Scott Freeman on the power of monetary policy

14 Dec 2018 Leave a comment

in business cycles, macroeconomics, monetary economics Tags: monetary policy

Scott Freeman on the money output correlation

02 Dec 2018 Leave a comment

in business cycles, macroeconomics, monetary economics Tags: monetary policy

Finn Kydland on the Great Recession

27 Nov 2018 1 Comment

in budget deficits, business cycles, economic growth, fiscal policy, great recession, macroeconomics, public economics Tags: monetary policy, taxation and entrepreneurship, taxation and investment, taxation and labour supply

Scott Freeman summarizes Lucas

16 Nov 2018 Leave a comment

in business cycles, economic growth, macroeconomics, monetary economics, Robert E. Lucas Tags: monetary policy

Scott Freeman on monetary policy as a stabilizing tool

15 Nov 2018 Leave a comment

in business cycles, economic growth, macroeconomics, monetary economics Tags: monetary policy

Central banks can’t raise interest rates so what chance of bankers’ cartel fixing interest rates

15 Nov 2018 Leave a comment

Scott Freeman on monetary policy neutrality

07 Nov 2018 Leave a comment

in applied price theory, business cycles, economic growth, macroeconomics, monetary economics Tags: monetary neutrality, monetary policy

Scott Freeman explains monetary neutrality

05 Nov 2018 Leave a comment

in applied price theory, business cycles, economic growth, macroeconomics, monetary economics Tags: monetary policy

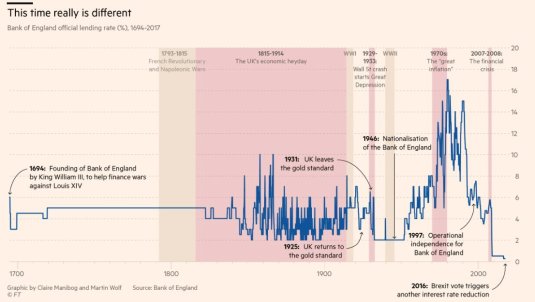

Stephen Williamson Monetary Policy Normalization: Origins of The Bank of England

23 May 2018 Leave a comment

in economic history, financial economics, macroeconomics, monetary economics Tags: monetary policy

Monetary Policy: The Best Case Scenario

11 Aug 2017 Leave a comment

in business cycles, economics, inflation targeting, macroeconomics, monetarism, monetary economics Tags: monetary policy

7. The New Deal and the Post War International Monetary System – Murray N Rothbard

16 Jul 2017 Leave a comment

in economic history, international economics, macroeconomics, monetary economics Tags: Austrian business cycle theory, monetary policy, regulatory capture

5 . The Inflationary Boom of the 1920s – Murray N Rothbard

15 Jul 2017 Leave a comment

in Austrian economics, business cycles, economic history, macroeconomics, monetary economics Tags: Austrian business cycle theory, monetary policy

Ed Prescott makes an excellent point in his last paragraph

16 May 2017 Leave a comment

Source: RBC Methodology and the Development of Aggregate Economic Theory Edward C. Prescott, Federal Reserve Bank of Minneapolis Staff Report 527 February 2016.

Milton Friedman is said to have mesmerised several countries with a flying visit!?

30 Sep 2016 Leave a comment

in business cycles, economic growth, macroeconomics, Milton Friedman, monetarism, monetary economics, politics - Australia Tags: central banks, conspiracy theories, lags on monetary policy, monetary policy, rules versus discretion, The fatal conceit, The pretense to knowledge

Milton Friedman visited Australia in 1975. He spoke with government officials and appeared on the TV show Monday Conference. Apparently, that was enough for him to take over Australian monetary policy setting for the foreseeable future.

When working at the next desk to the monetary policy section in the late 1980s, I heard not a word of Friedman’s Svengali influence:

- The market determined interest rates, not the reserve bank was the mantra for several years. Joan Robinson would be proud that her 1975 visit was still holding the reins.

- Monetary policy was targeting the current account. Read Edwards’ bio of Keating and his extracts from very Keynesian treasury briefings to Keating signed by David Morgan that reminded me of macro101.

See Ed Nelson’s (2005) Monetary Policy Neglect and the Great Inflation in Canada, Australia, and New Zealand who used contemporary news reports from 1970 to the early 1990s to uncover what was and was not ruling monetary policy. For example:

“As late as 1990, the governor of the Reserve Bank rejected central-bank inflation targeting as infeasible in Australia, and cited the need for other tools such as wages policy (AFR, October 18, 1990).”

Bernie Fraser was still sufficiently deprogrammed in 1993 to say that “…I am rather wary of inflation targets.” Easy to then announce one in the same speech when inflation was already 2-3%.

When as a commentator on a Treasury seminar paper in 1986, Peter Boxhall – fresh from the US and 1970s Chicago educated – suggested using monetary policy to reduce the inflation rate quickly to zero, David Morgan and Chris Higgins almost fell off their chairs. They had never heard of such radical ideas.

In their breathless protestations, neither were sufficiently in-tune with their Keynesian educations to remember the role of sticky wages or even the need for the monetary growth reductions to be gradual and, more importantly, credible as per Milton Freidman and as per Tom Sargent’s End of 4 big and two moderate inflations papers.

I was far too junior to point to this gap in their analytical memories about the role of sticky wages, and I was having far too much fun watching the intellectual cream of the Treasury senior management in full flight. At a much later meeting, another high flying deputy secretary was mystified as to why 18% mortgage rates were not reining in the current account in 1989.

Friedman’s Svengali influence did not extend to brainwashing in the monetarist creed that the lags on monetary policy were long and variable. The 1988 or 1989 budget papers put the lag on monetary policy at 1 year, which is short and rapier, if you ask me.

Recent Comments