Knowledge, ignorance and equilibrium in the market process – Israel Kirzner

27 Aug 2014 Leave a comment

What is the precariat?

24 Aug 2014 Leave a comment

in applied price theory, applied welfare economics, comparative institutional analysis, constitutional political economy, development economics, entrepreneurship, growth disasters, growth miracles, income redistribution, rentseeking, technological progress, Uncategorized Tags: Leftover Left, precariat, The Great Act, The Great Enrichment, The withering away the proletariat

With the withering away of the proletariat because of the great enrichment, the Left over Left coined the word precariat.

The precariat is a social class formed by people suffering from precarity: a condition of existence without predictability or security, affecting material or psychological welfare as well as being a member of a proletariat class of industrial workers who lack their own means of production and hence sell their labour to live. Specifically, it is applied to the condition of lack of job security, in other words intermittent employment or underemployment and the resultant precarious existence. The term is a portmanteau obtained by merging precarious with proletariat.

Very similar to the Karl Marx’s Lumpenproletariat: the layer of the working class that is unlikely ever to achieve class consciousness and is therefore lost to socially useful production, of no use to the revolutionary struggle, and perhaps even an impediment to the realization of a classless society.

One of the drawbacks of the precariat is they are inconveniently happier than Left over Left are willing to give them credit. For example, a lot of women in part-time jobs are happier than those in full-time jobs because of the greater worklife balance. Casual and seasonal jobs pay more too.

0

Henry Hazlitt on wise bureaucrats and farsighted politicians

21 Aug 2014 Leave a comment

in applied price theory, comparative institutional analysis, entrepreneurship, liberalism, Public Choice, rentseeking, survivor principle Tags: fatal conceit, Henry Hazlitt, pretence to knowledge

Should everyone get a trophy in sports or just the winners

21 Aug 2014 Leave a comment

in comparative institutional analysis, entrepreneurship, liberalism Tags: distributive justice, entitlement theory of justice, expressive voting, just deserts, The mirage of social justice

via 57 Percent of Americans Say Only Kids Who Win Should Get Trophies – Reason-Rupe Surveys : Reason.com.

“Trapped” in Rental Contracts | Organizations and Markets

17 Aug 2014 Leave a comment

in applied price theory, Armen Alchian, comparative institutional analysis, entrepreneurship, industrial organisation, Ronald Coase, survivor principle, theory of the firm Tags: long-term contracts, mutual dependency, relationship dependent assets, transaction costs, vertical integration

![]()

- Mercedes and BMW drivers trapped in lease contracts, rather than buying their cars with cash or credit

- Individuals trapped in wage and salary contracts, rather than raising the capital, arranging the inputs, and bearing the uncertainties to be sole proprietors

- Companies trapped in outsourcing agreements, rather than owning all upstream and downstream production processes directly, as vertically integrated firms

- Vacationers trapped in resort hotels, rather than owning their own vacation condos or timeshares

- Readers trapped by downloading and reading books on their Kindles, essentially “renting” them from Amazon, rather than buying physical books

- Movie fans trapped in DVD rental agreements with Netflix, rather than owning massive DVD libraries

via “Trapped” in Rental Contracts | Organizations and Markets.

Marvellously simple explanation of the beauty and power of the market process

15 Aug 2014 Leave a comment

Atomic Tests Were a Tourist Draw in 1950s Las Vegas – entrepreneurial alterness alert

10 Aug 2014 Leave a comment

in entrepreneurship, environmentalism, health and safety, market efficiency, survivor principle Tags: entreprunerial alterness, times have changed

Over 1000 tests from 1951 onwards.

