A Balanced-Growth View of Men’s and Women’s Unbalanced Labor Market Recoveries

19 Jan 2015 Leave a comment

in global financial crisis (GFC), great recession, labour economics, labour supply, macroeconomics, unemployment Tags: jobless recovery

More Evidence against Big-Spending Keynesian Economics

17 Jan 2015 3 Comments

in macroeconomics, politics - USA Tags: Keynesian macroeconomics

Keynesian economics is a perpetual-motion machine for statists. The way to boost growth, they argue, is to have governments borrow lots of money from the economy’s productive sector and then spend it on anything and everything.

Even if the money is squandered on global defense against a make-believe alien attack, according to Keynesians like Paul Krugman!

Krugman also has argued that a real war is good would be good for growth since the goal is simply more spending.

Heck, Krugman even asserted the 9-11 attacks were good for the economy because governments then spent more money.

And Nancy Pelosi actually argued that paying people not to work was a great way of creating jobs. I’m not joking.

Amazing. It’s almost as if these people are secret libertarians and they’re saying crazy things to discredit Keynesianism.

But they’re actually serious. This makes it difficult to tell the difference between satire…

View original post 787 more words

What is the evidence on human capital spillovers? Evidence from the mobility of knowledge workers

17 Jan 2015 Leave a comment

in economic growth, Gary Becker, human capital, job search and matching, labour economics, occupational choice Tags: human capital externalities

While there is a vast literature documenting the large private returns from education and on-the-job human capital (Card 1999; Rubenstein and Weiss 2007; Almeida and Carneiro 2008), evidence of human capital spillovers is limited. Many studies find little evidence of spillovers from education (Lange and Topel (2005), Ciccone and Peri (2006)). Studies even struggle to find small spillovers from another year in high school (Acemoglu and Angrist 2001). Differences in human capital also explain only a small part of cross-national differences in incomes per capita (Hsieh and Klenow 2010; Parente and Prescott 2000, 2005).

The R&D industries offer a case study of the likely size of skills spillovers from worker mobility from large firms. The mobility of technical personnel and the human capital embodied in them across R&D firms is a substantial source of knowledge transfer (Møen 2005). For there to be a spillover, the new employer must pay recruits less than the value added by the job experience and skills they bring to the fold.

A key advantage of studying the mobility of R&D workers for skills spillovers is these industries are populated with many spin-offs founded by the ex-employees of larger firms. R&D spin-offs tend to be larger on average that other new firms and initially employ more advanced, more experienced workers and more technical specialists than do other new firms (Andersson and Klepper 2013).

Capturing the value of skills spillovers from job-hopping is a major business opportunity. The efforts of entrepreneurs to create and enforce property rights over information and other resources as their value increases are central to the organisation of both markets and firms.

A litmus test for the capture of the value of skills spillover is whether wages adjust in line with evolving career opportunities. Becker (2007, p. 134) explains this process of market adaptation and entrepreneurship as follows:

Firms introducing innovations are alleged to be forced to share their knowledge with competitors through the bidding away of employees who are privy to their secrets. This may well be a common practice, but if employees benefit from access to saleable information about secrets, they would be willing to work more cheaply than otherwise.

Møen (2005), Magnani (2006) and Maliranta, Mohnen and Rouvinen (2009) found that employers capture much of the skills spillovers to others by paying R&D workers less early in their careers; later employers pay higher wages to reflect the valued added by the human capital that these R&D recruits bring.

Andersson, Freedman, Haltiwanger, Lane and Shaw (2009) found that software firms in markets with large returns from product breakthroughs pay higher starting salaries to attract star employees. Accounting and legal firms and sports teams also pay more to recruit and retain top performers (Wezel, Cattini and Pennings 2006; Campbell, Ganco, Franco and Agarwal 2012; Rosen 2001).

Employers balance skills and knowledge acquisition through recruitment with in-house development of skills and knowledge. Mason and Nohara (2010) did not find ‘any evidence’ that the external experience of scientists and engineers is any more valuable to firms than is their internal experience.

Firms will pay a wage that equalises the returns on skills acquisition through recruitment with the returns on investing in in-house training. This equalisation of the returns between internal and external sources of skills and knowledge is consistent with competition penalising firms that pay too much or too little for inputs and rewarding entrepreneurs for superior alertness to new opportunities.

