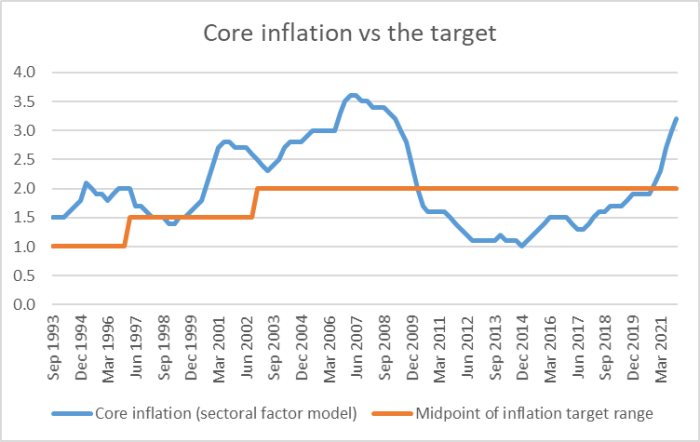

The CPI for the December quarter was finally released yesterday – even later in the month than that other CPI laggard the ABS. The picture wasn’t pretty, even if at this point not particularly surprising. My focus is on the sectoral factor model measure of core inflation – long the Reserve Bank’s favourite – and if, as my resident economics student says “but Dad, no one else seem to mention it”, well too bad. Of the range of indicators on offer it is the most useful if one is thinking about monetary policy, past and present.

Factor models like this provide imprecise reads (subject to revision) for the most recent periods – that’s what you’d expect, especially when things are moving a lot, as the model is looking to identify something like the underlying trend. The most recent observations were revised up yesterday, and the estimate for core inflation for…

View original post 2,252 more words

Recent Comments