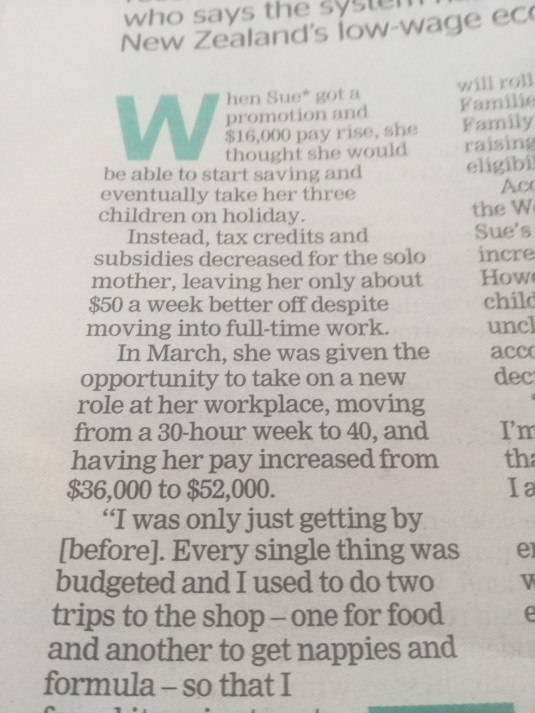

Poverty traps explained

21 Jun 2018 Leave a comment

in applied price theory, labour economics, labour supply, politics - New Zealand, public economics, welfare reform Tags: family poverty, poverty traps

Johan Norberg: The Truth about Swedish Socialism

05 Jun 2018 1 Comment

in applied price theory, economic history, macroeconomics, Public Choice, public economics Tags: growth of government, size of government, sweet

Milan Vaishnav | When Crime Pays: Money and Muscle in Indian Politics

07 May 2018 Leave a comment

in applied price theory, constitutional political economy, economics of bureaucracy, economics of crime, Public Choice, public economics, rentseeking Tags: economics of corruption, India

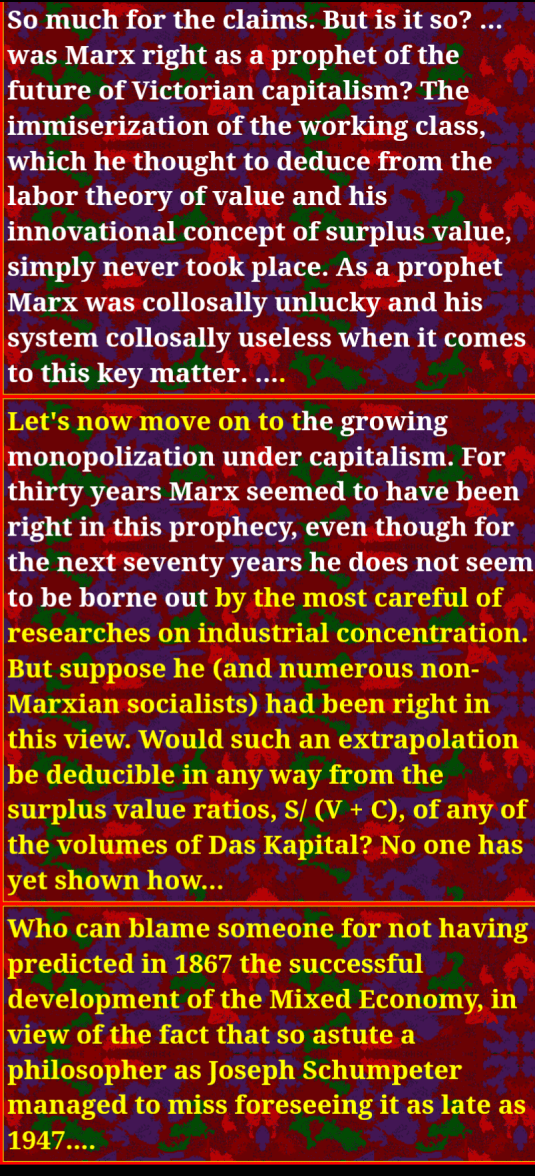

Was Karl Marx right? | The Economist

05 May 2018 Leave a comment

in applied price theory, business cycles, development economics, economic history, economics of bureaucracy, entrepreneurship, history of economic thought, industrial organisation, labour economics, macroeconomics, Marxist economics, poverty and inequality, Public Choice, public economics Tags: economics of socialism

