Edward C. Prescott – How to Restore US Prosperity?

12 Jun 2019 Leave a comment

in budget deficits, business cycles, economic growth, Edward Prescott, fiscal policy, great recession, macroeconomics, monetary economics Tags: real business cycle theory

Entrevista con Edward Prescott

07 May 2019 Leave a comment

in business cycles, economic growth, Edward Prescott, fiscal policy, labour economics, labour supply, macroeconomics, monetary economics Tags: real business cycle theory

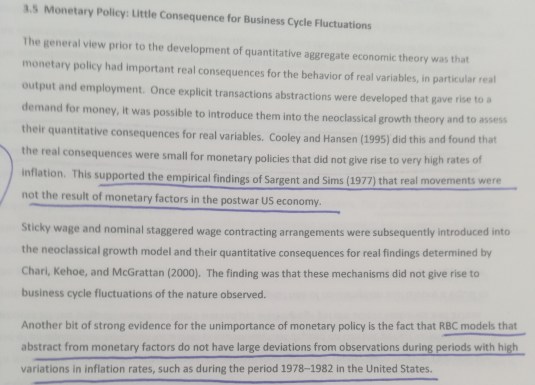

Policy responses to the business cycle require detailed information on the nature of the shocks

31 Mar 2019 Leave a comment

What are Real Shocks?

25 Nov 2018 Leave a comment

in business cycles, macroeconomics Tags: real business cycle theory

Bare bones RBC models and New Keynesian models on money and other drivers of the business cycle

17 Nov 2018 Leave a comment

in Edward Prescott Tags: New Keynesian macroeconomics, real business cycle theory

Edward Prescott on real business cycle theory as a genuine surprise

06 Nov 2018 Leave a comment

in business cycles, economic growth, Edward Prescott, macroeconomics, monetary economics Tags: real business cycle theory

What did Edward Prescott do when he found Keynesian macroeconomics wanting: double down on the old time religion or start again?

05 Nov 2018 Leave a comment

in budget deficits, business cycles, economic growth, Edward Prescott, fiscal policy, history of economic thought, macroeconomics, monetary economics, Robert E. Lucas Tags: Keynesian macroeconomics, real business cycle theory

The current state of the economy Edward Prescott 2012

26 Oct 2018 Leave a comment

in business cycles, Edward Prescott, fiscal policy, global financial crisis (GFC), great recession, macroeconomics Tags: real business cycle theory

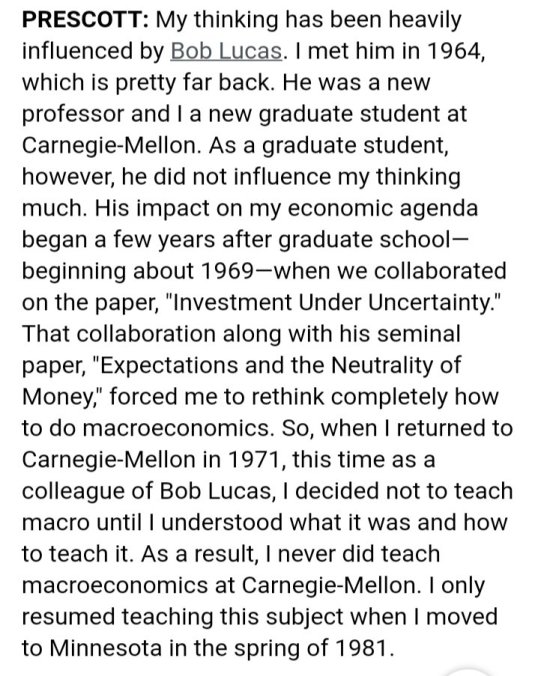

But did Ed Prescott consider whether a central bank can cause a recession if it really, really tried?

21 Sep 2018 Leave a comment

in business cycles, Edward Prescott, macroeconomics, monetary economics Tags: real business cycle theory

Ed Prescott makes an excellent point in his last paragraph

16 May 2017 Leave a comment

Source: RBC Methodology and the Development of Aggregate Economic Theory Edward C. Prescott, Federal Reserve Bank of Minneapolis Staff Report 527 February 2016.

