive investing

"Paul Samuelson" on the New Zealand superannuation fund beating the market

24 Feb 2015 Leave a comment

Is the best share price forecast whatever it is today?

20 Feb 2015 Leave a comment

in financial economics Tags: efficient markets hypothesis, random walk

More correctly, for the share market, it’s a random walk with a positive drift.

What were they thinking? NZ government super fund loses the lot on loan to already failing bank in one of the PIGS.

20 Feb 2015 Leave a comment

in economics of bureaucracy, entrepreneurship, financial economics, politics - New Zealand Tags: active investing, corruption, euro crisis, Index of Economic Freedom, junk bonds, passive investing, Portugal, risk diversification, state owned enterprises

A Portuguese bank on the verge of collapse – what were they thinking?

That would have been the response of many newspaper readers this morning upon learning the New Zealand Superannuation Fund has lost nearly $200 million in taxpayers’ cash on a "risk-free" loan it provided to Lisbon-based Banco Espirito Santo (BES) on July 3.

The loan – part of a US$784 million credit package US investment bank Goldman Sachs put together through its Oak Finance vehicle – was made exactly one month before Portugal’s central bank broke up BES and split the country’s biggest lender into two, with one part holding the good assets and the toxic assets placed in the other.

Unfortunately, the Oak Finance loan is now stranded in the so-called "bad bank" following a retrospective law change by the Bank of Portugal.

Christopher Adams: What were they thinking? – Business – NZ Herald News.

This is what the 2015 index of Economic Freedom has to say about Portugal on the rule of law:

In 2013, the OECD expressed concern over Portugal’s reluctance to crack down on foreign bribery, particularly in regard to its former colonies Brazil, Angola, and Mozambique.

Since 2001, Portugal had officially acknowledged only 15 bribery allegations, and there had been no prosecutions. The judiciary is constitutionally independent, but staff shortages and inefficiency contribute to a considerable backlog of pending trials.

Actively managed share funds are on the way out

20 Feb 2015 Leave a comment

in entrepreneurship, financial economics, industrial organisation, survivor principle Tags: active investing, efficient markets hypothesis, passive investing, William F. Shape

After costs, the return on the average actively managed dollar will be less than the return on the average passively managed dollar for any time period.

—William F. Sharpe, 1990 Nobel Laureate

4 out of 5 actively managed fund portfolios underperformed all index fund portfolios in all scenarios tested.

via The tide is turning as investors switch from high-cost, actively managed funds to index funds for lower costs, higher returns » AEI | Carpe Diem Blog » AEIdeas and Mutual Fund Expenses | Lion’s Share.

.

It’s not easy to be green: the cost of fossil fuels divestments to the New Zealand superannuation fund

17 Feb 2015 Leave a comment

in economics of bureaucracy, energy economics, environmental economics, environmentalism, financial economics, global warming, Public Choice, rentseeking Tags: efficient market hypothesis, fossil fuel disinvestment, Global disinvestment day, Green Party of New Zealand, index linked investing, privatisation, state ownership

The Green Party of New Zealand wants the New Zealand superannuation fund to sell its $676 million in fossil fuel investments. For those not in the know, this government investment fund is worth about $25 billion and is funded by present taxes to pay for the universal old age pension in New Zealand. Its current investment strategy seems to rely heavily on index linked funds that minimise management and trading costs.

The Government uses the Fund to save now in order to help pay for the future cost of providing universal superannuation.

In this way the Fund helps smooth the cost of superannuation between today’s taxpayers and future generations.

In common with the endowment funds of the American universities, that $676 million is about 2% of the total New Zealand superannuation portfolio of about NZ$25 billion.

Any portfolio manager risks considerable fees if she must monitor the entire portfolio because 2% is of dubious moral stature.

The main cost of divestiture is compliance costs to prevent fossil fuel investments drifting back into the portfolio through the routine day to day investments of other companies within their portfolios as these other firms expand into new businesses or diversified. The entire portfolio must be monitored for this risk.

American universities found that fossil fuels divestment rules out indexed linked funds as a class, along with their low management and trading fees. Ethical investors must move to actively managed investment funds which are perhaps a third more expensive in management fees.

If a move to a fossil fuel free portfolio rules out passive indexed linked funds, that is a major risk to future returns of the New Zealand superannuation fund. Would this fossil fuels disinvestment including selling the recently acquired Z petrol station network by the New Zealand superannuation fund?

Z Energy now owns and manages these businesses, which include:

- a 15.4 per cent stake in Refining NZ who runs New Zealand’s only oil refinery.

- a 25 per cent stake in Loyalty New Zealand who run Fly Buys

- over 200 service stations

- about 90 truck stops

- pipelines, terminals and bulk storage

As usual, in the course of argument for disinvestment by the government investment fund, the Green Party makes an excellent argument for the privatisation not only of state owned enterprises but of the New Zealand superannuation fund.

Rather than have one victory at a time, the Greens want the NZ superannuation fund to use the funds from the disinvestment to reinvest in pet projects of politicians. The green party co-leader said:

Money released from divestment can be reinvested in the rapidly growing renewable energy and energy efficiency sectors, helping to hasten the transition of our economy to a low-carbon future.

This makes government investment funds the playthings of politicians so they can never match the returns of a genuinely privately owned investment fund.

The most successful company in the world

17 Feb 2015 Leave a comment

in economic history, economics of regulation, financial economics, health economics Tags: tobacco regulation, wages of vice

The wages of vice. It’s Altria, the cigarette company.

HT: http://www.businessinsider.com/the-most-successful-company-in-the-world-2015-2?IR=T

Recent Comments