The option value of founding or working for a spin-off is also captured in the wages of R&D workers (Kitch 1980; Pakes and Nitzan 1983). Central to a spin-off is carrying on with new ideas and prototypes that the leaving employees judged to be under-valued by the parent firm and they want to build on at their own entrepreneurial risk (Klepper and Sleeper 2005; Klepper 2007).

Large firms are known for incremental innovations while small firms pioneer product break-troughs whose prospects were not as well valued inside large hierarchies (Baumol 2002, 2005; Audretsch and Thurik 2003). Many R&D spin-offs continue with emerging ideas and products that their parents were in the process of abandoning (Hellmann 2007; Chatetterjee and Rossi-Hansberg 2012; Klepper and Thompson 2010). One reason is the developing idea does not fit in with the risk profile and skills of the parent so many spin-offs are friendly (Fallick, Fleischman, and Rebitzer 2006; Chen and Thompson 2011).

Founding or working for a spin-off or start-up is a real prospect. In many innovative industries, upwards of 20 percent of new entrants are intra-industry spinoffs; these firms outperform other new entrants and disproportionately populate the ranks of industry leaders (Klepper and Thompson 2010).

The evidence of large firms spawning more entrepreneurs among scientists and engineers is mixed. Large parent firm size reduces both the probability of leaving, and more so, the probability of leaving to found a spin-off (Andersson and Klepper 2013; Sørensen 2007; Sørensen and Philipps 2011). Spin-offs are less likely from large parents because more of the skills and experience accumulated within large firms is firm-specific human capital and is therefore less mobile into a spin-off.

Scientists and engineers who worked in small firms are ‘far more likely’ to found a spin-off than are their large firm counterparts, and their spin-offs are more likely to be a success (Elfenbein, Hamilton and Zenger 2010; Sørensen and Phillips 2011). Working in smaller firms allows spin-off minded employees to gain the balance and wide array of technical knowledge and management skills that are prized in entrepreneurship (Elfenbein, Hamilton and Zenger 2010; Lazear 2004, 2005).

Working in managerial hierarchies works against founding a spin-off. Tåg, Åstebro and Thompson (2013) found that conditional on size, employees in firms with more layers of management are less likely to enter entrepreneurship, self-employing or quit to go to another firm. They attributed this to the employees in firms with fewer management layers developing a broader range of skills; multiple layers of management offering more promotion opportunities; and skill mismatch is less problematic in more hierarchical firms because there are more chances to move. The higher pay and better career opportunities in larger firms reduces job quits, and with it, skills spillovers and spin-offs.

The wage adjustments for current skills and knowledge transfer opportunities to future employers, start-ups and spin-offs are large. New science graduates accept 20 per cent less in starting pay to work where they can publish more in their own names (Stern 2004).

Scientists and engineers working in R&D accept 20 per cent less pay than other scientists and engineers who work in technical and managerial occupations to secure this more interesting work (Dupuy and Smits 2010). Gibbs (2006) suggested that the U.S. Department of Defense is able to recruit and retain engineers and scientists on low pay because they offer work on some of the most advanced technical research in the world.

Employers who pay full value in wages, share options, learning and R&D opportunities in exchange for the labour and human capital of employees are not benefiting from a skills spillover.

The evidence just reviewed identifies market processes that minimise skills spillovers from large R&D firms to spin-offs. Large firms train their employees in skills that are more often firm-specific and adjust wages to account for the career opportunities that might arise from on-the-job training that is more mobile. The employees of larger firms have longer job tenures in part because their human capital is less mobile.

The marvel of the market: the remarkable foresight of young adults in choosing what to study

16 Jan 2015 1 Comment

in Alfred Marshall, Armen Alchian, economics of education, George Stigler, human capital, job search and matching, labour economics, occupational choice, politics - New Zealand, rentseeking Tags: 2nd laws of supply and demand, Alfred Marshall, Armen Alchian, george stigler, search and matching, skills shortgaes

Known but yet to be exploited opportunities for profit do not last long in competitive markets, including hitherto unnoticed opportunities for the greater utilisation and development of skills and experience (Hakes and Sauer 2006, 2007; Ryoo and Rosen 2004; and Kirzner 1992). Moneyball is the classic example of entrepreneurial alertness to hitherto unexploited job skills which were quickly adopted by competing firms (Hakes and Sauer 2006, 2007).

