From https://www.aeaweb.org/articles?id=10.1257/jep.23.4.147

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

17 Nov 2020 Leave a comment

in applied price theory, applied welfare economics, economic growth, entrepreneurship, macroeconomics, Marxist economics, public economics Tags: company tax, optimal tax theory, taxation and investment, taxation and savings

19 Dec 2017 Leave a comment

in fiscal policy, politics - New Zealand, politics - USA, public economics Tags: company tax

02 Dec 2016 Leave a comment

in applied price theory, economic growth, entrepreneurship, international economics, macroeconomics, politics - USA, public economics Tags: 2016 presidential election, company tax

02 Jun 2016 Leave a comment

in applied price theory, politics - Australia, politics - New Zealand, public economics Tags: Australia, company tax, international tax competition, tax incidents, taxation and entrepreneurship, taxation and investment

28 May 2016 Leave a comment

in economic history, financial economics, politics - USA, public economics Tags: company tax, Leftover Left, pension fund socialism, Peter Drucker, tax havens, taxation and entrepreneurship, taxation and investment, Twitter left

Peter Drucker first pointed out in the 70s that the retirement savings of ordinary workers will end up opening the majority of public listed companies. That day has come much to the disappointment of the Leftover Left ranging from Thomas Piketty to Max Rashbrooke.

Source: CONVERSABLE ECONOMIST: US Corporate Stock: The Transition in Who Owns It.

Any call for higher taxes on investment incomes and capital and even tax havens is an attack on the retirement savings of ordinary workers.

28 Apr 2016 Leave a comment

in public economics Tags: company tax, rational irrationality, tax incidence, taxation and entrepreneurship, taxation and investment

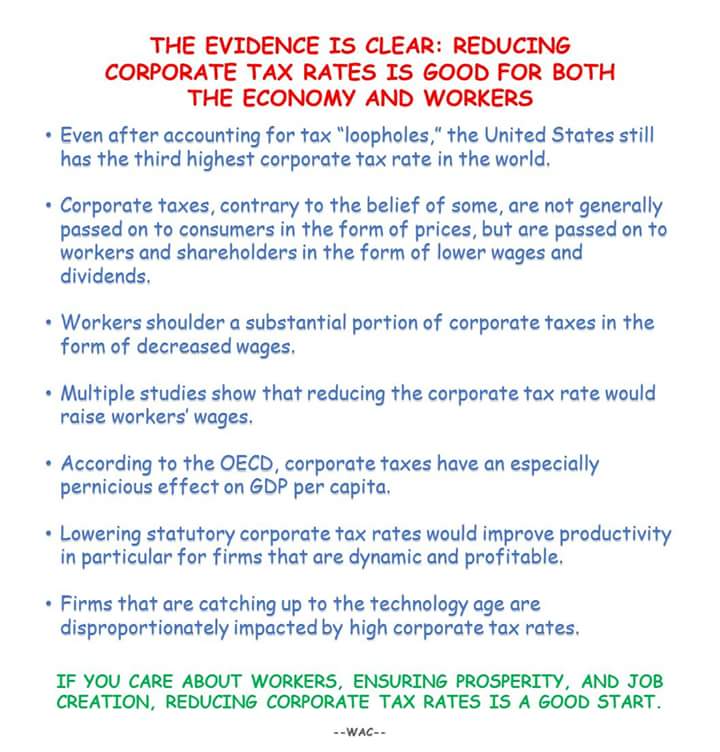

The tax incidence of sales taxes is understood by everybody but who pays company tax is stubbornly misunderstood. The seller is sending the tax cheque to the taxman does not fool anyone regarding who ultimately pays sales taxes.

The tax incidence of sales taxes is understood by everybody but who pays company tax is stubbornly misunderstood. The seller is sending the tax cheque to the taxman does not fool anyone regarding who ultimately pays sales taxes.

Everyone expects that sales tax increases such as of the GST or VAT will be passed on to buyers but sometimes a little bit is absorbed in terms of lower profits by sellers if it is more than the market can bear.

When it comes to company taxes, this intuitive understanding of the economics of the incidence of taxes completely disappears. There is a strong belief that only investors pay the company tax in the form of dividends.

The notion that investors may reduce their investment and therefore the amount of capital with which workers can work is stoutly denied as is the implications for lower than otherwise wages because of this.

The possibility that the entire company tax may show up as lower wages when capital is internationally mobile is just not even contemplated. This is despite foreign direct investment being welcomed on the grounds that more capital means higher wages for local workers.

Likewise, when a factory is re-located offshore, it is understood that that will harm wages. That understanding does not carry through to company tax incidence when the factory relocates offshore because of low company taxes rather than import competition.

17 Apr 2016 Leave a comment

in applied price theory, entrepreneurship, fiscal policy, macroeconomics, politics - New Zealand, public economics Tags: company tax, Gareth Morgan, rational irrationality, taxation and entrepreneurship, taxation and investment, taxation and labour supply, taxation of capital income

The Morgan Foundation gave optimal tax theory a pass in yesterday’s publication about taxes on land and capital. Gareth Morgan is keen on a comprehensive capital tax.

Source: Taxing Wealth & Property – What Works? A Morgan Foundation Report.

This failure to refer to optimal tax theory is despite the Foundation’s strong commitment to evidence-based policy. Any discussion of tax policy that is evidence-based must refer optimal tax theory.

Source: Morgan Foundation, Public Policy Education.

