Crony capitalism flashback – who voted against the TARP in 2008?

20 Jun 2014 Leave a comment

in financial economics, global financial crisis (GFC), great recession, macroeconomics, rentseeking Tags: crony capitalism, TARP

The US House of Representatives initially voted down the TARP in a grand coalition of right-wing republicans and left-wing democrats, voting 205–228. The right-wing republicans opposed the bailout because capitalism is a profit AND loss system. Democrats voted 140–95 in favour of the Bill while Republicans voted 133–65 against it.

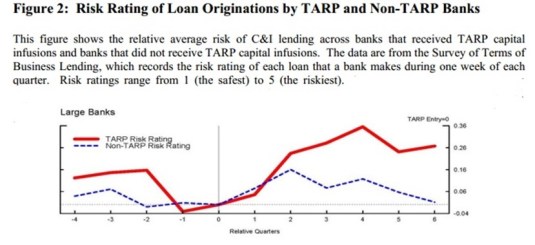

The chart above shows that the degree of risk in commercial loans made by TARP recipients appears to have increased. This is no surprise. In the 1960s, Sam Peltzman published a paper in in the 1960s showing that when deposit insurance was introduced in the USA in the 1930s, the banks halve their capital ratios. They did not need to have as much capital as before to back their lending. The chart below shows that the TARP really didn’t do much for economic policy uncertainty.

In an open letter sent to Congress, over 100 university economists described three fatal pitfalls in the TARP:

1) Its fairness. The plan is a subsidy to investors at taxpayers’ expense. Investors who took risks to earn profits must also bear the losses. The government can ensure a well-functioning financial industry without bailing out particular investors and institutions whose choices proved unwise.

2) Its ambiguity. Neither the mission of the new agency nor its oversight is clear. If taxpayers are to buy illiquid and opaque assets from troubled sellers, the terms, timing and methods of such purchases must be crystal clear ahead of time and carefully monitored afterwards.

3) Its long-term effects. If the plan is enacted, its effects will be with us for a generation. For all their recent troubles, America’s dynamic and innovative private capital markets have brought the nation unparalleled prosperity. Fundamentally weakening those markets in order to calm short-run disruptions is will short-sighted.

A recent IMF study of 42 systemic banking crises showed that in 32 cases, there was government financial intervention.

Of these 32 cases where the government recapitalised the banking system, only seven included a programme of purchase of bad assets/loans (like the one proposed by the US Treasury). These countries were Mexico, Japan, Bolivia, Czech Republic, Jamaica, Malaysia, and Paraguay.

The Government purchase of bad assets was the exception rather than the rule in banking crises and rightly so. The TARP mostly benefited bank shareholders. A case of privatising the gains and socialising the losses from banking was passed on the votes of Congressional Democrats.

To avert a financial panic, central banks should lend early and freely to solvent banks against good collateral but at penal rates

19 Jun 2014 Leave a comment

in financial economics, global financial crisis (GFC), great recession, macroeconomics, monetary economics, Thomas M. Humphrey Tags: lender of last resort, Thomas Humphrey, Walter Bagehot

First. That these loans should only be made at a very high rate of interest. This will operate as a heavy fine on unreasonable timidity, and will prevent the greatest number of applications by persons who do not require it. The rate should be raised early in the panic, so that the fine may be paid early; that no one may borrow out of idle precaution without paying well for it; that the Banking reserve may be protected as far as possible.

Secondly. That at this rate these advances should be made on all good banking securities, and as largely as the public ask for them. The reason is plain. The object is to stay alarm, and nothing therefore should be done to cause alarm. But the way to cause alarm is to refuse some one who has good security to offer… No advances indeed need be made by which the Bank will ultimately lose. The amount of bad business in commercial countries is an infinitesimally small fraction of the whole business…

The great majority, the majority to be protected, are the ‘sound’ people, the people who have good security to offer. If it is known that the Bank of England is freely advancing on what in ordinary times is reckoned a good security—on what is then commonly pledged and easily convertible—the alarm of the solvent merchants and bankers will be stayed. But if securities, really good and usually convertible, are refused by the Bank, the alarm will not abate, the other loans made will fail in obtaining their end, and the panic will become worse and worse.

