Churchill on capitalism

14 Sep 2014 Leave a comment

in applied welfare economics, constitutional political economy, market efficiency, Public Choice, public economics, technological progress Tags: capitalism, Winston Churchill

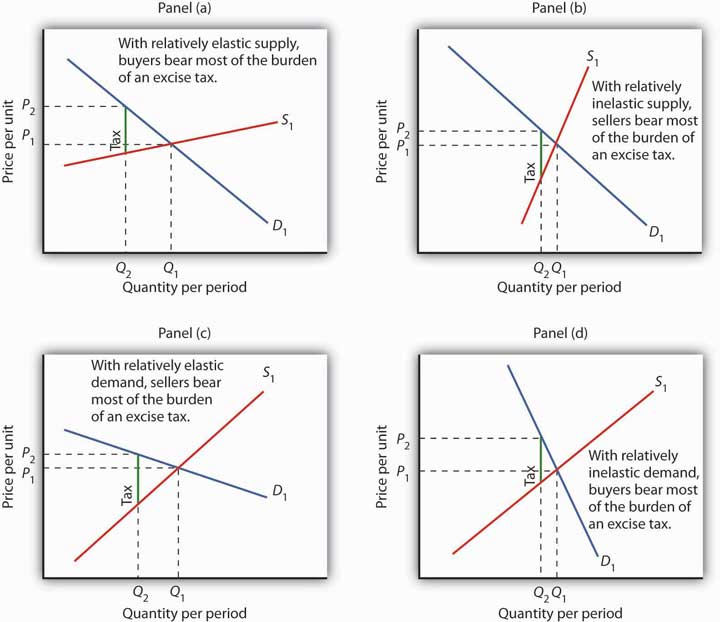

The most forgotten diagrams in the political economy of taxation-updated

30 Jul 2014 Leave a comment

in applied price theory, public economics, taxation Tags: incidence of taxes, the burden of taxes

The ability to pass the burden of the tax depends on price elasticity of demand and price elasticity of supply.

The state has no sources of money other than the money people earn themselves

28 Jul 2014 Leave a comment

in liberalism, public economics Tags: Margaret Thatcher

Have you ever heard of a private firm proposing to solve a shortage of the product it sells by telling people to buy less?

27 Jun 2014 Leave a comment

Tax Freedom Day

04 Jun 2014 Leave a comment

in public economics, taxation Tags: taxes

HT: Daniel Mitchell

Is Thomas Piketty a double secret supply-side economist?

03 Jun 2014 Leave a comment

in entrepreneurship, labour supply, public economics Tags: laffer curve, supply-side economics, Thomas Peketty

When a government taxes a certain level of income or inheritance at a rate of 70 or 80 percent, the primary goal is obviously not to raise additional revenue (because these very high brackets never yield much).

It is rather to put an end to such incomes and large estates, which lawmakers have for one reason or another come to regard as socially unacceptable and economically unproductive…

Recent Comments