via DNA Sequencing Costs.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

14 Mar 2015 Leave a comment

in entrepreneurship, health economics Tags: creative destruction, innovation, Moore's law, The Great Enrichment, The Great Escape

via DNA Sequencing Costs.

13 Mar 2015 Leave a comment

in applied price theory, Austrian economics, behavioural economics, comparative institutional analysis, entrepreneurship, industrial organisation, survivor principle Tags: efficient markets hypothesis, entrepreneurial alertness, Paul Samuelson

via Samuelson vs. Friedman, David Henderson | EconLog | Library of Economics and Liberty and An Interview With Paul Samuelson, Part One — The Atlantic.

06 Mar 2015 Leave a comment

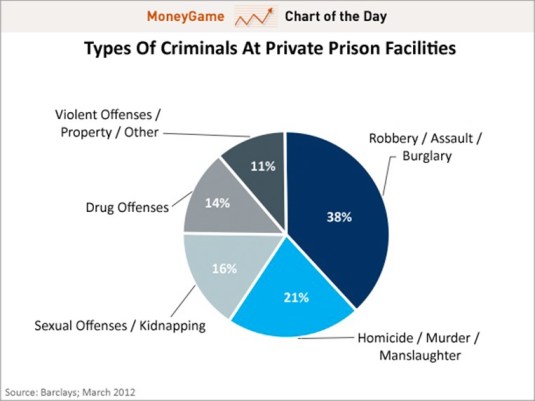

in economics of crime, entrepreneurship, law and economics, organisational economics, politics - New Zealand, politics - USA Tags: do gooders, law and order, prisons

I was listening to a radio show the other day on the introduction of close circuit television into New Zealand prisons that were to be monitored by both male and female guards. This is regarded as an indignity by some because these new close circuit cameras would be in showers and toilets.

The initial commentators on the radio programme immediately said they had watched plenty of TV programs where people were shanked in the showers.

The close circuit television was for the safety of prisoners. Close circuit cameras in all parts of prisons made prisons a safer place and that was that. It was the price of safety, especially for prisoners vulnerable to intimidation and sexual assault.

Greg Newbold, a New Zealand criminologist and an ex-prisoner in itself, then came on air to criticise the introduction of close circuit televisions in showers and other intimate areas such as toilets as an indignity on prisoners. Prisoners have a right to intimate privacy in his view. He said only 12 prisoners had been murdered in the New Zealand prisons since 1979.

Only 12 murders is 12 murders too many. Every one of those murders would have been subject of outrage about the failure of the prison administration from the bleeding hearts brigade.

The most interesting thing that Greg Newbold said on the radio was about how these close circuit television systems first emerged in prisons, initially in the USA.

Close circuit television systems will put throughout prisons initially in private prisons to avoid being sued for wrongful death and injury. The private prisons introduced this rather obvious security measure to reduce liability in the civil courts.

Public prisons are supposedly a safer place for prisoners to be if you listen to the bleeding hearts brigade and the Left over Left. Pubic prisons but never got around introducing what seems to me to be a rather basic security measure in confined areas of prisons. Close circuit television systems would protect both inmates and guards.

The different incentives facing public and hybrid prisons, in this case, exposure to litigation, is an illustration of the superior efficiency of private prisons.

Private prisons did something because it affects the bottom line. One way to reduce liability for deaths and injuries is prison security measures that reduce the number of deaths and injuries in prisons.

More importantly, private prisons have unforgiving critics in the form of the bleeding hearts brigade and Left over Left. No one on the Left will defend or protect a prison that is private from closure out of a knee-jerk defence of the public sector, and in particular, public-sector unions.

Oddly enough the only prison that the Left over Left want to close in New Zealand is the highest performing prison, Mt Eden, which happens to be privately run.

The main problem with private prisons is contracting over quality where it is difficult to define quality and measure performance against quality standards specified in a contract as Andrew Shleifer explains:

…critics of privatization often argue that private contractors would cut quality in the process of cutting costs because contracts do not adequately guard against this possibility

Privatisation for many government services is simply an extension of the make-or-buy decision. Every firm faces a make-or-buy decision – should the firm buy a production input from outside suppliers or should it make what it needs itself with existing or additional internal resources?

