Anti-competitive mergers make little sense to me

04 Aug 2016 Leave a comment

in applied price theory, industrial organisation, survivor principle Tags: competition and monopoly, competition law, mergers and takeovers

There are two main arguments against mergers and acquisitions. The first of these is that they are paper shuffling with little in the way of cost advantages. The second is they allow the combined firm to raise its prices because it faces less competition.

I find these arguments to be in direct contradiction. Anti-competitive mergers must be high risk venture if there is little in the way of cost savings. Two previously efficient firm sizes are disturbed permanently in the hope of some ability to raise prices in the future without provoking too much new entry or expansion from the competitive fringe.

It is far better just to keep on colluding or just compete rather than risk permanently damaging the efficient operation of both firms.

Creative destruction in technology acquisitions

19 Oct 2015 Leave a comment

in economic history, entrepreneurship, industrial organisation, survivor principle Tags: creative destruction, entrepreneurial alertness, market for corporate control, mergers and takeovers

The 12 biggest #technology acquisitions of all time wef.ch/1QrO2b5 http://t.co/Dx0YTm8NpA—

World Economic Forum (@wef) October 15, 2015

How to show the emergence of a working super rich while attempting to argue they are a rentier class

28 May 2015 Leave a comment

in financial economics, industrial organisation, managerial economics, organisational economics, survivor principle, theory of the firm Tags: CEO pay, Leftover Left, leveraged buyouts, market for corporate control, mergers and takeovers, superstar wages, superstars, Twitter left

The Washington Centre for Equitable Growth in a review of Thomas Piketty accidentally contradicted their own arguments about the emergence of the top 0.1%. They quote Piketty:

on page 302 of his book that the rise in labour income “primarily reflects the advent of ‘supermanagers,’ that is, top executives of large firms who have managed to obtain extremely high, historically unprecedented compensation packages for their labour.”

according to the Washington Centre for Equitable Growth:

these supermanagers were being vastly overly compensated given their questionable contributions to productivity.

The Washington Centre for Equitable Growth then goes on the argue that in 1979, most of the top managers worked for large, publicly traded firms but by 2005 more were working in closely held firms.

Who are today’s supermanagers and why are they so wealthy? equitablegrowth.org/research/today… http://t.co/Ts2OkOUk5g—

Equitable Growth (@equitablegrowth) December 03, 2014

I wish to explore this point about the biggest gains in both percentage terms and magnitude were among privately held business professionals and they are vastly overcompensated relative to their productivity. The key to the argument as explained in a link to a Robert Solow article by the Washington Centre for Equitable Growth is:

Piketty is of course aware that executive pay at the very top is usually determined in a cosy way by boards of directors and compensation committees made up of people very like the executives they are paying.

Piketty is equally direct about the ability of top managers to set their own pay:

It is only reasonable to assume that people in a position to set their own salaries have a natural incentive to treat themselves generously or at the least to be rather optimistic in gauging their marginal productivity.

Emmanuel Saez is less coy:

…while standard economic models assume that pay reflects productivity, there are strong reasons to be sceptical, especially at the top of the income ladder where the actual economic contribution of managers working in complex organizations is particularly difficult to measure. In this scenario, top earners might be able partly to set their own pay by bargaining harder or influencing executive compensation committees.

When arguing that the optimal top income tax rate is 83%, Piketty, Saez, and Stantcheva push for that high top tax rate in part because top executives are more likely to bargain for higher pay when tax rates are lower and receive funds that might go elsewhere within the firm.

Emmanuel Saez and Gabriel Zucman explore the new wealth divide in the U.S. equitablegrowth.org/research/explo… http://t.co/WKJKAigAPN—

Equitable Growth (@equitablegrowth) October 24, 2014

The only comment I could find on the increasing number of privately held companies that pay top executives so well is frustration by the Washington Centre for Equitable Growth that it complicates statistical collection. No other analysis is undertaken.

Xavier Gabaix and Augustin Landier found back in 2008 that what a major company’s CEO earns is directly proportional to the size of the firm that they are responsible for running. Executive compensation closely track the evolution of average firm value. During 2007 – 2009, firm value decreased by 17%, and CEO pay by 28%. During 2009-2011, firm value increased by 19% and CEO pay by 22%. Xavier Gabaix and Augustin Landier also found that compensation for executives has risen with the market capitalization. From 1980 to 2003, the average value of the top 500 companies rose by a factor of six. Two commonly used indexes of chief executive compensation show close to a proportional six-fold matching increase.

What intrigued me about this casual reference to the great number of super managers employed by privately held firms is the argument that they have a cosy relationship with their board of directors immediately collapses. That argument about executive pay is usually in the context of the separation of ownership from control. In large publicly held companies the executives are subject to less scrutiny by shareholders as few of them have a large enough individual stake in the company to gain from the extra effort of monitoring their pay packages.