There is considerable evidence that the demand and supply of human capital responds to wage changes. For example, over- or under-supplied human capital moves either in or out in response to changes in wages until the returns from education and training even out with time (Ryoo and Rosen 2004; Arcidiacono, Hotz and Kang 2012; Ehrenberg 2004).

As evidence of this equalisation of returns on human capital investments across labour markets, the returns to post-school investments in human capital are similar – 9 to 10 percent – across alternative occupations, and in occupations requiring low and high levels of training, low and high aptitude and for workers with more and less education (Freeman and Hirsch 2001, 2008). There is evidence that workers with similar skills in similarly attractive jobs, occupation and locations earn similar pay (Hirsch 2008; Vermeulen and Ommeren 2009; Rupert and Wasmer 2012; Roback 1982, 1988).

Ryoo and Rosen (2004) found that the labour supply and university enrolment decisions of engineers is “remarkably sensitive” to career earnings prospects. Graduates are the main source of new engineers. Engineers who moved out into other occupations such as management did not often moved back to work again as professional engineers. Ryoo and Rosen (2004) observed when summarising their work that:

Both the wage elasticity of demand for engineers and the elasticity of supply of engineering students to economic prospects are large. The concordance of entry into engineering schools with relative lifetime earnings in the profession is astonishing.

Ryoo and Rosen (2004) found several periods of surplus in the market for engineers. These periods of shortage or surplus corresponded to unexpected demand shocks in the market for engineers such as the end of the Cold War.

Figure 1: New entry flow of engineers: a, actual vs. imputed from changes in stock of engineers; b, time-varying coefficients.

Source: Ryoo and Rosen (2004)

Ryoo and Rosen (2004) noted that importance of permanent versus transitory changes in earnings. Transitory rises and falls in earnings prospects have much less influence on occupational choices and the educational investments of students.

In light of these findings that the supply of engineers rapidly adapted to changing market conditions, Ryoo and Rosen (2004) questioned whether public policy makers have better information on future labour market conditions than labour market participants do. When politicians get worked up about skill shortages, the markets for scientists and engineers often where they make extravagant claims about the ability of the market to adapt to changing conditions because of the long training pipeline involved in university study, including at the graduate level.

There can be unexpected shifts in the supply or demand for particular skills, training or qualifications. These imbalances even themselves out once people have time to learn, update their expectations and adapt to the new market conditions (Rosen 1992; Ryoo and Rosen 2004; Bettinger 2010; Zafar 2011; Arcidiacono, Hotz and Kang 2012; Webbink and Hartog 2004).

For example, Arcidiacono, Hotz and Kang (2012) found that both expected earnings and students’ abilities in the different majors are important determinants of student’s choice of a college major, and 7.5% of students would switch majors if they made no forecast errors.

The wage premium for a tertiary degree was low and stable in New Zealand in the 1990s (Hylsop and Maré 2009) and 2000s (OECD 2013). This stability in the returns to education suggests that supply has tended to kept up with the demand for skills at least over the longer term at the national level. There were no spikes and crafts that would be the evidence of a lack of foresight among teenagers in choosing what to study.

All in all, the remarkable sensitivity of engineers to a career earnings prospects, the frequent changes of college majors by university students in response to changing economic opportunities, and the stability of the returns on human capital over time suggest that the market for human capital is well functioning.

The argument that the market was not working well was assumed rather than proven. Likewise, the case for additional subsidies for science, technology, engineering and mathematics because of perceived skill shortages has not been made out. There is a large literature showing that the market for professional education works well.

The onus is on those who advocate intervention to come up with hard evidence, rather than innate pessimism about markets that are poorly understood because of a lack of attempts to understand it. Studies dating back to the 1950s by George Stigler and by Armen Alchian found that the market for scientists and engineers works well and the evidence of shortages were more presumed than real.