Walter Bagehot Lombard Street: A Description of the Money Market (1873).

The classical theory of the lender of last resort stressed

(1) protecting the aggregate money stock, not individual institutions,

(2) letting insolvent institutions fail,

(3) accommodating sound but temporarily illiquid institutions only,

(4) charging penalty rates,

(5) requiring good collateral, and

(6) preannouncing these conditions in advance of crises so as to remove uncertainty.

Did anyone follow these rules in the global financial crisis? The Fed violated the classical model in at least seven ways:

- Emphasis on Credit (Loans) as Opposed to Money

- Taking Junk Collateral

- Charging Subsidy Rates

- Rescuing Insolvent Firms Too Big and Interconnected to Fail

- Extension of Loan Repayment Deadlines

- No Pre-announced Commitment

- No Clear Exit Strategy

…{the Fed’s} policies are hardly benign, and that extension of central bank assistance to insolvent too-big-to-fail firms at below-market rates on junk-bond collateral may, besides the uncertainty, inefficiency, and moral hazard it generates, bring losses to the Fed and the taxpayer, all without compensating benefits. Worse still, it is a probable prelude to a severe inflation and to future crises dwarfing the current one.

2014 Homer Jones Memorial Lecture – Robert E. Lucas Jr.

18 Jun 2014 Leave a comment

The first part of his lecture discusses how the Fed can influence inflation and financial stability.

Central banks can control inflation. Can central banks maintain economic stability’s financial stability? This is still an open question as to whether central banks can do that. The quantity theory of money makes certain sharp predictions about monetary neutrality which are well borne out by the cross country evidence.

In the second part of this lecture, Lucas discusses how central banks around the world have used inflation targeting to keep inflation under control.

What is the Fed to do with the stable relationship between money and prices? Inflation targeting is superior to a fixed growth monetary supply growth rule. This always pushes policy in the direction of the inflation rate you want. Central banks around the world have succeeded in keeping inflation low by explicitly or implicitly targeting the inflation rate.

In the last part of his lecture, Lucas discusses financial crises. he agrees with Gary Gordon’s analysis that 2008 financial crisis was a run on Repo. A run on liquid assets accepted as money because they can be so quickly changed into money. The effective money supply shrank drastically when there was a run on these liquid assets.

Lucas favoured the Diamond and Dybvig of bank runs as panics. The logic of that model applies to the Repo markets now was well as to the banking system. How to extend Glass–Steagall Act type regulation of bank portfolios to the Repo market is a question for future research.

Inflation targeting is working well but the lender of last resort function is yet to be fully understood.

Note: The Diamond-Dybvig view is that bank runs are inherent to the liquidity transformation carried out by banks. A bank transforms illiquid assets into liquid liabilities, subject to withdrawal.

Because of this maturity mismatch, if depositors suspect that others will run on the bank, it is optimal for each depositor to run to the bank to withdraw his or her deposit before the assets are exhausted. The bank run is not driven by some decline in the fundamentals of the bank. Depositors are spooked for some reason, panic, and attempt to withdraw their funds before others get in first. In this case, the provision of deposit insurance and lender of last resort facilities reassures depositors and stems the bank run

In the Kareken and Wallace model of bank runs, deposit insurance is problematic because of the incentives it gives to deposit taking institutions that are insured to take much greater risks. When there is deposit insurance, depositors don’t care about the greater risk in the portfolios of their banks. The greater risk taking leads to higher returns at no extra cost because if these risky investments do fail, the deposit insurance covers their losses

It is therefore necessary to regulate the portfolio of insured banks to ensure that they do not do this. That is the great dilemma for banking regulation because quasi-banks and other liquidity transformation intermediaries such as a Repo market spring up just outside the regulatory net.

