Today the Treasury advised that it no longer calculates an annual rate of return on the portfolio of state owned enterprises as a whole. It no longer publishes an annual portfolio report (APR).

Source: Treasury response to Official Information Act request by Jim Rose, 14 January 2016.

The Treasury regards the crown portfolio report which contains performance indicators on the state owned enterprises portfolio as a whole as too resource intensive.

The Treasury prefers to be more forward-looking in their reporting on a quarterly basis to the Minister of Finance. Unfortunately, the Treasury refused to my requests for access to this forward-looking reporting to the Minister of Finance on commercial-in-confidence grounds.

The forward-looking approach to state-owned enterprise performance is now only by the Treasury and the Minister of Finance. No one else has access to this financial performance information.

It is no longer possible to say using a figure calculated by the Treasury whether the portfolio of state owned enterprises as a whole are a good return to the taxpayer or not. Individual annual reports of the state owned enterprises can be reviewed but the portfolio wide rate of return is no longer available from the Treasury with the associated credibility of the same.

A common argument against state ownership is that as a whole government ownership is a bad investment. Specifically, the portfolio of state owned enterprises struggle to pay a return in excess of the long-term bond rate.

A common argument for continued state ownership is the loss of the dividends from privatisation. The vulgar argument such as by the New Zealand Labor Party and New Zealand Greens is if a state owned enterprise is privatised either partially or fully, the taxpayers no longer receive dividends. The fact that the sale price reflects the present value of future dividends is simply ignored.

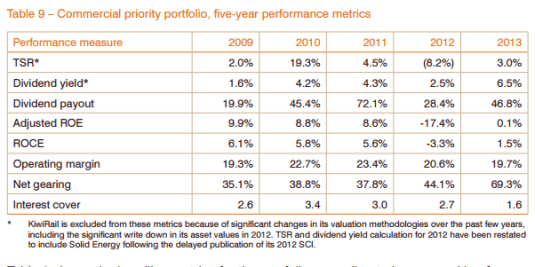

Source: Treasury, Crown Portfolio Report 2013.

The sophisticated argument is the assets are under-priced such as for political reasons. Failed privatisations are indeed the best case against state ownership because governments cannot even sell an asset with such any degree of competence.

Governments are so bad as business owners and so incapable of running a commercial process free of politics that governments cannot even sell a state-owned enterprise for a good price under the full glare of the media and public.

Source: Treasury, Crown Portfolio Report 2013.

A reply to the loss of dividends argument is the dividends from the portfolio as a whole do not repay the government debt incurred to fund capital infusions into state-owned enterprises both when initially established and through time. In that case, it is better to leave your money in the bank than in the state of enterprise.

John Quiggin often criticises privatisation on the grounds that state owned enterprises can invest at a cheaper rate because they are financed at the long-term bond rate:

In general, even after allowing for default risk, governments can borrow more cheaply than private firms. This cost saving may or may not outweigh the operational efficiency gains usually associated with private ownership.

It is not possible to scrutinise that argument without an annual rate of return on the portfolio of state owned enterprises as a whole to see if it is true at first pass at least. As the Treasury no longer calculates a rate of return on the portfolio and taxpayers’ equity, that debate comes to something of a crashing halt in New Zealand.

If these state owned enterprises were privately owned and listed on the share market, investors would just look at trends in share prices for daily measure of expected future profitability.

John Quiggin made the best simple summary of the case for privatisation which was the selling the dogs in the portfolio:

The fiscal case for privatisation must be assessed on a case by case basis. It will always be true for example that if a public enterprise is operating at a loss, and can be sold off for a positive price with no strings attached, the government’s fiscal position will benefit from privatisation.

Various early ventures in public ownership, such as the state butcher shops operated in Queensland in the 1920s (apparently a response to concerns about thumbs on scales) met this criterion, and there doesn’t seem to be much interest in repeating this experiment.

Quiggin also made a measured statement of why state ownership should be limited at most to monopolies:

In most sectors of the economy, the higher cost of equity capital is more than offset by the fact that private firms are run more efficiently, and therefore more profitably, than government enterprises.

But enterprises owned by governments are usually capital intensive and often have monopoly power that entails close external regulation, regardless of ownership. In these situations, the scope to increase profitability is limited, and the lower value of the asset to a private owner is reflected in the higher rate of return demanded by equity investors.

Quiggin is wrong about government enterprises have been a lower cost of capital because it contradicts the most fundamental principles of business finance as explained by Sinclair Davidson:

…it is clear that the Grant-Quiggin view violates the Modigliani-Miller theories of corporate finance. The cost of capital is a function of the riskiness of the investment projects and not a function of a firm’s ownership structure.

How the cash flows of a business are divided between owners and creditors does not matter unless that division changes the incentives they have to monitor the performance of the firm and keep it on its toes. Those lower down the pecking order if things go wrong such as owners have much more of an incentive to monitor the success of the business and lift its performance.

Capital structures of firms, the property rights structures of firms, matter precisely because they influence incentives of those with different claims on the cash flows of the firm.

Having to pay debt disciplines managerial slack and ensures that free-cash flows are used to repay debt (or pay dividends) rather than be invested in low quality new ventures. Having to borrow from strangers such as banks ensures regular scrutiny of the soundness and prospects of the company from a fresh set of eyes. Capital structures made up of both debt and equity keeps the firm on its toes.

Unfortunately, in New Zealand it is much more difficult to review the arguments for and against the current size and shape of the state owned enterprise portfolio as for example summarised by John Quiggin:

Technologies and social priorities change over time, with the result that activities suitable for public ownership at one time may be candidates for privatization in another. However, the reverse is equally true. Problems in financial markets or the emergence of new technologies may call for government intervention in activities previously undertaken by private enterprise.

In summary, privatization is valid and important as a policy tool for managing public sector assets effectively, but must be matched by a willingness to undertake new public investment where it is necessary.

As a policy program, the idea of large-scale privatization has had some important successes, but has reached its limits in many cases. Selling income-generating assets is rarely helpful as a way of reducing net debt. The central focus should always be on achieving the right balance between the public and private sectors.

This balancing of public and private ownership is more difficult in New Zealand because portfolio wide rates of return are unavailable unless you calculate them yourself. That must be labour-intensive given the Treasury thought it was too labour-intensive for it to do for itself.

An obvious motive to start a review the extent of state ownership is the portfolio is performing poorly. That warning sign is no longer available because the crown portfolio report is no longer published.

One way to fix an underperforming portfolio is to sell the dogs in the portfolio. One of the first ways owners notice dogs in their portfolio is the portfolio not returning as well as it used too because of the emergence of these dogs so further enquiries are made and explanations sought.

Taxpayers, ministers and parliamentarians are all busy people with little personal stake in the rate of return on the state owned enterprises portfolio.

Taxpayers, ministers and parliamentarians will all first look at the portfolio wide rate of return to see whether more detailed scrutiny of individual investments is required. That quick check against poor value for money and trouble ahead is no longer available on the state owned enterprises portfolio in New Zealand.

Recent Comments