From Paul Samuelson’s essay on marxist economics

Climate change suits versus disclosures of threats to tax bases to the municipal bond market – interview with Stephen Winterstein

03 May 2018 Leave a comment

in economics of crime, economics of information, environmental economics, financial economics, global warming, law and economics, politics - USA, Public Choice, public economics, rentseeking Tags: climate alarmism, securities fraud

#VirtueSignalling @nzprocom wants a great big increase in an old tax

27 Apr 2018 Leave a comment

in applied price theory, applied welfare economics, energy economics, environmental economics, global warming, politics - New Zealand, Public Choice, public economics Tags: carbon pricing, carbon tax

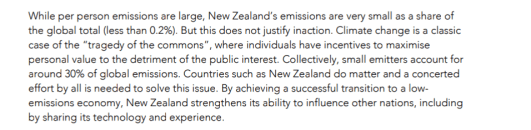

#VirtueSignalling @nzprocom on bit players leading the way in global public good supply

27 Apr 2018 Leave a comment

in applied price theory, applied welfare economics, energy economics, environmental economics, global warming, politics - New Zealand, Public Choice, public economics, rentseeking Tags: free riding, international public goods

Is there a Natural Resource Curse?

24 Mar 2018 Leave a comment

in applied price theory, applied welfare economics, comparative institutional analysis, constitutional political economy, development economics, economic history, growth disasters, growth miracles, international economics, Public Choice, public economics, rentseeking, resource economics Tags: resource curse

Why libertarianism is a marginal idea and not a universal value | Steven Pinker

10 Mar 2018 Leave a comment

in applied price theory, development economics, economic history, fiscal policy, growth disasters, growth miracles, income redistribution, Public Choice, public economics Tags: Director's Law, growth of government, Steven Pinker, Wagner's Law

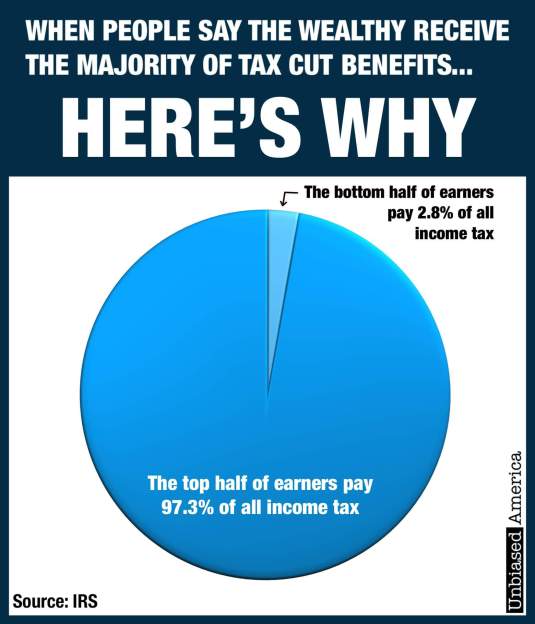

The new corporate tax landscape

19 Dec 2017 Leave a comment

in fiscal policy, politics - New Zealand, politics - USA, public economics Tags: company tax

Instead of what? @NZSuperfund contribution resumption @taxpayersunion

14 Dec 2017 Leave a comment

in politics - New Zealand, public economics

Would it have been cheaper just to raise the eligibility age to 67 for New Zealand superannuation? By 2022, either health or education spending could have been 15% higher.

Recent Comments