When the pay packages of top executives is questioned, it is always pointed out that there is an easy way to test for whether top executives cheat shareholders by overpaying themselves.

This simple test is comparing the pay of large private companies and public companies with a large or a few share holders with public companies with diffuse share holdings. Private equity typically also pay its top executives very well, even though the capacity to dupe public shareholders are not a factor.

Privately owned companies and public companies with a few large shareholders can easily keep track of the pay packages of the executives and the board of directors hired to monitor them. Private equity ownership have high pay-for-performance but also significant CEO co-investment.

The standard argument for excessive compensation for CEOs is free rider problems prevent shareholders from doing sufficient monitoring of executive compensation practices, and that the problems have been getting worse over time. For example, in a classic paper, Bebchuk and Fried (2004) argued that executive compensation is set by CEOs themselves rather than boards of directors on behalf of shareholders,

This argument does not apply to private companies with a few shareholders but they still offer large pay packages to their top executives. Companies, be they public or private that pay any employee more than they contribute risks takeover and loss of market share and failure through higher costs.

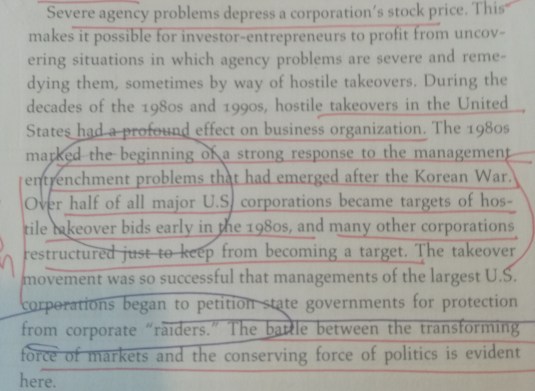

The burst of takeovers and leverage buyouts in the 1980s were partly driven by opportunities to profit from reducing corporate slack and downsizing flabby corporate headquarters of large publicly listed companies. Cleaning out the overpaid executives and overstaffing in the headquarters of large corporations was an express purpose of these takeovers and leveraged buyouts.

The response of the Left over Left of the day was support regulation to stop these mergers and takeovers rather than applauding them as giving lazy, overpaid top executives a kick up the backside and from the boot out the door. This regulation to make hostile takeovers more difficult undermined the market the corporate control rather than strengthened it as Michael Jensen explains:

This political activity is another example of special interests using the democratic political system to change the rules of the game to benefit themselves at the expense of society as a whole.

In this case, the special interests are top-level corporate managers and other groups who stand to lose from competition in the market for corporate control. The result will be a significant weakening of the corporation as an organizational form and a reduction in efficiency.

Central to the hypothesis of the Twitter Left of CEOs overpaying themselves is there is free cash within the business they pocket in pay rises, fringe benefits and lavished corporate headquarters rather than pay out in dividends or invest in profitable investments.

CEOs with high pay packages are now much more likely than 20 or 30 years ago to be employed in private companies where the shareholders have far greater opportunities to ensure they get value for money.

All modern theories of the focus in part or in full on reducing opportunistic behaviour, cheating and fraud in employment and commercial relationships. The market for corporate control, and mergers and takeovers realise large benefits from displacing underperforming manager teams. Premiums in hostile takeover offers historically exceed 30% on average. Acquiring-firm shareholders on average earn about 4% in hostile takeovers and roughly zero in mergers.

Another reason for high CEO pay in both public and private companies is CEOs tend to be more risk adverse than their shareholders. The shareholders in any one company has a diversified portfolio and protected by limited liability if the company fails because of a risky venture. Moreover, shareholders receive nothing in dividends if the company breaks even so they would prefer that managers pursue business ventures likely to do more than break even.

The agent principal conflict ears as long as the company breaks even, the CEO gets paid. Out of career concerns, a CEO does not want to be at the head of a company that fails because his re-employment prospects are quite grim. High-risk/high-reward ventures are less attractive to top executives because if they fail, their human capital that is specific to the failed company is worthless elsewhere.

To encourage CEOs to take risks, paying them were share options makes them more interested in risky ventures because their pay goes up in line with the risks they take which they would otherwise not take but for option being paid in options. Privately owned companies are well aware of this risk aversion among their chief executives which is why they pay them so well and often in share options and bonuses for taking risks.

The Washington Centre for Equitable Growth simply did not address the reasons for privately owned companies paying the top executives so well.

The incomes of executives, managers, financial professionals, and technology professionals who are in the top 0.1% is very sensitive to stock market fluctuations. This volatility in the pay of CEOs is inconsistent with the notion that their pay is linked to their ability to form cosy relationships with the boards of directors rather than with their performance.

These top 0.1% CEOs are working super rich whose fortunes rise and fall with the businesses they direct. Top CEOs are paid so much more because they direct the fortunes of large enterprises. In such cases, a small amount of extra talent is worth because the benefits of that small amount of extra talent are spread over such a large firm.

Recent Comments