Randall Kroszner’s advice for the next president

02 Dec 2016 Leave a comment

in applied price theory, economic growth, entrepreneurship, international economics, macroeconomics, politics - USA, public economics Tags: 2016 presidential election, company tax

Which is worse? The tax or regulation?

30 Nov 2016 Leave a comment

in applied price theory, economics of regulation, Public Choice, public economics Tags: tax incidence theory

Post-disaster co-operation: The voluntary provision of weakest-shot public goods

16 Nov 2016 Leave a comment

in applied price theory, economics of natural disasters, public economics Tags: economics of alliances, free riding, post-disaster cooperation, public goods, weakest shot public goods

After a natural disaster, both the economic and social fabric and the survival of individual employers each become weakest-shot public goods. The provision of these public goods temporarily depend by much more than is usual on the minimum individual contributions made – the weakest shots made for the common good. The supply of most public goods usually is not dependent on the contributions of any one user.

The classic example of a weakest shot public good by that brilliant applied price theorist Jack Hirschleifer is a dyke or a levee wall around a town. It is only as good as the laziest person contributing to its maintenance on their part of the levee. Vicary (1990, p. 376) lists other examples:

Similar examples would be the protection of a military front, taking a convoy across the ocean going at the speed of the slowest ship, or maintaining an attractive village/landscape (one eyesore spoils the view).

Many instances of teamwork involve weak-link elements, for example moving a pile of bricks by hand along a chain or providing a theatrical or orchestral performance (one bad individual effort spoils the whole effect.)

Most doing the duty is essential to the survival of all after a natural disaster. The alliances we call societies and the firm, normally not in danger of collapse, are threatened if there is a natural disaster. In these highly unusual circumstances, alliance-supportive activities, greater cooperativeness and self-sacrifice become an important public good.

In normal periods when threats are small, what social control mechanisms that are in place are sufficient and there is no need for exceptional behaviour and self-sacrifice.

Everyone has an interest in the continuity of the economic and social fabric and the survival of their employers in times of adversity. Individual contributions to these national and local public goods become much more decisive after a natural disaster.

In normal times people behave in a conventionally cooperative way because individually they find it profitable to do so. There is some slippage around the edges and there are social control mechanisms to deter illegal conduct and supply public goods.

As the threat to the social and economic fabric grows after a natural disaster, eventually the social and economic balance may hang by a hair. When this is so, any single person can reason that his own behaviour might be the social alliance’s weakest link. International military and political alliances also rise and fall on this weakest link basis.

Taxman – The Beatles

07 Sep 2016 Leave a comment

in applied price theory, public economics Tags: superstar wages, taxation and labour supply, The Beatles

% employees working more than 50 hours per week, 2014 OECD area

15 Aug 2016 6 Comments

in labour economics, labour supply, occupational choice, public economics Tags: hours worked, taxation and labour supply

Not coincidentally, countries with high marginal income tax rates have low levels of long hours worked per week.

Data extracted on 14 Aug 2016 01:52 UTC (GMT) from OECD.Stat; Data does not include the self-employed.

Socialism DOES Work | Jeremy Corbyn | Oxford Union

03 Aug 2016 Leave a comment

in applied price theory, economic history, economics, income redistribution, Public Choice, public economics, Rawls and Nozick Tags: British politics, Leftover Left

Do the Rich Pay Their Fair Share?

13 Jul 2016 Leave a comment

in politics - USA, public economics Tags: envy, superstars, taxation and entrepreneurship, taxation and investment, top 1%, top 10%

.@TheAusInstitute will EU finance ministers welcome 15% British company tax?

04 Jul 2016 Leave a comment

in applied price theory, politics - Australia, public economics

If the Australian Institute’s analysis of company tax cuts is to be believed, European Union member states must be rubbing their hands in glee at the extra tax revenue that will flow to them because of Britain’s plans to cut its company tax rate to 15%.

Their analysis is a company tax cut in Australia, or in this case Britain, will simply mean more taxes will be paid in the home country of the foreign investing owned company when it repatriates dividends.