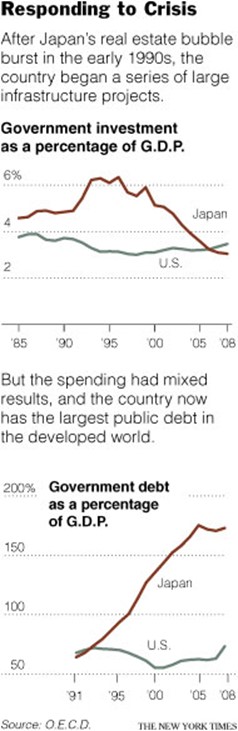

Zombie lending and lower Japanese productivity growth

15 Jan 2015 Leave a comment

in economic growth, macroeconomics, politics - New Zealand, public economics Tags: fiscal stimulus, Japan, Lost Decade, Think Big

The low Japanese productivity growth throughout the 1990s could have been the result of subsidies to inefficient firms and declining industries both directly and through a banking system rolling over loans in arrears to insolvent firms.

This policy is known as zombie lending, and it lowered productivity because higher cost firms kept producing a greater share of Japanese output than would otherwise have been the case (Hayashi and Prescott 2003; Ahearne and Shinada 2005).

- Zombie firms are insolvent firms often propped up with new loans and loan rollovers from Japanese banks.

- Zombie banks are insolvent banks propped up with loans from the central bank and by lax regulatory inspections of their weak loan portfolios and lack of adequate capital.

Japan’s economic policies have until recently kept insolvent banks operating, further encouraging zombie lending, which impeded the flow of capital to the more efficient firms.

The competitive process where zombies shed workers and lose market share was thwarted. The Japanese authorities subsidised insolvent banks and firms and provided credit to some firms and not to others (Prescott 2002; Hayashi and Prescott 2002; Caballero et al. 2005; Hoshi and Kashyap 2004).

The pervasiveness and long-term persistence of zombie lending as a shock to Japanese productivity growth cannot be understated. As Kashyap noted:

The government allowed even the worst banks to continue to attract financing and support their insolvent borrowers

…By keeping these unprofitable borrowers alive, banks allowed the zombies to distort competition throughout the rest of the economy.

Caballero et al. (2008) estimated that 30 per cent of all publicly traded Japanese manufacturing, construction, real estate, retail, wholesale, and service sector firms were on life support from banks in the early 2000s, and that most large Japanese banks only complied with capital standards because regulators were lax in their inspections.

The percentage of zombies hovered between 5 and 15 per cent up until 1993 and rose sharply over the mid-1990s to exceed 25 per cent for every year after 1994 (Caballero et al. 2008).

Figure 1: Prevalence of Firms Receiving Subsidized Loans in Japan

Source: Caballero et al. (2008) Zombie Lending and Depressed Restructuring in Japan. American Economic Review.

Zombie lending is a more serious problem for Japanese non-manufacturing firms than for manufacturing firms (Caballero et al. 2008). Small and medium size firms were also major beneficiaries of zombie lending.

Zombie lending also discourages new investments that increase Japanese productivity, encourages inefficient firms to avoid making the decisions necessary to raise their profitability, and impedes the solvent Japanese banks from finding good lending opportunities (Caballero et al. 2008; Sekine et al. 2003). As Kashyap noted:

Usually when an industry is hit by a bad shock, many firms exit… In Japan, firms never exited. Given that they never exited, it is not surprising that new firms weren’t created.

Under normal conditions, higher cost firms would go bankrupt and be replaced by new and better ideas and firms. Instead, firms that were more efficient than the zombie firms tended to exit industries because their demise does not require the banks to acknowledge large bad loans. This exit of the firms of intermediate efficiency rather than the exit of the least efficient firms dragged productivity down even further (Nishimura et al. 2005; Okana and Horioka 2008). New Zealand in the 1970s and in the early 1980s also had a range of policy measures that supported high-cost firms and declining industries.

When bankrupt firms can stay in business, they retain workers who otherwise would be willing to work for lower wages at a healthy firm and depress market prices for their products. Low prices and high wages reduce the profits that more productive firms can earn which discourages entry and investment.

The creation of new jobs is a measure of industry dynamism. In manufacturing, which suffered the least from the zombie problem, job creation hardly changed from the early 1990s to the late 1990s. In contrast, there was a large decline in job creation in the non-manufacturing sectors, particularly in construction (Caballero et al. 2008; Hoshi 2006; Caballero et al. 2008).

There was less restructuring of employment and market shares in favour of the more productive firms. The gap in productivity growth between the Japanese manufacturing and non-manufacturing sectors more than doubled over the 1990s (Caballero et al. 2008).

