Austrian macroeconomics vs. Keynesian macroeconomics in One Chart : The Circle Bastiat

23 Sep 2014 Leave a comment

Barriers to entry alert: do late entrants have a chance

22 Sep 2014 Leave a comment

in applied price theory, Austrian economics, economic history, entrepreneurship, industrial organisation, liberalism, technological progress Tags: Austrian economics, barriers to entry, creative destruction, Israel Kirzner, market process

September 21, 1999 – Google came out of beta; the 17th search engine to officially enter the market.

Kirzner defines a competitive market as a market where no potential participant faces non-market obstacles to entry:

Following a long tradition in economics going back at least to Adam Smith, Austrians define a competitive market not as a situation where no participant or potential participant has the power to make any difference, but as a market where no potential participant faces nonmarket obstacles to entry.

(The adjective “nonmarket” refers, primarily, to government obstacles to entry; it is used to differentiate such obstacles from, for example, high production costs that might discourage entry. These latter do not constitute noncompetitive elements in a market; to be able to enter means to be able to enter a market if one judges such entry to be economically promising-it does not mean to be able to enter without having to bear the relevant costs of production.) That is, a situation is competitive if no incumbent participant possesses privileges that protect him against the possible entry of new competitors.

The achievements that free markets are able to attain depend, in the Austrian view, on freedom of entry, that is, on the absence of privilege.

Market inefficiency is revealed through a process of entrepreneurial discovery

13 Sep 2014 Leave a comment

Preferences are demonstrated through choices – nothing more and nothing less

04 Sep 2014 Leave a comment

Hayek Explains Why He Did Not Challenge Keynes’ General Theory

03 Sep 2014 Leave a comment

in Austrian economics, business cycles, F.A. Hayek, fiscal policy, great depression, macroeconomics Tags: FA Hayek, General Theory, Keynes

Time I want back on my deathbed: listening to social credit and other monetary cranks

02 Sep 2014 1 Comment

in Austrian economics, business cycles, economic growth, inflation targeting, monetarism, monetary economics, Murray Rothbard Tags: Austrian school of economics, business cycle, fractional reserve banking, hyperinflation, inflation, monetary business cycle, monetary cranks, quantity theory of money

I lost a good 15 minutes of my life that I will not get back on my deathbed listening to some monetary cranks at a Meet the Candidates forum last night for the New Zealand general election.

Monetary cranks advocate boundless inflation and credit expansion as the patent medicine for all our economic ills:

those who have Found the Light about Money take up their pens and write, with a conviction, a persistence and a devotion otherwise only found among the disciples of a new religion.

It is easy to scoff at these productions: it is not so easy always to see exactly where they go wrong. It is natural that practical bankers, vaguely conscious that the projects of monetary cranks are dangerous to society, should cling in self-defence to the solid rock, or what they believe to be so, of tradition and accepted practice. But it is not open to the detached student of economics to take refuge from dangerous innovation in blind conservatism.

D.H. Robertson (1928)

Listening to these monetary cranks in the audience last night rates with the worst movies I have ever ever seen for time I want back my deathbed. I think the worst movie I have ever seen was Absolute Beginners starring David Bowie. After that it, might be Last Tango in Paris.

These particular monetary cranks with their obsessions about factional reserve banking are from the social credit party in New Zealand. They are followers of Major C.H. Douglas, whom Keynes referred to as a:

private, perhaps, but not a major in the brave army of heretics

Social credit and other monetary cranks believe that all the world’s problems will be sold if the reserve bank prints money and they seem to think that was really easy because there is a fractional reserve banking system.

No one in the room who knew better wanted to lose more time that they wanted back on their deathbed explaining why printing money doesn’t make you richer. The “money is wealth” error is the defining affliction of the monetary crank.

The good economist will know that money creation is no short-cut to wealth. Only the production of valued goods and services in a market which reflects the consumer’s willingness to pay can relieve poverty and promote prosperity. A people are prosperous to the extent they possess goods and services, not money. All the money in the world—paper or metallic—will still leave one starving if goods and services are not available.

Obviously, none of them were persuaded by the quantity theory of money: if you increase the supply of money without a matching increase in the rate of real growth in the production of goods and services, you’ll have more money chasing the same amount of goods so prices will go up. It’s called inflation. Printing money creates inflation.

There is a school of thought in economic school, the Austrian school of economics, does get excited about fractional reserve banking. The reason it does is to explain how fractional reserve banking creates inflation and promotes the business cycle.

A cycle of booms and busts is not looked upon as a good thing by the Austrian school of economics.

