Does inflation stimulate the economy? | Robert E. Lucas

19 Oct 2016 Leave a comment

in fiscal policy, macroeconomics, monetary economics, Robert E. Lucas Tags: fiscal stimulus

Milton Friedman – Congressional House Economic Task Force (1993)

15 Oct 2016 Leave a comment

in economic history, fiscal policy, great depression, history of economic thought, macroeconomics, Milton Friedman, monetarism, monetary economics Tags: fiscal stimulus

Milton Friedman is said to have mesmerised several countries with a flying visit!?

30 Sep 2016 Leave a comment

in business cycles, economic growth, macroeconomics, Milton Friedman, monetarism, monetary economics, politics - Australia Tags: central banks, conspiracy theories, lags on monetary policy, monetary policy, rules versus discretion, The fatal conceit, The pretense to knowledge

Milton Friedman visited Australia in 1975. He spoke with government officials and appeared on the TV show Monday Conference. Apparently, that was enough for him to take over Australian monetary policy setting for the foreseeable future.

When working at the next desk to the monetary policy section in the late 1980s, I heard not a word of Friedman’s Svengali influence:

- The market determined interest rates, not the reserve bank was the mantra for several years. Joan Robinson would be proud that her 1975 visit was still holding the reins.

- Monetary policy was targeting the current account. Read Edwards’ bio of Keating and his extracts from very Keynesian treasury briefings to Keating signed by David Morgan that reminded me of macro101.

See Ed Nelson’s (2005) Monetary Policy Neglect and the Great Inflation in Canada, Australia, and New Zealand who used contemporary news reports from 1970 to the early 1990s to uncover what was and was not ruling monetary policy. For example:

“As late as 1990, the governor of the Reserve Bank rejected central-bank inflation targeting as infeasible in Australia, and cited the need for other tools such as wages policy (AFR, October 18, 1990).”

Bernie Fraser was still sufficiently deprogrammed in 1993 to say that “…I am rather wary of inflation targets.” Easy to then announce one in the same speech when inflation was already 2-3%.

When as a commentator on a Treasury seminar paper in 1986, Peter Boxhall – fresh from the US and 1970s Chicago educated – suggested using monetary policy to reduce the inflation rate quickly to zero, David Morgan and Chris Higgins almost fell off their chairs. They had never heard of such radical ideas.

In their breathless protestations, neither were sufficiently in-tune with their Keynesian educations to remember the role of sticky wages or even the need for the monetary growth reductions to be gradual and, more importantly, credible as per Milton Freidman and as per Tom Sargent’s End of 4 big and two moderate inflations papers.

I was far too junior to point to this gap in their analytical memories about the role of sticky wages, and I was having far too much fun watching the intellectual cream of the Treasury senior management in full flight. At a much later meeting, another high flying deputy secretary was mystified as to why 18% mortgage rates were not reining in the current account in 1989.

Friedman’s Svengali influence did not extend to brainwashing in the monetarist creed that the lags on monetary policy were long and variable. The 1988 or 1989 budget papers put the lag on monetary policy at 1 year, which is short and rapier, if you ask me.

When did Canberra policy makers accept that inflation was a monetary phenomenon?

27 Sep 2016 3 Comments

in business cycles, economic history, macroeconomics, monetarism, monetary economics, politics - Australia Tags: central banks, monetary policy, The Great Inflation

Australian policymakers from at least 1971 viewed inflation as not a consequence of their monetary policy decisions. There were repeated references by them to wage-price spirals and both unsuccessful (1977) and successful attempts (1981) at wage freezes.

The prices and incomes accord from 1983 onwards was just another 1970s wage tax trade-off. An Incomes policy attributes inflation to non-monetary factors, as did Fraser and Lynch regularly.

• It was not until 1980 that the Fraser government’s monetary policy became genuinely anti-inflationary. With a lag, these changes halved inflation to the mid-single digits by 1983. The implementation lag on the 1975 Monday conference programme must have been long and variable and lasted for a three year window!? Three years out of 20 is hardly a monetarist hegemony!

• Australia had lower CPI inflation in the 1980s than the 1970s, but this was marred by rebounds in 1985–86 and 1988–90 to near 9%.