Edward C Prescott on the EU, business cycles and European economic research

07 May 2017 Leave a comment

in budget deficits, business cycles, economic growth, Edward Prescott, macroeconomics Tags: real business cycle theory

Fiat Value in the theory of value – an ADEMU lecture by Edward C Prescott

06 May 2017 Leave a comment

Operations Research and The Revolution in Aggregate Economics – Edward Prescott 2012

18 Nov 2014 Leave a comment

in applied welfare economics, business cycles, economic growth, fiscal policy, global financial crisis (GFC), great depression, great recession, macroeconomics Tags: Edward Prescott, real business cycle theory

The extension of recursive methods to dynamic equilibrium modelling spawned a revolution in aggregate economics.

This revolution has resulted in aggregate economics becoming, like physics, a hard science and not exercises in storytelling.

Operations research played a major role in the development of practical methods to model dynamic aggregate economic phenomena and to predict the consequences of policy regimes.

Subsequently recursive methods were used to develop a quantitative theory of aggregate fluctuations and other aggregate phenomena.

The contribution of the random fortunes of large firms to business cycle volatility, or how a single, small, dirty pipe threatened to bring a nation to its knees

02 Aug 2014 Leave a comment

in business cycles, macroeconomics Tags: Fonterra, real business cycle theory

One contaminated pipe at a milk processing factory of New Zealand’s largest company, Fonterra, New Zealand’s largest company (7% of GDP) and largest exporter caused such a loss of brand-name value of the company that the New Zealand Treasury revised down its GDP forecasts for the year.

It is a little bit scary to wonder what kind of nation we live in when a single, small, dirty pipe threatens to bring the nation to its knees. That indeed was the fear when, over the weekend, Fonterra announced the contamination of a small amount of whey powder from a Waikato processing plant – Bank of New Zealand

This growth forecast revision after the milk contamination scandal, but turn out to be false reading, is a good example of how the random fortunes of individual large companies can have economy-wide implications and can even lead to recessions.

Figure 1: Sector’s concentration (Herfindahl Index) and sector’s contribution to aggregate volatility

Source: (Gabaix 2011).

There is growing evidence that idiosyncratic shocks to the fortunes of the 100 largest firms arising from changes in demand and cost conditions in their local and export markets combine to contribute about one-third of up-swings and downswings in U.S. output and employment (Gabaix 2011).

In an economy dominated by a few large firms, idiosyncratic shocks to large firms do not cancel out. The ups and downs in the individual fortunes of very large firms combine with firm-to-firm linkages to travel far beyond the firm and sector of origin (Gabaix 2011). These effects are likely to be stronger outside of the USA because it has a more diversified economy than most countries (Gabaix 2011).

Di Giovanni and Levchenko (2010) found that having fewer and less diversified firms and exports dominated by large firms helps to explain why small, more open economies such as New Zealand are more volatile. Fonterra accounts for 7 per cent of GDP and 20 per cent of overall exports. Drought is important to the New Zealand business cycle and agricultural exports (Buckle, Kim, Kirkham, McLellan and Sharma 2007).

As another example of the importance of a few large firms, Samsung and Hyundai account for 35 per cent of Korean exports and 22 per cent of Korean GDP.It would not be a good idea for the chief executives of those two Korean businesses to travel in the same car and have an accident.

Finland was monikered the one-firm economy because Nokia was responsible for 1/5th of Finnish economic growth, exports and company tax revenues for two decades. Nokia shares initially fell by 90 per cent in 2007 when Apple leap-frogged it with an iPhone that resembled a PC. The loss of one product development race imperilled the foundation of one-fifth of Finnish economic growth.

The literature on the contribution of large firms to business cycle volatility is a good examples of how the real business cycle theory is alive and well and is a progressive research programme.

Recent Comments