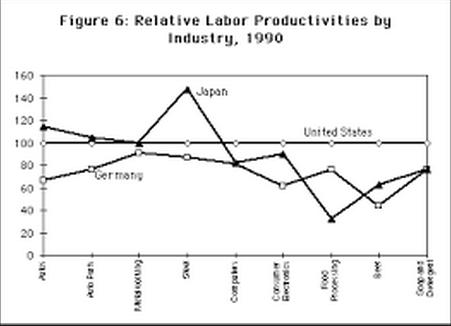

The puzzlingly large cross country differences in sector labour productivity

02 Aug 2014 Leave a comment

in applied price theory, entrepreneurship, macroeconomics Tags: barriers to riches, Britain, France, Germany, Japan, relative labour productivity, USA

There are large productivity differences between the global industrial leaders at the industry level. In a 1993 McKinsey’s study, large differences were uncovered in value added per worker between the USA, Japan, France, the UK and Germany across individual industries, by a factor of three in some cases (Prescott and Parente 2000, 2005).

- The USA competes with Japan for productivity leadership in many manufacturing industries.

- The Japanese services sector productivity can be as little as a one-third of that of the USA. Japanese labour productivity is almost twice Germany’s in producing automobiles and is better that Germany by a large margin for many other manufactured goods.

- The USA is uniformly more productive in services sector labour productivity. For example, British, French and German telecom workers were 38 to 56 per cent as productive as their American counter-parts.

Figure 1: Relative Value Added Per Worker: Germany, Japan, and the United States Manufacturer’s Industries

| Industry | Japan | Germany |

| Automobiles | 116 | 66 |

| Automobile Parts | 124 | 76 |

| Metal Working | 119 | 100 |

| Steel | 145 | 100 |

| Computer | 95 | 89 |

| Consumer Electronics | 115 | 62 |

| Food | 33 | 76 |

| Beer | 69 | 44 |

| Soap and Detergent | 94 | 76 |

Differences in the access to the global pool of useful knowledge cannot explain such large productivity differences at the sector and the individual industry levels between the USA, Japan, France, the UK and Germany and between these three European neighbours. The stock of useful technological knowledge does not vary that much across these countries (Prescott and Parente 2000, 2005). These countries produce and are the markets for the majority of that knowledge.

Figure 2: Relative Value Added Per Worker – service industries

| Industry | Japan | Germany | U.K. | France |

| Retailing | 44 | 96 | 82 | 69 |

| Telecommunications | 66 | 50 | 38 | 56 |

| Banking | – | 68 | 64 | – |

Lags in technology diffusion cannot be important. The USA, Japan, France, the UK, and Germany define the global technological frontier.

Differences in the skills of the individual worker or in the total stock of human capital of all workers in a country cannot explain these differences in value added per worker. The USA, Japan, France, the UK and Germany all have relatively well-educated, experienced and tested labour forces. For example, the 1993 McKinsey’s study inquired into the education and skills levels of Japanese and German steel workers. Comparably skilled German steel workers were half as productive as their Japanese counterparts (Prescott and Parente 2000, 2005).

What differ between these countries at the glob technological frontier is the amount of the global pool of useful productive of knowledge that is used and as work practices. Ford Europe failed to adopt Japanese just-in-time production, but Ford U.S.A. has adopted it. In the beer industry, much of the high technology machinery in Japan and U.S. is manufactured in Germany but German breweries fail to use these more productive technologies. The less productive airline sector in Europe vis-à-vis the United States is the result of over-staffing.

Can One Enviropreneur Save an Endangered Species? See for Yourself | Learn Liberty

01 Aug 2014 Leave a comment

in entrepreneurship, environmental economics, law and economics, property rights Tags: endangered species, enviropreneurs

Who Routinely Trounces the U.S. Stock Market? Try 2 Out of 2,862 Funds – NYTimes.com

30 Jul 2014 Leave a comment

in entrepreneurship, financial economics, survivor principle Tags: active investing, efficient markets hypothesis, indexed linked investing, passive investing, stock picking

For the three years ended March 2014, 14.10% of large-cap funds, 16.32% of mid-cap funds and 25.00% of small-cap funds maintained a top-half ranking over three consecutive 12-month periods. Random expectations would suggest a rate of 25%.

After five years, two funds are still beating the market in each of the last five years.The rest of fallen by the wayside.

via Who Routinely Trounces the Stock Market? Try 2 Out of 2,862 Funds – NYTimes.com

Recent Comments