The monetary policy regime change in the late 1980s was triggered by factors besides rising inflation: a demonic view of currant account.

After several years of high interest rates, the budget papers forecasted a moderate slowing:

• The budget GDP forecast for 1990-91 was 2% with an actual of minus 0.4%; for inflation the actual and forecast were 5.3% versus 6.5%; 1989-90 inflation rate was 8% with GDP growth of 3.3%.

• In 1991-92, the budget GDP forecast was 1.5% with an actual of 2.1%; for inflation the actual and forecast were 1.9% versus 3.8%.

• In 1992-93, the budget papers forecast for inflation 3% for an actual of 1%.

• In 1993-94, the budget forecast for inflation 3.5% for an actual of 1.8%.

The monetarists in the Treasury, entranced as they were by Friedman’s 1975 visit, still had not clicked to the link between a tight monetary policy and low inflation as late as 1993. Australia pursued a stop-go monetary policy from 1971 to the early 1990s.

I worked in the next desk to the monetary policy section in the Prime Minister’s Department in the 1980s. They were determined that market set interest rates, not monetary policy.

I suggest you read the biography of keating by john edwards(?) – his economic advisor in the late 1980s.

Edwards quotes from numerous Treasury briefings to Keating. the Treasury remembered their Keynesian educations well, as did those at DPMC. the prices and incomes accord was very Keynesian: inflation as a non-monetary phenomenon

Mentioning Friedman’s name in the 1980s at job interviews would have been extremely career limiting. Not much better in the early 1990s. Back in the late 1980s, Friedman was graduating from ‘a wild man in the wings’ to just a suspicious character in policy circles.

If you name dropped Hayek in the 1980s and 1990s, any sign of name recognition would have indicated that you were been interviewed by people who were very widely read.

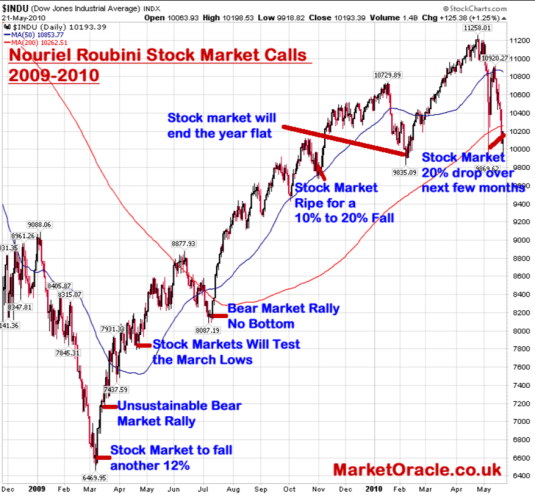

Did @AnnPettifor correctly predict the global financial crisis in 2003?

21 Sep 2016 1 Comment

in economic history, global financial crisis (GFC), macroeconomics, monetary economics

You are not much of a leftover Marxist if you are not predicting a crisis in capitalism is on the horizon.

https://twitter.com/PolicyObsAUT/status/778456702655995904

Capitalism is supposed to collapse under its own inner contradictions.

Professional stock market tipsters are notorious from specialising in predicting doom as well and they still get listened too despite terrible forecasting records.

Plenty of people warned of dark days ahead in the lead up to the global financial crisis. An essay anyone can read with profit is Ross Levine’s An Autopsy of the U.S. Financial System: Accident, Suicide, or Negligent Homicide? His abstract says

The evidence is inconsistent with the view that the collapse of the financial system was caused only by the popping of the housing bubble (“accident”) and the herding behavior of financiers rushing to create and market increasingly complex and questionable financial products (“suicide”).

Rather, the evidence indicates that senior policymakers repeatedly designed, implemented, and maintained policies that destabilized the global financial system in the decade before the crisis. Moreover, although the major regulatory agencies were aware of the growing fragility of the financial system due to their policies, they chose not to modify those policies, suggesting that “negligent homicide” contributed to the financial system’s collapse.

