Prime Minister Jim Hacker: “Well, of course we do what we can. There are many calls on the public purse: inner cities, schools, hospitals, kidney machines…”

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

27 Mar 2017 Leave a comment

in fiscal policy, politics - New Zealand, public economics, television Tags: sovereign wealth funds, Yes Prime Minister

Prime Minister Jim Hacker: “Well, of course we do what we can. There are many calls on the public purse: inner cities, schools, hospitals, kidney machines…”

27 Mar 2017 Leave a comment

in discrimination, gender, labour economics, politics - New Zealand Tags: gender wage gap, reversing gender gap, unconscious bias

26 Mar 2017 Leave a comment

26 Mar 2017 Leave a comment

25 Mar 2017 Leave a comment

in economic history, politics - New Zealand, poverty and inequality Tags: child poverty, family poverty, The Great Enrichment

According to Brian Perry, the the expert at the Ministry of Social Development writing in last year’s Social Report:

The primary measure is the proportion of people in households with equivalised disposable income net-of-housing-costs below a threshold set at 50 percent of the 2007 household disposable income median – and held fixed in real terms (the 2007 anchored or constant value measure, CV-07).

This measure shows whether the incomes of low-income households are rising or falling in real terms, irrespective of what is happening to the incomes of the rest of the population.

The two other measures use fully relative thresholds set at 50 and 60 percent of the current year’s household disposable income median net-of-housing-costs (REL 50/60). These measures reflect how low-income households are faring relative to middle-income households.

25 Mar 2017 Leave a comment

24 Mar 2017 Leave a comment

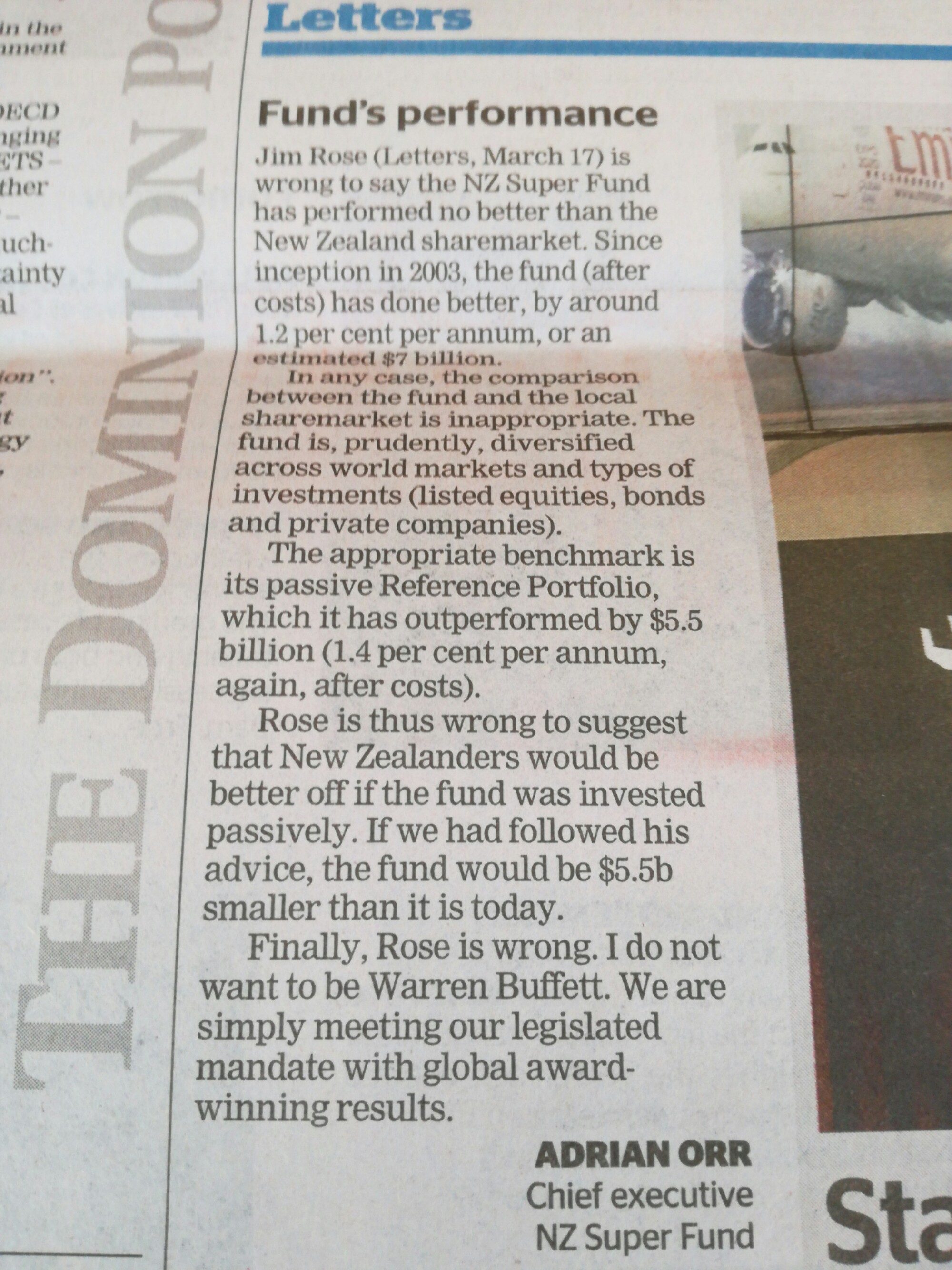

in financial economics, fiscal policy, politics - New Zealand, public economics Tags: active investing, efficient markets hypothesis, passive investing, sovereign wealth funds