The Austrian school wants to get rid of fractional reserve banking as a way of reducing inflation and reducing the possibility of a loose monetary policy causing booms and busts in the economy.

These monetary cranks from social credit party honestly believed that printing more money will make you wealthier. Thankfully no one asked them to explain their position.

A few supporters of the monetary cranks in the audience asked other members of their views on the ideas of these monetary cranks. Sensibly, they all gave short answers that did not provoke them further and waste more of their precious life listening to them talk nonsense.

If printing money was a winner, as with any populist policy that has a half a chance of working, the parties of the centre-left and centre right would be all over it like flies to s…

Knowledge, ignorance and equilibrium in the market process – Israel Kirzner

27 Aug 2014 Leave a comment

What Austrian Economics IS and What Austrian Economics Is NOT with Steve Horwitz

28 Jul 2014 Leave a comment

in Austrian economics Tags: Pete Boetkke, Steve Horwitz

Pete Boettke’s entry on “Austrian Economics” at the Concise Encyclopedia of Economics, also offered 10 propositions that define Austrian economics:

- Only individuals choose.

- The study of the market order is fundamentally about exchange behaviour and the institutions within which exchanges take place.

- The “facts” of the social sciences are what people believe and think.

- Utility and costs are subjective.

- The price system economizes on the information that people need to process in making their decisions.

- Private property in the means of production is a necessary condition for rational economic calculation.

- The competitive market is a process of entrepreneurial discovery.

- Money is non-natural.

- The capital structure consists of heterogeneous goods that have multispecific uses that must be aligned.

- Social institutions often are the result of human action, but not of human design.

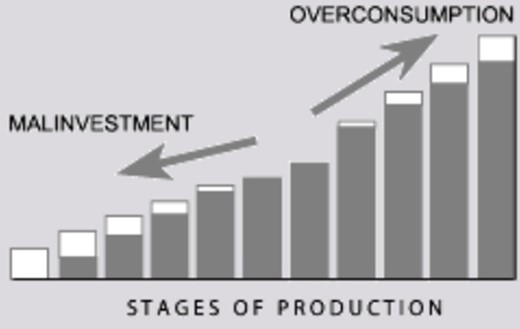

Why is Austrian business cycle theory held to such a high-bar?

14 Jul 2014 Leave a comment

in Austrian economics, macroeconomics Tags: Austrian business cycle theory, Murray Rothbard, rational expectations

I find it surprising that so many concentrate on rational expectations when discussing Austrian business cycle theory (ABCT). Is Austrian business cycle theory the only modern business cycle theory that must reach such a high bar?

Many modern business cycle theories build on information costs and learning and explain that people make forecasting errors because of noisy information, and repeated monetary shocks keeping up this confusion.

A good general explanation of misperceptions theories of business cycle is in Alchian and Allen (1967), which Murray Rothbard called a brilliant textbook. The business cycle is not based on money illusion or on systematic mistakes.

People take time to acquire the necessary information to interpret what has shocked the economy and what these changes mean for them. Additional shocks complicate this learning so there are more errors and confusion continues to affect market choices. Learning is neither instantaneous nor is the requisite information free to collate. People must make do with the incomplete knowledge they have and make choices about market signals that might be spurious or be meaningful signs of change.

Mises, Hayek, and Rothbard all noted in the collection edited by Garrison, for example, that a one-shot monetary shock would be soon uncovered by entrepreneurs, the malinvestments quickly reversed, and the boom would bust. Monetary shock after monetary shock require repeated entrepreneurial revisions and it will take a long time for entrepreneurs to catch up. This is also in Alchian and Allen.

Rothbard (MES pp. 1002-1005) discusses one-time versus repeated and increasingly large in size monetary shocks as the basis for booms and the reasons for the on-going deception of entrepreneurs. The shocks must increase in size to keep injecting more unanticipated noise into monetary and entrepreneurial calculations.

ABCT proposes a more complicated signal extraction problem than in say the Lucas-Phelps islands model. Dispersed and slowly unfolding information must be produced as each new monetary shock ripples its own unique way across the economy, passing through different hands each time. Only slowly does the requisite knowledge about the relative prices effects of each new monetary shock emerge as the result of market interactions and become open to entrepreneurial discovery.

What is perhaps dismissed too easily by Rothbard (but not Mises) is that under a gold standard, increases in the output of gold mining can be well forecasted by entrepreneurs. Rothbard’s best ground is when he notes that "the credit expansion tampered with all their [entrepreneurs’] moorings." A stop-go monetary policy is by definition unpredictable. Gold output fluctuations are irregular but usually small. A unique contribution of ABCT is that the longer the boom, the deeper the bust.

Recent Comments