The New York Times warned in 1999 that Fannie Mae was taking on so much risk that an economic downturn could trigger a “rescue similar to that of the savings and loan industry in the 1980s,” and emphasised this point again in 2003. Greenspan testified before a Senate committee in 2004 that the increasingly large and risky Fannie Mae and Freddie Mac portfolios could have enormously adverse ramifications.

You predict a financial crisis by pointing to adjustments in your share portfolio to take advantage of shorting the market and then showing how big a profit you made afterwards.

The movie The Big Short highlights that its protagonists had skin in the game. They were investing in mortgages or shorting the same in the expectation of the crash they were predicting. Much of the drama in the film is about how long their foretelling of a crash took to come true.

There were no windbags and armchair critics in The Big Short talking gloom and doom on the horizon without investing their own money to profit from their forecasts.

Shawshank Redemption — Money in Prison

15 Sep 2016 Leave a comment

in applied price theory, monetary economics Tags: Shawshank Redemption

NZ inflation rate since 1991 with 1% CPI bias adjustment

13 Sep 2016 Leave a comment

in economic history, inflation targeting, macroeconomics, monetary economics, politics - New Zealand Tags: CPI bias, inflation rate

The inflation rate is overstated by about 1% each year because of difficulties in measuring new goods entering the consumer price index and improvements in the quality of existing goods in the consumer price index. With that adjustment of 1% in the chart below, a common measure of that bias, New Zealand has had zero to negative inflation for four years

Source: Reserve Bank of New Zealand Key Statistics.

One of the reasons for an inflation target band of 1 to 3% is an inflation rate of 1% is actually an inflation rate of 0%.

Four Reasons Financial Intermediaries Fail

28 Jul 2016 Leave a comment

in applied price theory, business cycles, macroeconomics, monetary economics Tags: bank panics, banks runs

Hayek on Milton Friedman and Monetary Policy

25 Jun 2016 Leave a comment

in business cycles, economics, F.A. Hayek, macroeconomics, Milton Friedman, monetarism, monetary economics

@NZGreens @jamespeshaw forgot how much NZ’s deposit insurance recently cost taxpayers

22 Jun 2016 Leave a comment

in applied price theory, monetary economics, politics - New Zealand

The Greens co-leader James Shaw has today called for New Zealand to re-introduce deposit insurance saying that

“It would be a small levy placed on the banks, which would go into an insurance fund. It’s been operating successfully in many, many other countries.” But Mr Shaw said the Government and Reserve Bank keep putting off the change, saying customers can choose the bank they believe is most stable. “Consumers are not well educated about the stability of banks, so what that means is they tend to flow to the really big Australian-owned banks.”

Deposit insurance has a long history of promoting banking instability and irresponsible lending. It has not operated successfully in other countries nor in New Zealand. The Green Party announcement made no mention of New Zealand’s recent experience with deposit insurance

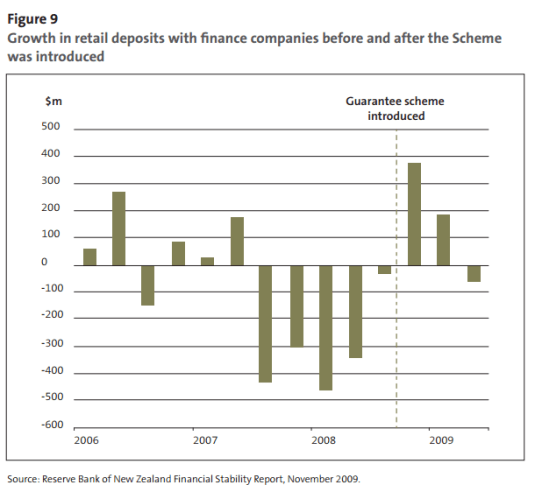

At the height of the global financial crisis and in the final days of the 2008 general election, New Zealand not only extended a deposit guarantee to its banks it also did so to finance companies. As the Auditor-General recorded in her recent report

On Sunday 12 October 2008, at the peak of the global financial crisis, the Government decided that it needed to implement a form of retail deposit guarantee scheme to avoid a flight of funds from New Zealand institutions to those in Australia. It needed to do this urgently: The Crown Retail Deposit Guarantee Scheme (the Scheme) was designed and announced that same day.