As any industry grows, there is more room for more specialised producers to supply to firms of all sizes at a lower cost than in-house production (Stigler 1951, 1987; Levy 1984). As an example, all with the largest firms intermittently hire legal, accounting and many other professional skills from specialists.

By contracting-out to these more specialised and niche suppliers, firms can enjoy all available economies of scale in production unless its needs are unique or the firm has some special competency in producing the input in-house (Lindsay and Maloney 1996; Shughart 1997; Roberts 2004). Firms in most industries capture all available economies of scale at relatively small sizes after which they have a long region of production where their marginal cost of further increases in production are constant (Stigler 1958; Lucas 1978; Barzel and Kochin 1992; Shughart 1997).

Put simply, an entrepreneur makes what he or she cannot buy at the quality preferred through contracting in market:

The case for in-house provision is generally stronger when non-contractible cost reductions have large deleterious effects on quality, when quality innovations are unimportant, and when corruption in government procurement is a severe problem. In contrast, the case for privatization is stronger when quality reducing cost reductions can be controlled through contract or competition, when quality innovations are important, and when patronage and powerful unions are a severe problem inside the government.

The way in which the market process dealt with chiselling on quality where quality reducing cost reductions where costly to control through contract or competition was the emergence of non-profit institutions. The competitive edge of these non-profit institutions was they had fewer incentives to dilute hard to measure qualities of the product transacted.

Any additional profits from this dilution of quality were not distributed to the owners because the non-profit organisation was either run by a charity or was owned mutually by the customers. The proceeds from cutting corners on quality could not be paid out to the owners in dividends because there were none.

Examples of non-profits competing successfully in the market are obvious, such as life insurance. Until recent decades, most life insurance companies were mutually owned by the policyholders. Life insurance companies were mutually owned as an assurance that no one could run off with the money by paying high dividends to the owners before policyholders died many years after they have paid their premiums.

Most private universities are run as non-profit institutions even when they are set up by private developers with profits in mind. The private university itself is owned by a charity with esteemed persons on the board to assure quality and probity. The active involvement of alumni is encouraged as a further guard of the future quality of the University from which they graduated. The private developers make their profit on the surrounding land as the university grows and prospers. Land grant universities in the USA may have operated this way.

Other examples of the emergence of non-profit institutions to assure quality in a competitive market are private schools, private hospitals, and private day care centres where concerns about the private provision of a quality service arise, with or without justification. Andrew Shleifer again:

…entrepreneurial not-for-profit firms can be more efficient than either the government or the for-profit private suppliers precisely … where soft incentives are desirable, and competitive and reputational mechanisms do not soften the incentives of private suppliers [to dilute quality].

Of course, any proper analysis must compare like with like and compare the dismal record of public prisons date in terms of prisoner and prison guard safety and preventing escapes with any scandals in the private prison systems. Few do that.

04 Mar 2015 7 Comments

in applied price theory, Austrian economics, entrepreneurship, F.A. Hayek, George Stigler, human capital, industrial organisation, job search and matching, labour economics, law and economics, Ludwig von Mises, politics - New Zealand, survivor principle Tags: Armen Alchian, employment law, employment protection laws, entrepreneurial alertness, France, Israel Kirzner, The fatal conceit, The pretence to knowledge

As discussed yesterday, if the Employment Court had its way, New Zealand case law under the Employment Relations Act regarding redundancies and layoffs would be as job destroying as those in France.

The Employment Court’s war against jobs goes back more than 20 years. To 1991 and G N Hale & Son Ltd v Wellington etc Caretakers etc IUW where the Court held that a redundancy to be justifiable under law it must be ‘unavoidable’, as in redundancies could only arise where the employer’s capacity for business survival was threatened.

The Court of Appeal slapped that down and affirm the right of the employer to manage his business in no uncertain terms:

…this Court must now make it clear that an employer is entitled to make his business more efficient, as for example by automation, abandonment of unprofitable activities, re-organisation or other cost-saving steps, no matter whether or not the business would otherwise go to the wall…

The personal grievance provisions … should not be treated as derogating from the rights of employers to make management decisions genuinely on such grounds. Nor could it be right for the Labour Court to substitute its own opinion as to the wisdom or the expediency of the employer’s decision.