Japanese R&D spending has also slowed down significantly since the start of the 1990s (Comin forthcoming). The gap in the rate of computer adoption between Japan and USA also increased in the 1990s. The speed of diffusion of new technologies slowed to the point that South Körea has now surpassed Japan in the diffusion of computers and the Internet (Comin forthcoming).

Over the 1990s, there were ten massive fiscal packages to maintain employment and investment. Much of this additional Japanese government spending was on public works and other projects whose social payoffs have been queried by independent observers. The consumption tax was increased from 3 per cent to 5 per cent in 1997. There were two rounds of temporary tax cuts – for 2 years only.

Japan pursued economic policies in response to a recession that stifled total factor productivity by providing bad incentives to the private sector.

The unproductive firms depressed Japanese productivity because they competed for labour and capital that could have been used by the more productive firms. Zombie lending allowed many firms to stay in business long after the monetary policy changes that uncovered their unprofitable petered out. The diversion of resources to these insolvent firms prevented a productivity recovery. The lack of a productivity recovery depressed wages, incomes and consumer demand.

The zombie lending and fiscal packages compounded the 1990 monetary contraction into the highly persistent shocks that were required to be able to depress Japanese productivity growth for more than a decade.

More and more resources were tied up in high cost firms and in declining industries. This was rather than be reallocated to more productive uses by the normal market processes of relative price and wage changes, free entry and profit and loss. Kashyap argues that:

The experience in Japan definitely shows that providing subsidized credit to dying firms will be costly over time. Keeping an industry from restructuring only delays the day of reckoning and raises the cost substantially

…There are many examples besides Japan where people fail to recognize that it is dangerous to keep people attached to businesses that are fundamentally unprofitable

The massive Japanese government investments have echoes of the ‘Think Big’ energy investments in New Zealand in the late 1970s.

The productivity impact of ‘Think Big’ was suspect. In addition, state-owned enterprises offering a net return of zero to the Crown in the 1980s has Japanese parallels.

The propping up of high cost state owned and private firms in the 1970s and 1980s in New Zealand helped to depress productivity growth rates. State-owned enterprises offered a net return of about zero to the taxpayer, even as recently as last year in New Zealand.

More and more resources were tied up in New Zealand in the high cost firms and declining industries than be reallocated to more productive uses by the market processes of price and wage changes, free entry and profit and loss. The lack of productivity growth depressed wages, incomes and consumer demand in New Zealand.

The productivity based explanations for the slumps in New Zealand from 1974 to 1992 and in Japan from 1990 to 2003 have a number of common threads.

