Short Cut: Macron’s Scandi-Solution for France

16 May 2017 Leave a comment

in economics, fiscal policy, labour supply, macroeconomics, minimum wage, Public Choice, public economics, welfare reform

Macroeconomic Consequences of Taxing the Rich

11 May 2017 Leave a comment

in fiscal policy, macroeconomics, politics - USA, Public Choice, public economics, sports economics Tags: taxation and labour supply, top 1%

Instead of contributing to the @NZSuperfund? @TaxpayersUnion

11 May 2017 Leave a comment

in politics - New Zealand, population economics, public economics Tags: ageing society, social insurance, Social Security

Spending on health or education could have been increased by a quarter or the company tax rate cut by up to 10 percentage points but for the Cullen Fund.

Who Really Pays Business Taxes?

06 May 2017 Leave a comment

in applied price theory, Milton Friedman, Public Choice, public economics Tags: tax incidence

Trailblazers: The New Zealand Story – Full Video

29 Apr 2017 Leave a comment

in economic history, economics of regulation, industrial organisation, politics - New Zealand, Public Choice, public economics, rentseeking, survivor principle

Important to mention tax credits when discussing the working poor? @JordNZ

21 Apr 2017 Leave a comment

in labour economics, politics - New Zealand, poverty and inequality, public economics, welfare reform Tags: child poverty, family poverty, family tax credits, taxation and labour supply

Which matters more to the incentive effects of income tax? @JordNZ

20 Apr 2017 Leave a comment

in politics - New Zealand, public economics Tags: average tax rates, family taxation, Marginal tax rates, taxation and labour supply

So New Zealanders do not pay much income tax @TaxpayersUnion

19 Apr 2017 Leave a comment

in politics - USA, public economics Tags: family tax credits, family taxation, Marginal tax rates, taxation and labour supply

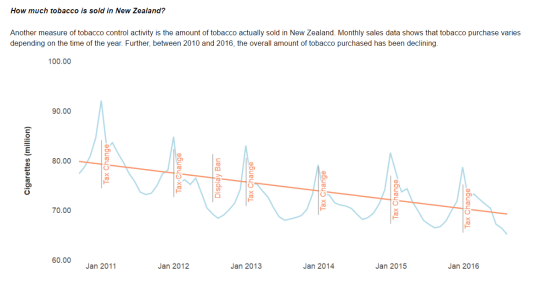

Do smokers stockpile in anticipation of tax rises?

16 Apr 2017 Leave a comment

Source: TCDR – Overview

No income tax to cut anymore until household incomes in the six figures!

31 Mar 2017 Leave a comment

The wage bump from 1% Oz company tax cut @TheAusInstitute @GrattanInst @JordNZ

31 Mar 2017 Leave a comment

in economic growth, fiscal policy, politics - Australia, politics - New Zealand, public economics Tags: company tax incidence, endogenous growth theory, optimal tax theory

How wasteful is the Oz company tax? @TheAusInstitute @GrattanInst

30 Mar 2017 Leave a comment

Source: The incidence of company tax in Australia, Xavier Rimmer, Jazmine Smith and Sebastian Wende, Australian Treasury working paper.

Morgan’s capital tax forgot 30% retirees move every 5 years @TaxpayersUnion

30 Mar 2017 Leave a comment

in politics - New Zealand, population economics, public economics Tags: 2017 New Zealand election, capital taxation, inheritance taxes, Opportunities Party, optimal tax theory

With 30% of retirees changing address every 5 years, they will have to downsize into hovels because they have to pay IRD the great big new tax on their capital championed by Morgan and his Opportunities Party well before they die.

Morgan’s 1.8% tax on equity capital is not an inheritance tax for the majority of retirees. It is a nest egg tax as they downsize after the kids fly the nest, grandchildren appear or they move to a more convenient place as they become frail.

Because they will have to pay back taxes of tens of thousands of dollars to IRD every time they sell their house, retirees either will not be able to move closer to family because of grand-children or health issues or they will have difficulty moving into a retirement home of their choice.

This is the first in a series of blogs showing how the Opportunities Party is too clever by half in its manifesto development. By insisting on having different policies to everybody else by a good country mile, it ends up having to take up the policies others rejected because they do not work.

In the case at hand, they put an inheritance tax on ordinary New Zealanders at the same rate as the rich including the founder of the Opportunities Party. This tax will be the only capital tax anywhere that is not progressive.

Over 70% of the retired own their own house mortgage free. The majority of that equity will now go to IRD plus interest by the time both members of the couple die given the average capital tax will be about $10,000 per year in Wellington and twice that in Auckland. They face up to 20 to 25 years of deferred capital taxation that will take half the value of their house easily. It will be hardest if they must cash-out their house to go into retirement home.

The purpose of buying a house is to have a nest egg for retirement. You may draw down that capital because of health issues or pass it on to children if you are luckier than that.

Morgan wants to radically change the way in which retirees go into the evening of their days. People who just managed to save for a house will have nothing to pass on to their children. No more bank of mum and dad either.

Sharp ratios of @NZSuperFund since inception @TaxpayerUnion

28 Mar 2017 Leave a comment

in financial economics, fiscal policy, politics - New Zealand, public economics Tags: sharp ratios, sovereign wealth funds

The Sharp ratio describes how much excess return you are receiving for the extra volatility that you endure for holding a riskier asset. If manager A generates a return of 15% while manager B generates a return of 12%, it would appear that manager A is a better performer. But if manager A took much larger risks than manager B, manager B may be a better risk-adjusted return.

The Sharpe Ratio such as those below of the NZ Superannuation Fund can be used to compare two funds on how much risk a fund had to bear to earn excess return over the risk-free rate.

Source:New Zealand Superannuation Fund response to Official Information Act request.

Recent Comments