When a dismissal is based on redundancy, it is the good faith of that basis and the fairness of the procedure followed that may fall to be examined on a complaint of unjustifiable dismissal

… the Court and the grievance committees cannot properly be concerned with an examination of the employer’s accounts except in so far as it bears on the true reason for dismissal.

The Employment Court could only inquire as to the genuineness of the employer’s decision and the procedures adopted. The Court could not substitute their views on management decisions. No second-guessing.

In Brake v Grace Team Accounting Ltd, the Employment Court found its way back into second-guessing employer’s decisions about how to manage their business. The figures used by the employer to decide that a redundancy was required were in error. The employer miscalculated.

The Employment Court had previously held in Rittson-Thomas T/A Totara Hills Farm v Hamish Davidson that the statutory test of what a fair and reasonable employer could have done in all the circumstances applies to the substantive reasoning for redundancies. Some enquiry into the employer’s substantive decision is required to establish that a hypothetical fair and reasonable employer could also make the same decision in all of the circumstances.

Subsequently in Brake v Grace Team Accounting Ltd, the Employment Court found that the actions by the employer were “not what a fair and reasonable employer would have done in all the circumstances” and “failed to discharge the burden of showing that the plaintiff’s dismissal for redundancy was justified”.

The Court found that the redundancy was “a genuine, but mistaken, dismissal”, but it still found that the dismissal was substantively unjustified. That is a major new development. Mistaken dismissals that are genuine are unlawful and grounds for compensation under the employment law.

The case was appealed where the issues were whether the correct test had been applied. The Court of Appeal, in a sad day for employers, job creation and the unemployed, found that the Employment Court was within its rights to do what it did and applied the statutory tests correctly:

GTA acted precipitously and did not exercise proper care in its evaluation of its business situation and it made its decision about Ms Brake’s redundancy on a false premise.

So it never turned its mind to what its proper business needs were but rather proceeded to evaluate its options based on incorrect information. We can see no error in the finding by the Employment Court that a fair and reasonable employer would not do this.

The test is now that fair and reasonable employers in New Zealand do not make mistakes. A much greater burden is now laid upon employers to show that not only that redundancies are justified, but they have made careful calculations and no mistakes.

No more seat of your pants entrepreneurship in New Zealand. No more entrepreneurial hunches – the essence of entrepreneurship is acting on hunches and other judgements that are incapable of being articulated to others and about which there is mighty disagreement in many cases. As Lavoie (1991) states:

…most acts of entrepreneurship are not like an isolated individual finding things on beaches; they require efforts of the creative imagination, skillful judgments of future costs and revenue possibilities, and an ability to read the significance of complex social situations.

The essence of entrepreneurship is your hunches are better than the next guy’s and you survive in competition by backing that hunch often to the consternation of the crowd. As Mises explains:

[Economics] also calls entrepreneurs those who are especially eager to profit from adjusting production to the expected changes in conditions, those who have more initiative, more venturesomeness, and a quicker eye than the crowd, the pushing and promoting pioneers of economic improvement…

The entrepreneurial idea that carries on and brings profits is precisely that idea which did not occur to the majority… The prize goes only to those dissenters who do not let themselves be misled by the errors accepted by the multitude

In many cases, those entrepreneurial hunches are sorted, sifted and selected on the basis of trial and error in the marketplace. Central to Hayek’s conception of the meaning of competition is it is a process of trial and error with many errors:

Although the result would, of course, within fairly wide margins be indeterminate, the market would still bring about a set of prices at which each commodity sold just cheap enough to outbid its potential close substitutes — and this in itself is no small thing when we consider the insurmountable difficulties of discovering even such a system of prices by any other method except that of trial and error in the market, with the individual participants gradually learning the relevant circumstances.