There is always one. Liran Einav had to be the only economist out of 100 or so top American and European economists who disagreed with the proposition that:

In general, absent any inside information, an equity investor can expect to do better by choosing a well-diversified, low-cost index fund than by picking a few stocks.

The New Zealand Superannuation Fund’s policy of active investing has one supporter out of 100 surveyed by the Initiative for Global Markets. I suppose it is better than none.

Letter to @DomPost on @NZSuperfund performance @Taxpayersunion utopiayouarestandinginit.com/2017/03/18/let… https://t.co/wxo6F1zZn5—

Jim Rose (@JimRose69872629) March 18, 2017

The chief executive of the fund quibbles by claiming there is a 3rd way between active and passive investing but there is not as William Sharp explained in his timeless 1991 article, The Arithmetic of Active Management:

An active fund is a fund that is not a passive fund. If you do not own a balanced portfolio of every security in the market, you are an active investor.

The majority of the New Zealand Superannuation fund is passively invested but some of it is not. It is invested in dogs like KiwiBank, in Z service stations and even in some bad Portuguese loans.

23 Mar 2017 Leave a comment

There really is an issue on which economists are unanimous, a big issue to boot.

Source: Diversified Investing | IGM Forum.

Actively-managed mutual funds cannot earn excess returns over index funds because in aggregate they earn the same as index funds, less the difference in cost. This was proposed by Sharpe in his timeless 1991 article, The Arithmetic of Active Management.

Of course, certain definitions of the key terms are necessary. First a market must be selected — the stocks in the S&P 500, for example, or a set of “small” stocks. Then each investor who holds securities from the market must be classified as either active or passive.

- A passive investor always holds every security from the market, with each represented in the same manner as in the market. Thus if security X represents 3 per cent of the value of the securities in the market, a passive investor’s portfolio will have 3 per cent of its value invested in X. Equivalently, a passive manager will hold the same percentage of the total outstanding amount of each security in the market2.

- An active investor is one who is not passive. His or her portfolio will differ from that of the passive managers at some or all times. Because active managers usually act on perceptions of mispricing, and because such misperceptions change relatively frequently, such managers tend to trade fairly frequently — hence the term “active.”

… Properly measured, the average actively-managed dollar must underperform the average passively-managed dollar, net of costs. Empirical analyses that appear to refute this principle are guilty of improper measurement.

In 2008, Warren Buffett made a bet of $1 million with Protégé Partners LLC that, including fees, costs and expenses, an S&P 500 index fund would outperform a hand-picked portfolio of hedge funds over the 10 years ending December 31, 2017.

20 Mar 2017 Leave a comment

in fiscal policy, politics - New Zealand, public economics Tags: family tax credits

The last Labour Government so hated tax cuts that it would not call its family tax credit a family tax credit. For those on the minimum wage, it could increase your income by 1/3rd. Oddly enough, because of abatement rates of 22.5% after $36,000, two minimum wage earners do not get much at all.

19 Mar 2017 Leave a comment

19 Mar 2017 Leave a comment

in fiscal policy, macroeconomics, politics - New Zealand, public economics Tags: intergenerational equity, intergenerational justice, old age pensions, sovereign wealth funds

Pre-funding of New Zealand’s old age pension obligations requires contributions to the New Zealand Superannuation Fund now, higher taxes now in return for lower taxes later through the joys of compounding of the returns on the investments. If that is so, when the contributions are not made, the $3 billion in annual taxes should not be collected.

Source: Andrew Coleman, PAYGO vs SAYGO: Prefunding Government-provided Pensions, Motu Economics and Public Policy 26 Oct 2010.

There should be a separate New Zealand superannuation fund contribution levy that should lapse when contributions are suspended, as they were from 2009, and the pay-outs start after 2036? Otherwise, taxpayers will never see the promised lower taxes in the future. Never?

Source: Andrew Coleman Mandatory retirement income schemes, saving incentives, and KiwiSaver at http://www.treasury.govt.nz/publications/reviews-consultation/savingsworkinggroup/pdfs/swg-b-m-mris-24dec10.pdf

Constitutional political economy matters despite the reluctance of most who specialise in Social Security reform to think about that backend public choice risk. Unless there is iron-clad guarantee of lower taxes in the future, the whole deal about pre-funding superannuation pay-outs is a con.

That politicians can pass a law in 2003 to pre-fund old-age pensions 40 years hence and expect the politicians of 2036 and onwards to honour the deal with tax cuts is politically naive.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A History of the Alt-Right

Econ Prof at George Mason University, Economic Historian, Québécois

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Recent Comments