Employment losses after financial crises

11 Jun 2014 Leave a comment

in Euro crisis, global financial crisis (GFC), great recession, macroeconomics Tags: financial crise will s, The shape of recovery

Policy Consistency and the Growth of Nations Finn Kydland

20 Apr 2014 Leave a comment

in development economics, global financial crisis (GFC), growth miracles, macroeconomics

Uncertainty and Ambiguity in American Fiscal and Monetary Policies – Tom Sargent

16 Apr 2014 Leave a comment

in applied welfare economics, global financial crisis (GFC), great recession, macroeconomics

Macroeconomic forecasting has had a turbulent history

16 Apr 2014 Leave a comment

in global financial crisis (GFC), great recession, macroeconomics, Milton Friedman Tags: data mining, Edward Leamer, forecasting, lags on monetary policy

Most early discussions argued against econometric forecasting in principle:

- Forecasting was not properly grounded in statistical theory,

- It presupposed that causation implies predictability, and

- The forecasts themselves were invalidated by the reactions of economic agents to them.

A long tradition argued that social relationships were too complex, too multifarious and too infected with capricious human choices to generate enduring, stable relationships that could be estimated.

These objections came before Hayek’s point that much of all social knowledge is not capable of summation in statistics or even language.

The limitations of forecasting are well-known. Forecasts are conditional on a number of variables; there are important unresolved analytical differences about the operation of the economy; and large uncertainties about the size and timing of responses to macroeconomic changes. Shocks to the output, prices, employment and other variables are partly permanent and partly transitory.

At the practical level, forecasting requires that there are regularities on which to base models, such regularities are informative about the future and these regularities are encapsulated in the selected forecasting model.

We have very little reliable information about the distribution of shocks or about how the distributions change over time. Forecast errors arise from changes in the parameters in the model, mis-specification of the model, estimation uncertainty, mis-measurement of the initial conditions and error accumulation.

In the 1980s, data mining and publications bias were so strong and statistical inferences were so fragile that Ed Leamer’s 1983 Let’s Take the Con out of Econometrics paper made up-and-coming applied economists despair for their professional field and for their own careers:

The econometric art as it is practiced at the computer terminal involves fitting many, perhaps thousands, of statistical models. One or several that the researcher finds pleasing are selected for reporting purposes.

This search for a model is often well intentioned, but there can be no doubt that such a specification search invalidates the traditional theories of inference….

[A]ll the concepts of traditional theory…utterly lose their meaning by the time an applied researcher pulls from the bramble of computer output the one thorn of a model he likes best, the one he chooses to portray as a rose.

… This is a sad and decidedly unscientific state of affairs we find ourselves in.

Hardly anyone takes data analyses seriously.

Or perhaps more accurately, hardly anyone takes anyone else’s data analyses seriously.

Like elaborately plumed birds who have long since lost the ability to procreate but not the desire, we preen and strut and display our t-values [which measure statistical significance].

Leamer still doubts the progress towards techniques that separate sturdy from fragile inferences. Economists by and large simply do not want to hear that they cannot make major conclusions from the data sets. But not that they really do, but that is for a forthcoming post.

Before the great moderation spread wide, Brunner and Meltzer found that in the 1970s and 1980s, the 95% confidence intervals on next year’s forecasts for Gross Domestic Product and the Consumer Price Index are such that government and private forecasters in the USA and Europe could not distinguish between a recession and a boom, nor say whether inflation will be zero or ten per cent.

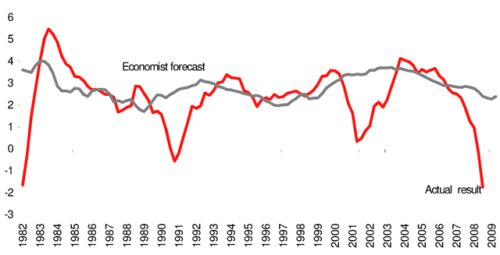

A review this week by Ahir and Lounganishows found that recent forecasting by the private and public sector has not improved:

none of the 62 recessions in 2008–09 was predicted as the previous year was drawing to a close.