Remember Hayek’s conception of competition as a discovery procedure where prices and production emerge through the clash of entrepreneurial judgements and competitive rivalry:

…competition is important only because and insofar as its outcomes are unpredictable and on the whole different from those that anyone would have been able to consciously strive for; and that its salutary effects must manifest themselves by frustrating certain intentions and disappointing certain expectations

Errors are no longer permitted in the New Zealand labour market by the Employment Court. The Court has outlawed error in redundancy decisions.

This is despite the fact that the conception by Kirzner of the market process is that it is an error correction procedure without rival and a central role of entrepreneurial alertness is to correct errors in pricing and production:

It is important to notice the role played in this process of market discovery by pure entrepreneurial profit. Pure profit opportunities emerge continually as errors are made by market participants in a changing world. The inevitably fleeting character of these opportunities arises from the powerful market tendency for entrepreneurs to notice, exploit, and then eliminate these pure price differentials.

The paradox of pure profit opportunities is precisely that they are at the same time both continually emerging and yet continually disappearing. It is this incessant process of the creation and the destruction of opportunities for pure profit that makes up the discovery procedure of the market. It is this process that keeps entrepreneurs reasonably abreast of changes in consumer preferences, in available technologies, and in resource availabilities.

Rothbard made similar arguments about the centrality of discrepancies and error in entrepreneurship:

The capitalist-entrepreneur buys factors or factor services in the present; his product must be sold in the future. He is always on the alert, then, for discrepancies, for areas where he can earn more than the going rate of interest.

In Frank Knight’s conception of profit, there were temporary profits that arise from the correction of error:

In the theory of competition, all adjustments “tend” to be made correctly, through the correction of errors on the basis of experience, and pure profit accordingly tends to be temporary.

The Employment Court misunderstands the market process as a process of error correction. Those errors are identified through entrepreneurial alertness and trial and error. These errors are both of over-optimism and over-pessimism as Kirzner explains:

Errors of over-pessimism are those in which superior opportunities have been overlooked. They manifest themselves in the emergence of more than one price for a product which these resources can create. They generate pure profit opportunities which attract entrepreneurs who, by grasping them, correct these over-pessimistic errors.

The other kind of error, error due to over-optimism, has a different source and plays a different role in the entrepreneurial discovery process. Over-optimistic error occurs when a market participant expects to be able to complete a plan which cannot, in fact, be completed.

A considerable part of entrepreneurial alertness arises from the business opportunities created by sheer ignorance and pure error as Kirzner explains:

What distinguishes discovery (relevant to hitherto unknown profit opportunities) from successful search (relevant to the deliberate production of information which one knew one had lacked) is that the former (unlike the latter) involves that surprise which accompanies the realization that one had overlooked something in fact readily available. (“It was under my very nose!”)

The market process is a selection procedure where the more efficient survive for reasons that may be unknown to the entrepreneurs directly concerned as well as to observers and officious judges. Alchian pointed out the evolutionary struggle for survival in the face of market competition ensured that only the profit maximising firms survived:

The surviving firms may not know why they are successful, but they have survived and will keep surviving until overtaken by a better rival. All business needs to know is a practice is successful.

One method of organising production and supplying to the market will supplant another when it can supply at a lower price (Marshall 1920, Stigler 1958). Gary Becker (1962) argued that firms cannot survive for long in the market with inferior product and production methods regardless of what their motives are. They will not cover their costs.

The more efficient sized firms are the firm sizes that are currently expanding their market shares in the face of competition; the less efficient sized are those firms that are currently losing market share (Stigler 1958; Alchian 1950; Demsetz 1973, 1976). Business vitality and capacity for growth and innovation are only weakly related to cost conditions and often depends on many factors that are subtle and difficult to observe (Stigler 1958, 1987). The Employment Court pretends to know better than the outcome of the competitive struggle in the market for survival.

The Employment Court also believes employers have something akin to academic tenure. In 2010, the Court found that an employee’s redundancy was unjustified because the employer did not offer redeployment and there is no requirement that the right of the redeployment be written into the employment agreement (Wang v Hamilton Multicultural Services Trust). The particulars of this case were quite interesting:

In the case at hand, the Employment Court held that the employer was obliged to look for alternatives to making the employee redundant. Given that he would be able to perform the new finance manager position with some up-skilling, the employer should have offered him the position rather than simply inviting him to apply for it.