<p>

31 Mar 2016 Leave a comment

in applied price theory, public economics Tags: capital gains tax, company tax, family tax credits, in-work tax credits, taxation and entrepreneurship, taxation and investment, taxation and labour supply

18 Mar 2016 Leave a comment

in business cycles, economic history, fiscal policy, great recession, macroeconomics, politics - USA, public economics Tags: company tax, company tax rate, growth of government, GST, indirect taxation, property taxes, size of government, Social Security contributions, taxation and investment, taxation and labour supply, welfare state

The only major change in the US tax mix in the last 50 years has been greater reliance on social security contributions.

Source: OECD Stat.

The share going to income taxes bobbing up and down quite a lot in the last 30 years much of that to do with the business cycle. In the 1990s, the share of taxes from personal income increased during boom times. In the Great Recession, the tax share to income tax rose with the declining economy as did that on corporate profits.

18 May 2015 Leave a comment

in politics - New Zealand, politics - USA, public economics Tags: company tax, endogenous growth theory, foreign direct investment, lost decades

New Zealand is one of only two developed countries, the other being Finland, that switched from a territorial tax system to a worldwide system.Both eventually returned to a territorial tax system for competitiveness reasons. New Zealand went one step further in their experiment with worldwide taxation by ending deferral.

This resulted in a twenty year stagnation in foreign investment at a time when foreign investment was growing dramatically in the rest of the developed world.

This coincided with an economic decline in New Zealand relative to Australia and the rest of the developed world. Because foreign investment is key to accessing the world’s consumers, it is not surprising that less foreign investment translated to less economic prosperity at home.

The New Zealand experience shows that ending or limiting deferral in the United States, as President Obama and others have proposed, would likely have severe economic downsides. Instead, as New Zealand eventually did in 2009, the U.S. should implement a territorial system that exempts foreign earnings.

via New Zealand’s Experience with Territorial Taxation | Tax Foundation.

03 Feb 2015 Leave a comment

in politics - Australia, politics - New Zealand, politics - USA, Public Choice, public economics Tags: capital gains tax, company tax, efficient taxes, optimal taxes

28 Mar 2014 1 Comment

in labour economics, public economics, Rawls and Nozick Tags: company tax, economic growth, flat rate consumption tax, higher wages, income tax, inequality

John Rawls is often put forward by political progressives as the starting point for political philosophy. Rawls pointed out that behind the veil of ignorance, people will agree to inequality as long as it is to everyone’s advantage.

Rawls was attuned to the importance of incentives in a just and prosperous society. If unequal incomes are allowed, this might turn out to be to the advantage of everyone.

Rawls lent qualified support to the idea of a flat-rate consumption tax (see A Theory of Justice, pp. 278-79). He said that:

A proportional expenditure tax may be part of the best scheme [and that adding such tax] can contain all the usual exemptions.

The reason why Rawls lent qualified support to the idea of a flat-rate consumption tax was because these taxes:

impose a levy according to how much a person takes out of the common store of goods and not according to how much he contributes.

A simple way to have a progressive consumption tax is to exempt all savings from taxation. Taxable consumption is calculated as income minus savings minus a large standard deduction. Different countries use different terms to describe the minimum amount that must be earned before any taxes are paid.

Income tax must be opposed on social justice grounds, but not progressive consumption taxes.

Given that the super-rich – the top 0.1% of income earners – do not spend much of their incomes, especially on the way up building their businesses, they could be rather over-taxed!

Steven Kaplan and Joshua Rauh’s “It’s the Market: The Broad-Based Rise in the Return to Top Talent”, Journal of Economic Perspectives (2013) found that:

Today’s super-rich are highly productive because they produce new and better products and services that people want and are willing to pay for. These rewards for entrepreneurship and hard work guide people of different talents and skills into the occupations and industries where their talents are valued the most. The efficient allocation of talent and income maximising occupational choices were important to Rawls’ framework.

Another important role for incentives is it rewards entrepreneurial alertness. People will look for and take advantage of hitherto unnoticed business opportunities if they are rewarded for doing so. These private rewards for greater effort, excellence and superior alertness are the driving force of the market. Most of the innovation that drives modern prosperity would not have occurred but for the lure of profit.

Rawls was keen on stiff inheritance taxes to prevent the “large-scale private concentrations of capital from coming to have a dominant role in economic and political life”. His support for inheritance taxes was out of concern with a concentration of political power rather than improving incentives.

Rawls overrated the power of the rich to buy political influence as do many on the Left. They do not understand Director’s law of public expenditure and the theories of the median voter and the expressive voter. The major political parties all chase the swinging voter in the middle class.

Rawls’ views on incomes taxes and the rich are rather under-discussed among his champions on the progressive Left. Google John Rawls and income taxes and you do not get many hits or papers of any substance.

With his emphasis on fair distribution of income, Rawls’ initial appeal was to the Left, but left-wing thinkers started to dislike his acceptance of capitalism and tolerance of large discrepancies in income. Many moved on. Rawls excluded envy from deliberations behind the veil of ignorance. This may be why he lost some of his initial appeal to some.

You must admire his consistency. Rawls was happy for people to be super-rich as long as they saved and invested their resources. Everyone in society gains from those investments and is better off.

Robert Lucas (1990) estimated that a revenue neutral elimination of all taxes on income from capital and on capital gains would increase the U.S. capital stock by about 35% and consumption by 7%. Hans Fehr, Sabine Jokisch, Ashwin Kambhampati, and Laurence J. Kotlikoff (2014) found that eliminating the corporate income tax would raise the U.S capital stock (machines and buildings) by 23%, output by 8% and the real wages of unskilled and skilled workers by 12%. Is taxing the rich worth this large a lost wage rise?

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A History of the Alt-Right

Econ Prof at George Mason University, Economic Historian, Québécois

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Recent Comments