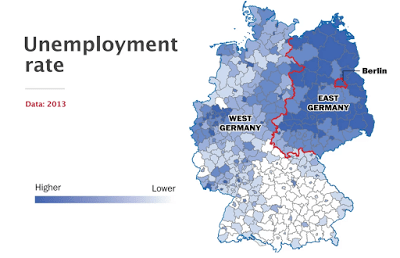

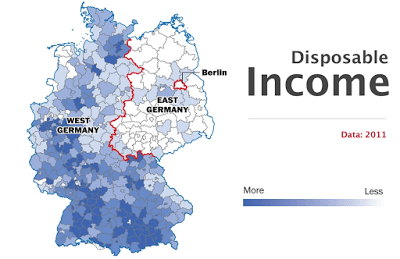

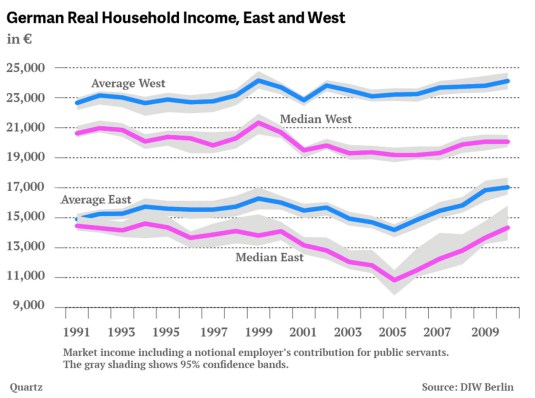

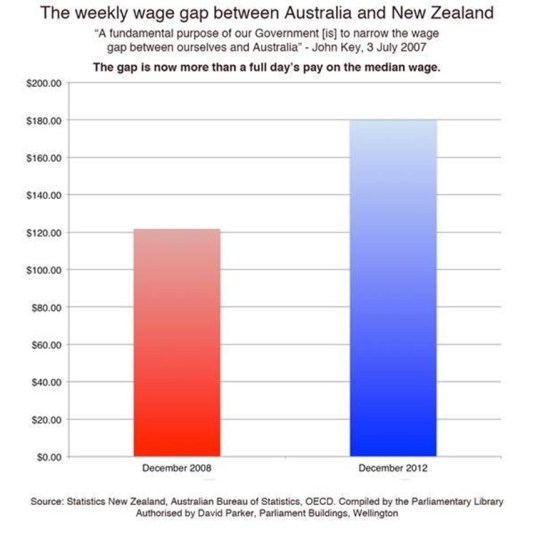

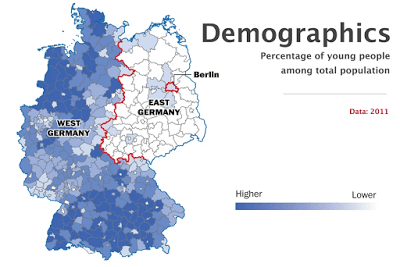

Why is anybody still living in East Germany (or New Zealand)?

14 Jan 2015 1 Comment

in economic history, macroeconomics, politics - Australia, politics - New Zealand Tags: East Germany, Germany, immigration, Trans-Tasman income gap

When I pointed to Jennifer Hunt’s so titled paper freshly released in 2000 on why does anyone still live in East Germany, none of my New Zealand colleagues understood the parallel with their own country.

The wage gap between East and West Germany is about the same as the wage gap between Australia and New Zealand.

- East Germans have the advantage of being able to getting their car to go to the west. Some do commute from the east to jobs in the West; and

- New Zealanders have to get into a plane and commuting done a daily basis is really out of the question – the air flight time alone is three hours.

There are in fact bigger language, or more correctly dialect differences between Germany than there are across the Tasman Sea between New Zealanders and Australians. Educational standards are similar between New Zealanders and Australians.

In 1997 GDP per capita in East Germany was 57% of that of West Germany, wages were 75% of western levels, and the unemployment rate was at least double the western rate of 7.8%.

The wage gap across the Tasman between New Zealand and Australia is about one third. Wage gaps between East and West Germany and between Australia and New Zealand are about the same.

Australia and New Zealand have a single integrated labour market. Any New Zealander Australian is free to work in the other country.

New Zealanders are not eligible for social security benefits if they first arrived in Australia after mid-2001. Prior to 2001, New Zealanders have the same rights as Australians for social security benefits.

One would expect that if capital flows and trade in goods failed to bring convergence between East and West Germany, labour flows should respond, enhancing overall efficiency.

Same goes between Australia and New Zealand. About 35,000 New Zealanders used to move to Australia each year, but that’s recently dried up to about zero. Funnily enough, by the late 1990s net emigration from East Germany has fallen from high levels in 1989-1990 to close to zero.

Jennifer Hunt found through her analysis of the eastern sample of the German Socio-Economic Panel for 1990-1997 that commuting is unlikely to substitute substantially for emigration.

Wage convergence between the East and the West was a main factor that stemmed immigration. The individual-level data further indicate that emigrants are disproportionately young and skilled, and that individuals suffering a layoff or non-employment spell are also much more likely to emigrate. This is all as predicted by the Roy model of immigration self-selection.

Like all human capital investments, both international and within country migration is based on the comparison of the present value of lifetime earnings in all available employment opportunities. Individuals compare the potential incomes and the destination country with the income in the home countries, and make the migration decision based on these income differentials (net of mobility costs).

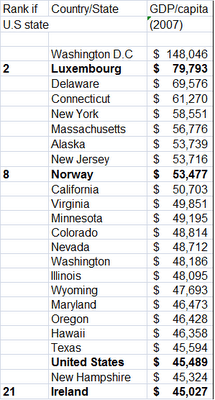

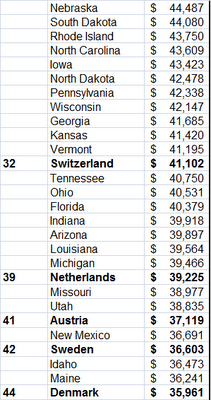

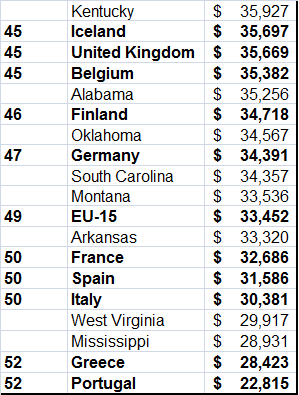

How does the standard of living compare across the EU?