Figure 1. Number of recessions predicted by September of the previous year

Source: Ahir and Loungani 2014, “There will be growth in the spring”: How well do economists predict turning points?” http://www.voxeu.org/

A policy-maker who adjusts policy based on forecasts for the following year has little reason to be confident that he has changed policy in the right direction.

While at graduate school, I wrote what was published as Official Economic Forecasting Errors in Australia 1983-96.

Australian Treasury forecasting errors were so large relative to the mean annual rate of change in real GDP and the inflation rate that, on average, forecasters could not distinguish slow growth from a deep recession or stable prices from moderate inflation.

The biography of Paul Keating by Edwards suggested that the Government of the day was well aware of the poor value of forecasts. So much so that forecasts may not have actually played a significant role in monetary policy making in Australia in the late 1980s onwards. John Stone said this to Keating when he assumed office as Treasurer in 1983:

As you know, we (and I in particular) have never had much faith in forecasting.

Not infrequently, our forecasts turn out to be seriously wrong.

… We simply do the best we can, in as professional manner as we can — and, if it is any consolation, no one seems to be able to do any better, at least in the long haul.

We always emphasize the uncertainties that attach to the forecasts — but we cannot ensure that such qualifications are heeded and plainly they often are not

To cast my results in Milton Friedman’s nomenclature for monetary lags, the recognition lag on a forecasting based monetary policy appears to be infinite because forecasters do not know if there will be a recession or 10% inflation afoot when their monetary policy changes take hold in 18 to 24 months.

Was the global economic crisis unforeseen?

15 Apr 2014 Leave a comment

in global financial crisis (GFC), great recession Tags: Kareken and Wallace model of deposit insurance, Ross Levine, Too big to fail

Plenty of people warned of dark days ahead. An essay anyone can read with profit is Ross Levine’s "An Autopsy of the U.S. Financial System: Accident, Suicide, or Negligent Homicide?"

The paper studies five important policies:

- Securities and Exchange Commission (SEC) policies toward credit rating agencies,

- Federal Reserve policies concerning bank capital and credit default swaps,

- SEC and Federal Reserve policies about over-the-counter derivatives,

- SEC policies toward the consolidated supervision of major investment banks, and government policies toward Fannie Mae and Freddie Mac.

Levine concludes that

- The evidence is inconsistent with the view that the collapse of the financial system was caused only by the popping of the housing bubble ("accident") and the herding behaviour of financiers rushing to create and market increasingly complex and questionable financial products ("suicide").

- Rather, the evidence indicates that senior policymakers repeatedly designed, implemented, and maintained policies that destabilized the global financial system in the decade before the crisis.

- Moreover, although the major regulatory agencies were aware of the growing fragility of the financial system due to their policies, they chose not to modify those policies, suggesting that "negligent homicide" contributed to the financial system’s collapse

- Although influential policymakers presumed that international capital flows, euphoric traders, and insufficient regulatory power caused the crisis, the paper shows that these factors played only a partial role.

- Current reforms represent only a partial and incomplete step in establishing a stable and well-functioning financial system.

- Since systemic institutional failures helped cause the crisis, systemic institutional reforms must be a part of a comprehensively effective response.

The most interesting morsels are:

- The New York Times warned in 1999 that Fannie Mae was taking on so much risk that an economic downturn could trigger a “rescue similar to that of the savings and loan industry in the 1980s,” and again emphasized this point in 2003; and

- Alan Greenspan testified before the Senate Banking Committee in 2004 that the increasingly large and risky GSE portfolios could have enormously adverse ramifications! A rare occasion on which Greenspan did not talk in riddles.