The deposit guarantee was extended to finance companies. Money flooded into previously high risk investments as investors had nothing to lose and everything to gain from the higher returns.

As the Auditor-General noted in a 2015 recent report reviewing the scheme

From the outset, the advice from officials recognised that the decision to include finance companies in the Scheme carried significant risk. Once deposits with these companies were guaranteed, depositors could safely move investments to where they would get the highest return, irrespective of the risk of company failure.

The finance companies also had less reason to minimise risk in their investment activity. The Crown was carrying much of this risk. During 2009, the Treasury watched some of that behaviour eventuate. Deposits with finance companies under the Scheme grew, in some instances significantly. We saw one example where a finance company’s deposits grew from $800,000 to $8.3 million after its deposits were guaranteed. At South Canterbury Finance Limited, the deposits grew by 25% after the guarantee was put in place.

The flood of deposits into finance company after the deposit guarantee somewhat undermines the low opinion the Greens have of depositors as investors sensitive to risk

On blunting incentives, otherwise known as ‘moral hazard’, Bill English can’t seriously expect everyday savers to analyse the loan books of banks to assess their credit risk when they open their accounts, let alone do this on a six-monthly basis.

At its height, the bank and finance company guarantees totalled over $133 billion. Ninety-six institutions were covered by the scheme – 60 non-bank deposit takers, 12 banks and 24 collective investment schemes. All guarantees had ended by December 2011.

To put context on the risk that the taxpayer, this $133 billion underwritten by the taxpayer return for little or no insurance fee was nearly twice the amount the Government spends in a year, or about 2/3rd of GDP.

If a financial institution in the Scheme failed, taxpayers would repay all of the money that eligible people had deposited or invested, up to a cap of $1 million each.

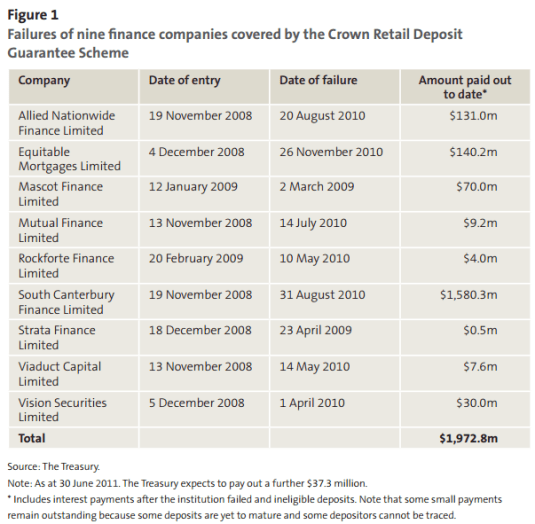

Nine finance companies out of the 30 accepted into the scheme failed. This resulted in payments by the taxpayer to the investors of $2 billion. Expected recoveries are currently estimated at about $0.9 billion after the completion of the various receiverships of these institutions according to the recent report on the scheme by the Auditor-General.

The deposit guarantee was extended to the finance companies despite 28 such companies failing between 2006 and 2008. This included some larger finance companies such as Bridgecorp Finance (New Zealand) Limited, Provincial Finance Limited, and Hanover Finance Limited.

FDR was initially opposed to deposit insurance in the USA in 1933 because it would encourage greater risk taking by banks. Sam Peltzman in the mid-1960s found that U.S. banks in the 1930s halved their capital ratios after the introduction of federal deposit insurance.

If you want to make banks safer, increase their capital ratios and require them to have more subordinated debt in their capital requirements.

Any form of deposit insurance requires extensive regulation of insured bank portfolios to prevent excessive risk-taking. The Kareken and Wallace model of deposit insurance which is based on moral hazard, predicts that if a government sets up deposit insurance and doesn’t regulate bank portfolios to prevent them from taking too much risk, the government is setting the stage for a financial crisis. The Kareken-Wallace model makes you very cautious about lender-of-last-resort facilities and very sensitive to the risk-taking activities of banks.

Kareken and Wallace called for much higher capital reserves for banks and more regulation to avoid future crises. It is much easier to require banks to put up more capital than to not take risks with the monies invested in them by depositors.

Recent Comments