13 Jan 2015 Leave a comment

in macroeconomics Tags: European Union

Super-Economy: Dynamic America, Poor Europe

13 Jan 2015 Leave a comment

in economic growth, liberalism, macroeconomics Tags: Eurosclerosis

The role of the introduction of a five day working week in Japan’s Lost Decade

13 Jan 2015 2 Comments

in business cycles, economic growth, economic history, labour economics, labour supply, macroeconomics, monetarism Tags: Japan, Japanese banking system, Lost Decade

When I lived in Japan between 1995 and 1997, they are undergoing the transition from a six-day week to a five day week. At the time, workers at my University had to show up on Saturday morning. They then went home at lunchtime. Saturday morning at the office was phased out a few years later.

In explanations of the Lost Decade of growth in Japan dating from the early 1990s, with the exception of Ed Prescott, the explanation that the Japanese simply chose to produce less per worker over the course of the 1990s does not figure highly.

The Japanese working week was reduced by law from 48 to 44 hours per week in 1988 and further reduced by the same labour standards law to 40 hours per week from 1993 (Prescott 1999; Hayashi and Prescott 2002). The Japanese stopped routinely working on Saturdays over the 1990s. The number of national holidays was increased by three and an extra day of annual leave was also prescribed by law.

Figure 1 shows this regulatory change about the length of the standard working week that started in 1987 was followed by a sharp drop in hours worked per working per working age Japanese over the period 1988 to 1993. The Japanese working age population is defined as those aged 20 to 69 (Hayashi and Prescott 2002).

Figure 1: Weekly hours worked per Japanese aged 20 to 69, 1970-2000

Source: Hayashi and Prescott 2002.

The regulatory process to end the standard six day working week in Japan straddled the start of the Lost Decade. This major change in the regulation of the supply of labour per week in the number of hours worked and the stagnation of GDP growth soon after could be more than a coincidence (Prescott 1999; Hayashi and Prescott 2002).

Americans work more hours a year than workers in Japan. But both work less than before. Data: buff.ly/1LhU5gH http://t.co/7oaGYKLRmk—

HumanProgress.org (@humanprogress) August 18, 2015

More employment did not fill the short-fall in weekly labour supply per worker after the introduction of the 44 hour week and then the 40 hour week in Japan. Many offices and factories closed on Saturday rather than employ more to make up the hours. The regulatory change was a clear cut constraint on the length of the working week that was hard to get around because of the need to recruit a separate set of workers to come in on Saturday afternoon and then all day Saturday.

During the transition to a five day working week, Japanese real GDP growth should slow down because output levels must taper during a transitional period because one day per week less in labour is supplied in production and capital is being worked for one day a week less than before (Prescott 1999; Hayashi and Prescott 2002).

Output per working age person depends on capital-labour ratios, on hours worked per week and on changes in total factor productivity due to factors such as technological progress and changes in institutions and economic policies.

The effects of the change in the length of the working week on output per working age Japanese will persist for a significant time because investment plans and the capital stock must also adjust to a shorter working week. This is another example of a highly persistent shock that can partly account for the Lost Decade. As Prescott (1999) observed:

Given the change in Japanese law and the resulting drop in normal market hours, growth theory predicts the almost stagnant output of the Japanese economy in the 1990s. This reduction in market hours lowered the marginal product of capital, making investment unprofitable.

Given the lack of profitable domestic investment opportunities, the Japanese began saving by investing abroad. This explains Japan’s large trade surpluses

…The Japanese economy in the 1990s is not as depressed as the U.S. economy was in the 1930s. Market hours in Japan in the 1990s have fallen only half as much as market hours fell in the United States during the Great Depression.

More importantly, the reduction in market hours in Japan in the 1990s was the stated objective of policy.