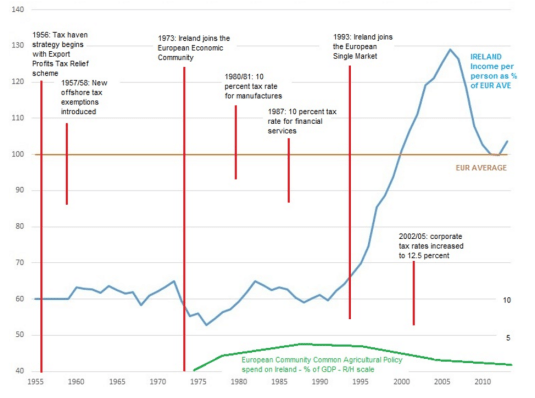

Ireland was relentlessly bullied over its 12.5% company tax rates by the rest of the European Union. Facts speaks louder than words and the Australia Institute economic analysis.

You do wonder why losing finance ministers complain about lowering of company taxes as a race to the bottom. They are complaining because they are losing foreign investment to lower company tax jurisdictions.

.@MaxRashbrooke kills case for #UBI @GrantRobertson1 @JordNZ

03 Jul 2016 Leave a comment

in applied welfare economics, politics - New Zealand, poverty and inequality, Public Choice, public economics

Rashbrooke in the snap-shot quote describes the massive new taxes to fund a universal basic income as a policy shift for which middle New Zealand must be prepared properly over many years. But the purpose of these great big new taxes is to ensure that those with whom the modern welfare state was designed to protect our left no worse off, not better off, just as good as they were under the previous regime of social insurance. Why take that journey when you can target their poverty directly to the current welfare state?

Source: Is Labour really going to deliver a UBI? – Inequality: A New Zealand Conversation.

The West Wing: “In This White House” (2000)

28 Jun 2016 Leave a comment

in development economics, economics of media and culture, growth disasters, growth miracles, health economics, Public Choice, public economics Tags: drug prices, intellectual monopolies, patents and copyrights

@TheAusInstitute @BenOquist wrong to say every economist agrees on effects of company tax cut

24 Jun 2016 Leave a comment

in applied price theory, politics - Australia, politics - USA, public economics

Source: Company tax cut won’t help Australian economy, jobs – Crikey.

It is unfortunate that the Australia Institute today misspoke when it claimed that every economist agrees that the effect of a company tax rate cut is small.

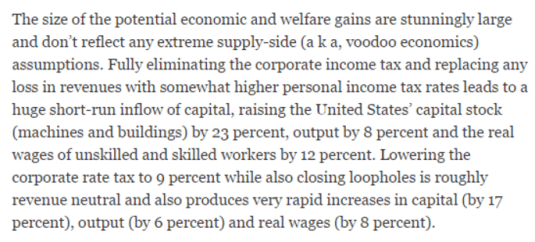

The top economists in the field of public economics disagree. Their views are freely available on the Internet. They are easiest to find by googling the words abolish the corporate tax. Optimal rate of tax on capital is zero are other good words to Google.

Source: Abolish the Corporate Income Tax – The New York Times.

It has been well known for decades of the optimal rate of tax on income from capital and from capital gains are zero. The Australia Institute has joined with Paul Krugman in not reporting this as Greg Mankiw explains

Paul Krugman responds to my post about a recent column of his. He is correct that not all economists agree that low capital taxation is desirable; he appropriately cites Diamond and Saez, who are on the high-capital-tax side of this debate. FYI, here is another recent paper, written in part as a response to Diamond and Saez, which finds that optimal rates of capital taxation, while positive, are quite low.

But that is not really the issue. If Paul had said “reasonable economists disagree, here are the arguments, and here is why I tend to favor one side rather than the other” I would not have objected.

Instead, in his original column, he wrote as if there were no reasonable arguments for the policy pursued by the Bush administration, and he attributed the most vile motives to those who advanced the policy.

This episode illustrates a fundamental difference between Paul and me. I try not to assume the worst in other people, just because they disagree with me.

Taxes on incomes from capital should be much lower because capital migrates from high-tax to low-tax locations, reducing capital-to-labour ratios in the higher company tax countries.