The notion that an employee through training can quickly increase their marginal productivity by 50% to fill a more senior role contradicts the modern labour economics of human capital. A 50% salary increase through a bit of training would imply extraordinary annual returns on other forms of on-the-job training and formal education as well as the training at hand in the Employment Court case.

I would very much like to be in the position where I can get a 50% salary increase after a bit of training. As I recall, I required about 5-10 years of on-the-job human capital acquisition before my starting salary as a graduate was 50% higher through promotion and transfers.

In summary, the Employment Court stands apart from the modern labour economics of human capital and job search and matching as well as the modern theory of entrepreneurial alertness, and the market as a discovery procedure and an error correction mechanism. The Employment Court has fallen for both the pretence to knowledge and the fatal conceit.

03 Mar 2015 Leave a comment

in energy economics, entrepreneurship, environmental economics, environmentalism, global warming Tags: carbon neutral economy, China, climate alarmism, global warming, solar energy

02 Mar 2015 Leave a comment

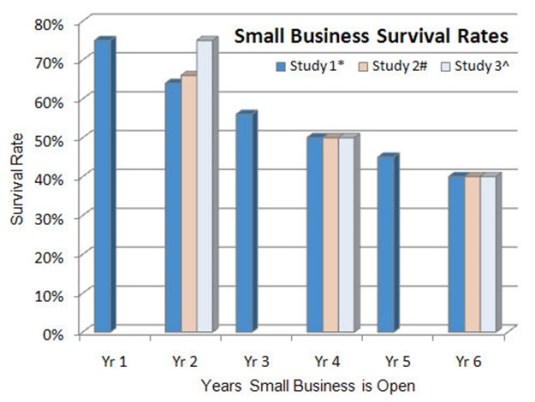

in economic history, entrepreneurship, survivor principle

HT: Do nine out of 10 new businesses fail, as Rand Paul claims? – The Washington Post.

For venture capital start-ups, about three or 4 out of 10 fail; three or 4 out of 10 return the original investment, with the rest offering a substantial profit.

24 Feb 2015 Leave a comment

in entrepreneurship, financial economics Tags: active investing, efficient markets hypothesis, entrepreneurial alertness, indexed linked investing, passive investing

23 Feb 2015 Leave a comment

in economics of religion, entrepreneurship Tags: entrepreneurial alertness, hoaxers, spoofs

20 Feb 2015 Leave a comment

in economics of bureaucracy, entrepreneurship, financial economics, politics - New Zealand Tags: active investing, corruption, euro crisis, Index of Economic Freedom, junk bonds, passive investing, Portugal, risk diversification, state owned enterprises

A Portuguese bank on the verge of collapse – what were they thinking?

That would have been the response of many newspaper readers this morning upon learning the New Zealand Superannuation Fund has lost nearly $200 million in taxpayers’ cash on a "risk-free" loan it provided to Lisbon-based Banco Espirito Santo (BES) on July 3.

The loan – part of a US$784 million credit package US investment bank Goldman Sachs put together through its Oak Finance vehicle – was made exactly one month before Portugal’s central bank broke up BES and split the country’s biggest lender into two, with one part holding the good assets and the toxic assets placed in the other.

Unfortunately, the Oak Finance loan is now stranded in the so-called "bad bank" following a retrospective law change by the Bank of Portugal.

Christopher Adams: What were they thinking? – Business – NZ Herald News.

This is what the 2015 index of Economic Freedom has to say about Portugal on the rule of law:

In 2013, the OECD expressed concern over Portugal’s reluctance to crack down on foreign bribery, particularly in regard to its former colonies Brazil, Angola, and Mozambique.

Since 2001, Portugal had officially acknowledged only 15 bribery allegations, and there had been no prosecutions. The judiciary is constitutionally independent, but staff shortages and inefficiency contribute to a considerable backlog of pending trials.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A History of the Alt-Right

Econ Prof at George Mason University, Economic Historian, Québécois

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Recent Comments