The reduction in weekly hours worked will also reduce the working week of capital because labour and capital are usually complementary inputs. The reduced length of the working week will see some existing capital producing less, some capital will go spare, and the rate of wear and depreciation will fall.

The drop in weekly hours worked will lower the marginal productivity of existing and new capital which will make new capital investments in Japan less profitable than before. Net investment will be less while the Japanese capital stock is adjusting down to the reduced working week for capital and labour.

Measured total factor productivity will fall because of an under-utilisation of a capital stock that is now larger than required for the available labour force. Net investment will decline by a large amount because investment demand is a small yearly addition to the capital stock.

For example, if annual investment demand is 5 per cent of the capital stock, and the desired capital stock becomes 1 per cent smaller than previous, annual net investment will fall 20 per cent. GDP growth will resume at the trend rate once the lower level of output per working age person is reached.

For those that still doubt, consider the contrary, what would you expect to happen in your country moved from five day week before day working week? Do you expect workers to produce as much as before? Britain was on a three day working week during the coal miners’ strike. As expected, output fell because the working week was shorter.

The main gap in the English language literature about the reduction in the working week in Japan is a lack of publications I can find by Japanese economists discussing what predictions of a made about the likely consequences for output, investment and productivity before the reduction in the length of working week was legislated. Did the reduction in the length of the working week in Japan turn out as planned and predicted before it was implemented?

France introduced a 35 hour week some years ago. Although there were various options for over time, albeit strictly regulated, a uniform prediction was that the 35 hour week would reduce productivity. The new workweek was phased in slowly, with large firms adopting it in February 2000 and smaller firms doing so only in January 2002.

French employees were expected to bear only a small part of the cost of the working-time reduction, continuing to earn roughly the same monthly income – in line with the unions’ slogan ’35 hours pays. To ease that transition, the law reduced the overtime premium for small firms and increased their annual limit on overtime work compared with large firms.

The reduction in the length of the French working week failed as work sharing strategy and reduced productivity. This was a fair summary by the IMF:

The 35-hour workweek appears to have had a mainly negative impact. It failed to create more jobs and generated a significant—and mostly negative—reaction both from companies and workers as they tried to neutralize the law’s effect on hours of work and monthly wages.

While it cannot be ruled out that individuals who did not change their behaviour because of the law became more satisfied with their work hours, simple survey measures do not show increased satisfaction.

Between 1997 and 2000, Quebec reduced its standard workweek from 44 to 40 hours to stimulate jobs growth – the old work sharing ideal. The Quebec policy contained no suggestion or requirement that employers provide wage increases to compensate workers for lost hours.

Despite a 20% reduction among full-time workers in weekly hours worked beyond 40, the policy failed to raise employment at the provincial level or within industries. If anything, there were job losses.

Japan was the only case where a reduction in the length of the working week met with wide approval by the public and people simply stopped working on Saturdays. The law succeeded simply because it did but it was designed to do: reduce the number of days existing workers worked. Japan was undergoing mild deflation at the time, so the need to reduce wages was minimal.

Annual hours worked per employed Japanese has continued to slowly taper down since the late 1990s, which may be a further explanation of its continual slow growth.

David Andolfatto wrote a nice paper explaining the consequences for the financial and monetary sectors of this reduction in the length of the Japanese working week:

- a steady decline in bank lending;

- the money multiplier declines;

- nominal interest rates that are close to zero; and

- massive infusions of liquidity by the Bank of Japan that seem to have no effect at all.

In his analysis, David Andolfatto referred generally to a productivity slowdown as discussed by Prescott rather than to the specifically to the reduction in the length of the Japanese working week. Nothing detracts in his analysis, as Andolfatto said, that Japan has a problem: lagging productivity growth and as Andolfatto concluded:

…monetary and fiscal policies, or reforms directed exclusively at the banking sector, are unlikely to re-establish productivity growth. What is likely needed are economy-wide reforms that enhance the willingness and ability of individuals to adopt potentially disruptive technological advancements and work practices.

For those who are job-hunting after the holidays

12 Jan 2015 Leave a comment

in job search and matching, personnel economics Tags: search and matching

I find the biggest mistake made at job interviews at the interview panel forget that you are interviewing them as prospective employer.

If they can’t even be polite and friendly to you before you work for them, imagine what they’re like every day.

About 20% of the people I’ve met at job interviews I would never want to work with, much less work for.

Recent Comments