Business demographic statistics in New Zealand include companies with zero employees and calls them a firm.

Source: Statistics New Zealand.

Every definition of a firm that I have seen refers to a firm as a relationship between employers, employees and others. There is team production or some sort of nexus of contracts or dependent assets, something social.

The notion is that transactions that normally take place in the market are taken out of the market and take place within the firm. Most profoundly, as Ronald Coase explained in 1937 in his seminal work The Nature of the Firm is what needs to be explained is the existence of the firm, with its

distinguishing mark … [of] the supersession of the price mechanism.

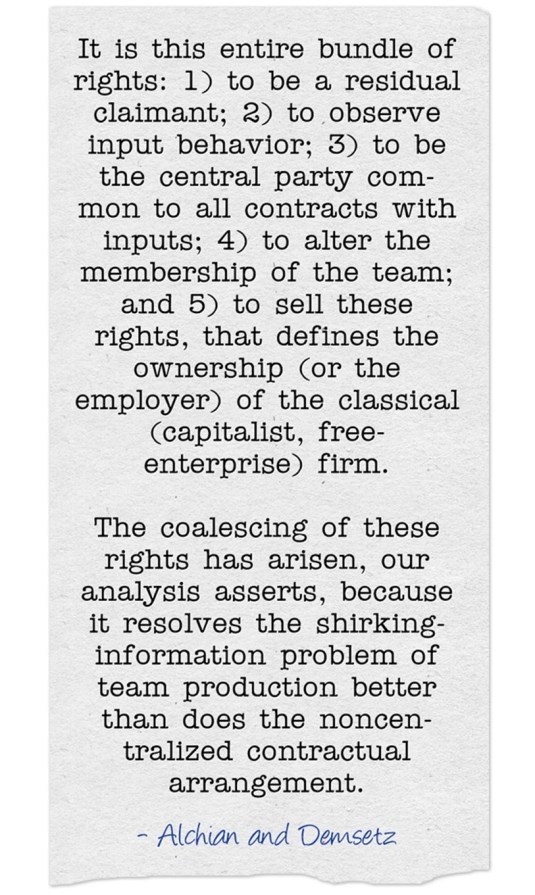

If there’s only one person in the firm, there is no one to transact with within the firm that the parties would normally have otherwise done in the market at arm’s length. There is no suppression of the price system, because all the dealings of the one person firm is with others. There are no transactions outside of the price system. As Barzel and Kochin explain when contrasting Ronald Coase’s theory of the firm with that of Alchian and Demsetz:

Even though they offer an alternative to Coase’s theory of the firm, their firm, nevertheless, is fundamentally a transaction cost phenomenon – it arises in response to the costs associated with measuring and policing various inputs and outputs.

Doug Allen, along with Eugene Fama, argue that all economic organisations are designed to maximise the gains from trade net of transaction costs. Other forms of organisation, forms of organisation that do not maximise the gains from trade net of transaction costs as well would not survive in market competition.

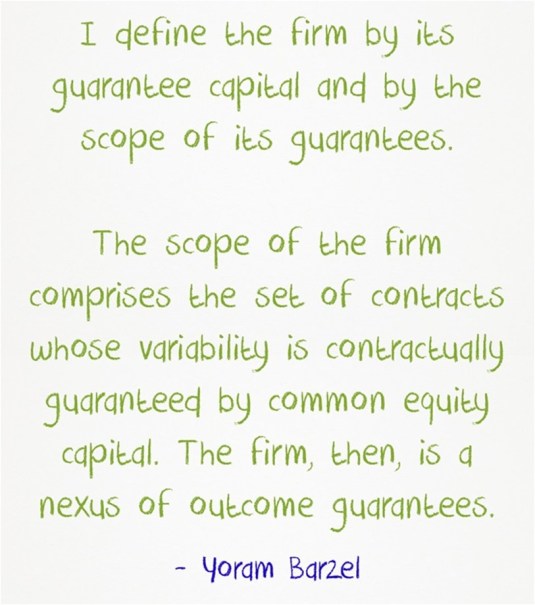

Transaction costs are defined by Allen as the costs of establishing and maintaining property rights. Yoram Barzel defines (economic) property rights (in this paper, p. 394) as:

… an individual’s net valuation, in expected terms, of the ability to directly consume the services of the asset, or to consume it indirectly through exchange. A key word is ability: The definition is concerned not with what people are legally entitled to do but with what they believe they can do.

A property right, according to Alchian (1965, 1987) and Cheung (1969), is essentially the ability to enjoy a piece of property, but this ability to benefit from an asset or commodity, either directly, or indirectly through market exchange, is seldom unhindered. Eugene Fama observed that:

The striking insight of Alchian and Demsetz (1972) and Jensen and Meckling (1976) is in viewing the firm as a set of contracts among factors of production. In effect, the firm is viewed as a team whose members act from self-interest but realize that their destinies depend to some extent on the survival of the team in its competition with other teams.

If the firm consists only of the owner, there is no internal constraints on the establishment and maintenance of property rights because no one else is in the firm to cause any conflict. There is no nexus of contracts between different suppliers of production inputs whose destinies depend on the ability of them as a team to survive in competition with other teams.

Whatever constraints might arise about the ability of the owner to actually exercise property rights, none of these constraints arise internally to the firm because of the presence of employees or partners.

If there are no employees, if the firm only consist of the owner, the purpose of the firm, which is to make the incentives of workers compatible with those of owners is lost.

Firms, to be a firm, must have employees. If not employees, there must be at least more than one party involved, such as in a partnership.

Firms exist because it is cheaper to organize inputs within a firm than buy and sell in many different markets. This buying and selling requires a continual negotiation, renegotiation, enforcement and monitoring of contracts at arm’s length with independent suppliers of inputs. Barzel stressed this enforcement of property rights in an unpublished paper:

I hypothesize that the firm is organized for the express purpose of creating rights that are more economically enforced by non-state rather than by state means.

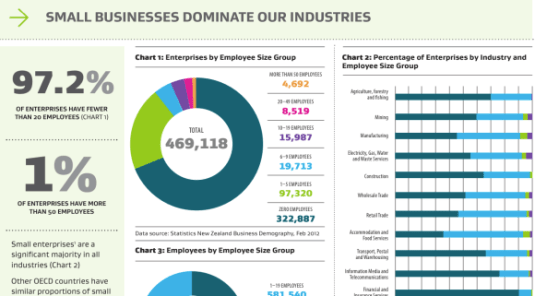

Many of these firms with zero employees in the New Zealand business demographic statistics, a classification that accounts for over 60% of all firms in New Zealand, are shelf companies or property investment companies.

There is no measuring and policing of inputs and outputs in a firm that has no employees and only an owner. These entities are not firms. They meet none of the criteria for a firm in the economics of industrial organisation.

This failure to distinguish between a firm and other forms of organisation leads the Minister of Economic Development to say unfortunate things such as:

97 per cent of enterprises in New Zealand are small businesses and have fewer than 20 employees.

Two thirds of that 97% of enterprises has no employees. Any discussion that pretends to know that there are too many or too few small and large firms in New Zealand should not be confused with other forms of organisation of capital that have nothing to do with the topic at hand, which is usually workplace productivity and entrepreneurial competence.

Many of these zero employee firms are not even economic organisations. They are legal mechanisms for exercising legal property rights. Including these property rights in business demographic statistics on business organisations is confusing.

Recent Comments