Stern and Feldman’s Too Big to Fail in 2004 used insights gleaned from the formal economic literature to frame warnings in 2004 about the time bomb for a financial crisis set by current regulations and government promises.

The prediction of the Kareken and Wallace moral hazard model of deposit insurance is if a government sets up deposit insurance and doesn’t regulate bank portfolios to prevent them from taking too much risk, the government is setting the stage for a financial crisis. If financial intermediaries do not bear the full consequences of their actions (because they are insured) then profit maximising portfolios will be too risky. The Kareken-Wallace model makes you very cautious about lender-of-last-resort facilities and very sensitive to the risk-taking activities of banks.

Tom Sargent said that Jose Scheinkman made a list of the ten academic papers that the Reagan administration should have looked at. Number one on his list was Kareken and Wallace.

The idea that deposit insurance leads to more financial crises even troubled FDR before he signed the 1934 U.S. bill to introduce deposit insurance.

Why do recessions cheer the Left up?

05 Apr 2014 Leave a comment

in global financial crisis (GFC), great recession, politics

Why is it that the further to the Left that people go, the more cheerful they seem to be in recessions and economic crises? They are miserable when times are good.

The Left supported the discretionary fiscal, monetary and regulatory policies that caused the recession and then supported crisis management policies that deepen the recession. The Left always wants to tax and regulate their way out of every recession.

Most crisis management policies distort the incentives to hire and invest and reduce competition and efficiency. While different sorts of shocks lead to ordinary downturns, it is overreactions by governments to stem the crisis that prolong and deepen economic downturns, turning them into depressions.

One in three EU unemployed are Spanish because of employment protection laws. Cahuc et al. 2012 estimated that Spanish unemployment would be 45% lower if Spain adopted the less strict French laws! Differences in their employment protection laws accounted for nearly half of the dramatic rise in Spanish unemployment since 2007. Who is for and against these terrible laws?

Lee Ohanian: Hoover, Roosevelt and the Great Depression

03 Apr 2014 Leave a comment

in global financial crisis (GFC), great depression, regulation

Lee Ohanian: The Economic Crisis: A Comparison Across Time and Countries

01 Apr 2014 Leave a comment

in global financial crisis (GFC), great recession, labour economics

“The Recession of 2007–?” by Robert E. Lucas

31 Mar 2014 1 Comment

in global financial crisis (GFC), great recession

Robert Lucas in this speech noted that the implicit assumption is that the US economy will get back to old trend growth rate and the only question is how long it will take

Lucas asked whether this is really the case? He noted that:

- We know that European economies have larger government role and 20-30% lower income level than the US; and

- Is it possible that by imitating European policies on labor markets, welfare, and taxes U.S. has chosen a new, lower GDP trend?

If so, Lucas said that it may be that the weak recovery the USA has had so far is all the recovery it will get.

Ed Prescott also considers that tax rates are being increased in the USA. These increases lower amount of capital a firm chooses to have. The reason for low investment is not problem of getting loans – it is expected future high tax rates in the USA.

Ed Prescott also considers that investment suddenly became depressed beginning early in 2008 – because of a policy regime change. Business owners feared higher tax rates with the regime change and rationally cut investment, rationally cut employment ad rationally took more cash out of business.

How to Restore US Prosperity – Prof. Edward C. Prescott

29 Mar 2014 Leave a comment

in global financial crisis (GFC), great recession, labour economics, regulation

Euro Crisis: Sources and Its Global Implications – Tom Sargent updated

28 Mar 2014 Leave a comment

in Euro crisis, global financial crisis (GFC), great recession Tags: Tom Sargent

Sargent said: “A government can be said to be ambiguous when decision makers can’t yet agree what to do and decide to postpone making a decision.” He also raised questions over whether a country should join a currency union, whether it should pay its debts, and whether the central government in a federal system should pay the debts of subordinate government.

Recent Comments