The low-tax on income from capital countries experience higher capital-to-labour ratios, a higher marginal product of labour, and higher wages. Robert Lucas described abolishing taxes on income from capital is one of the few genuinely free lunches out there in applied welfare economics.

Mankiw and Weinzierl “Dynamic Scoring: A Back-of-the-Envelope Guide,” Journal of Public Economics (September 2006): 1415-1433 argue that, in the long run, about 17% of a cut in individual income taxes is recouped through higher economic growth. For a cut in company taxes, their figure is 50%.

The Australia Institute manages to put itself in the contradictory position of saying a company tax rate just means more revenue for the IRS in the USA but Google, Facebook and other multinationals managed to avoid tax on a massive stale through tax havens. If the former is correct, their less company tax in Australia means more company tax paid in the USA means multinationals must be rather unsuccessful at avoiding tax through tax havens.

Multinationals are both avoiding company tax in Australia and offshore and paying it in full in the USA if Australia’s company taxes cut if the Australian Institute is to be believed today.

More than 50% of US corporate profits earned abroad are made in nations considered tax havens on.wsj.com/1h2Uitv http://t.co/6L8Hqislxd—

Nick Timiraos (@NickTimiraos) September 29, 2015

The Australia Institute obviously has not picked up on the relentless bullying that Ireland was subject to by the rest of the European Union over its 12.5% company tax.

The Irish company tax rate of 12.5% was initially on export profits. To finesse European Union member state complaints about that 12.5% company tax rate on discrimination grounds, the Irish government extended that low rate to all companies in 1995.

I am yet to see a minister of finance welcoming a company tax cut in a competing jurisdiction, rubbing his hands in anticipation of greater tax revenues on the foreign profits of multinationals that are headquartered in his country.

If there is an ounce of sense in what the Australia Institute said about foreign taxmen benefiting from low company taxes in Australia, high corporate tax rate countries such as Germany, France and the USA should welcome low company tax rates in destination countries for foreign investment originating in those countries but they do not.

Rather than seek tax harmonisation, high tax country should welcome low company taxes in competing investment destinations but they do not. Why is this so if the Australia Institute is making sense?

The Nordic countries follow optimal tax theory and have high but flat taxes on labour income, low taxes on business income and a high, broad-based consumption tax. That is the only way they can fund their welfare states.

The Nordics are alert to not killing the goose that laid the golden egg. Company taxes are relatively low in Scandinavian countries as compared to the USA so that businesses do not flee to other jurisdictions.

A large welfare state such as those in the Nordic countries require a significant amount of revenue, so the tax base in these countries must be broad. This also means higher taxes on consumption through the VAT or GST and higher taxes on middle-income taxpayers.

Business taxes are a less reliable source of revenue because of capital flight and disincentives to invest. Thus, the Nordics do not place above-average tax burdens on capital income and focus taxation on labour and consumption. All those nuances are lost if you are to believe the Australia Institute today.

Does abolishing bureaucracy save the #UBI? Avoid a great big new tax?

23 Jun 2016 Leave a comment

in applied welfare economics, income redistribution, politics - USA, poverty and inequality, public economics Tags: expressive voting, social insurance, universal basic income

Firing the entire welfare state bureaucracy does not save the day for a universal basic income as Robert Greenstein explains

Suppose UBI provided everyone with $10,000 a year. That would cost more than $3 trillion a year — and $30 trillion to $40 trillion over ten years.

This single-year figure equals more than three-fourths of the entire yearly federal budget — and double the entire budget outside Social Security, Medicare, defense, and interest payments. It’s also equal to close to 100 percent of all tax revenue the federal government collects…

Where would the money to finance such a large expenditure come from? That it would come mainly or entirely from new taxes isn’t plausible.

We’ll already need substantial new revenues in the coming decades to help keep Social Security and Medicare solvent and avoid large benefit cuts in them. We’ll need further tax increases to help repair a crumbling infrastructure that will otherwise impede economic growth. And if we want to create more opportunity and reduce racial and other barriers and inequities, we’ll also need to raise new revenues to invest more in areas like pre-school education, child care, college affordability, and revitalizing segregated inner-city communities.

A UBI that’s financed primarily by tax increases would require the American people to accept a level of taxation that vastly exceeds anything in U.S. history. It’s hard to imagine that such a UBI would advance very far, especially given the tax increases we’ll already need for Social Security, Medicare, infrastructure, and other needs.

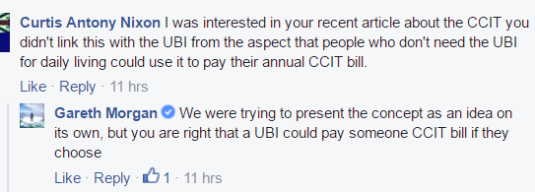

#Morganfoundation’s same #UBI of $11,000 per adult is now triple pledged

22 Jun 2016 Leave a comment

in applied welfare economics, politics - New Zealand, poverty and inequality, public economics

Before my two comments disappeared from Gareth Morgan’s Facebook page, I pointed out that his universal basic income of $11,000 per adult is as of last night at least triple pledged.

According to Gareth Morgan’s latest remark in the screenshot, people can use their universal basic income of $11,000 to pay their comprehensive capital tax bill. This new tax is proposed to fill the at least $10 billion gap in the funding of his universal basic income.

This is not possible because his universal basic income is already pledged to at least two other purposes that may use up a good part of the universal basic income of $11,000 per adult that he is proposing.

The first of these pledges is a by-product of adults under the age of 50 not being grandfathered in to the current level of generosity of New Zealand Superannuation – New Zealand’s universal old age pension.

Adults under the age of 50 under the Morgan Foundation’s universal basic income are expected to save part of their universal basic income. This saving is to make up for the $50 per week cut in New Zealand Superannuation when it is replaced by a universal basic income of $11,000 per adult. Gareth Morgan explains

Only people who are today under the age of 50 could be expected to retire under the UBI policy, the policy would not apply to existing superannuitants.

The key question is whether someone aged, say 40 today, would be better or worse off in retirement under the policy. And the answer is if they earn the average wage now, have an average house, they will tend to be neither better nor worse off.

For the 25 years prior to retirement they will receive the UBI on top of their wages. If they save a good portion of it they will have nest egg at retirement which they can use in retirement to supplement the UBI (which is more modest than today’s NZ Super).

In addition to this, the universal basic income makes those on a single parents benefit $150 a week worse off on the basic benefit that is not including lost accommodation supplements and additional child payments. The Morgan Foundation solution is to take part of the universal basic income of the other parent and give it to their children. Gareth Morgan explains again

It is totally feasible that the UBI of both parents could be required to be directed to support the children in the event of separation.

So in addition to the poor and ordinary families saving their universal basic income for as little as 15 years to making up for the $50 per week cut in support for old age pensioners, and the $150 plus cut in income support to single parents on a welfare benefit, the universal basic income also will be used to pay the comprehensive capital tax on the family home.

Somewhere buried in the universal basic income is it is the idea that it replaces existing welfare benefits. However, as most of the universal basic income has been pledged to other purposes such as saving for retirement, supporting children and paying the great big new tax in the family home, it will be very unwise to actually become unemployed, get sick, become a single parent or being invalid on the already meagre universal basic income as Geoff Simmons explains

With an unconditional basic income, most beneficiaries would be no better off than they are now (in fact sole parents would almost certainly receive a lower benefit).

There is a high risk that nothing will be left over from the Morgan foundation’s universal basic income to help you out when you fall in bad times because that universal basic income is already spoken for by your children, your retirement, and a capital tax bill.

Helping people out in times of misfortunes is the purpose of social insurance. The Morgan Foundation’s universal basic income fails this basic test set by Gareth Morgan

…let’s agree on what is a minimum income every adult should have in order to live a dignified life and then see what flows from that. We begin by specifying the income level below which we are not prepared to see anyone having to live.

At very best, and only very best, the Morgan Foundation’s universal basic income leaves some of those for whom social insurance was designed perhaps no worse. There are plenty of commonplace scenarios where individuals and families down on their luck are made much worse by a universal basic income replacing existing welfare benefits and plunged far deeper in poverty and hardship.

Recent Comments