via Six Things Technology Has Made Insanely Cheap – Bloomberg Business.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

08 May 2015 1 Comment

in entrepreneurship, technological progress Tags: creative destruction, entrepreneurial alertness, living standards, mismeasurement of prosperity, Moore's law, The Great Enrichment, The Great Fact

08 May 2015 Leave a comment

#Dailychart: In 2015 consumers will spend more time online than watching TV econ.st/1EU7g5Q http://t.co/pqKNum7CU5—

The Economist (@EconBizFin) May 05, 2015

07 May 2015 1 Comment

in business cycles, economic growth, economic history, entrepreneurship, global financial crisis (GFC), great depression, macroeconomics Tags: British disease, British economy, Celtic Tiger, Ireland, prosperity and depression, sick man of Europe

Figure 1: Real GDP per British and Irish aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1955-2013

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

Figure 2 detrends British real GDP growth since 1955 by 1.9% and Irish real GDP growth by 3.6%. The US real GDP growth in the 20th century is used as the measure of the global technological frontier growing at trend rate of 1.9% in the 20th century. The Irish economy is more complicated story because its growth rate in figure 2 was detrended at a rate of 3.6% because it was catching up from a very low base. Trend GDP growth per working age Irish for 1960-73 was 3.6 per cent (Ahearne et al. 2006).

Figure 2: Real GDP per British and Irish aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1.9 per cent detrended UK, 3.6% detrended Ireland, 1955-2013

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

A flat line in figure 2 indicates growth at 1.9% for that year. A rising line in figure 2 means above-trend growth; a falling line means below trend growth for that year.

In the 1950s, Britain was growing quickly that the Prime Minister of the time campaigned on the slogan you never had it so good.

By the 1970s, and two spells of labour governments, Britain was the sick man of Europe culminating with the Winter of Discontent of 1978–1979. What happened? The British disease resulted in a 10% drop in output relative to trend in the 1970s, which counts as a depression – see figure 2 .

Prescott’s definition of a depression is when the economy is significantly below trend, the economy is in a depression. A great depression is a depression that is deep, rapid and enduring:

The British disease in the 1970s bordered on a depression. There was then a strong recovery through the early-1980s with above trend growth from the early 1980s until 2006 with one recession in between in 1990. So much for the curse of Thatchernomics?

Figure 1 suggests a steady economic course in Ireland until the 1990s with a growth explosion growth with the Irish converged on British living standards up until the global financial crisis.

Figure 2 shows the power of detrending GDP growth and why Ireland was known as the sick man of Europe in the 1970s and 1980s with unemployment as high as 18% and mass migration again. The Irish population did not grow for about 60 years from 1926 because of mass migration.

Figure 2 shows that real GDP growth per working age Irish dropped below its 3.6 per cent trend for nearly 20 years from 1974 , but more than bounced back after 1992. The deepest trough was 18 per cent below trend and the final trough was in 1992 – see Figure 2.

The deviation from trend economic growth made the Irish depression from 1973 to 1992 comparable in depth and length to the 1930s depressions (Ahearne et al. 2006).

The Irish depression of 1973 to 1992 can be attributed to large increases in taxes and government expenditure and reduced productivity (Ahearne et al. 2006). There were two oil price shocks in the 1970s and many suspect Irish policy choices from 1973 to 1987.

There were three fiscal approaches: an aggressive fiscal expansion from 1977; tax-and-spend from 1981; and aggressive fiscal cuts from 1987 onwards. In the early 1980s, Irish CPI inflation at 21 per cent, public sector borrowing reached 20 per cent of GNP.

To rein in budget deficits, taxes as a share of GNP rose by 10 percentage points in seven years. The unemployment rate reached 17 per cent despite a surge in emigration. The rising tax burden raised wage demands, worsening unemployment. Government debt grew on some measures to 130 per cent of GNP in 1986 (Honohan and Walsh 2002).

From 1992, Ireland rebounded to resume catching-up with the USA. The Celtic Tiger was a recovery from a depression that was preceded by large cuts in taxes and government spending from the late 1980s (Ahearne et al. 2006). Others reach similar conclusions but avoid the depression word. Fortin (2002, p. 13) labelled Irish public finances in the 1970s and to the mid-1980s as a ‘black hole’.

Fortin (2002) and Honohan and Walsh (2002) disentangle the Irish recovery into a long-term productivity boom that had dated from the 1950s and 1960s, and a sudden short-term output and employment boom since 1993 following the late 1980s fiscal and monetary reforms.

Honohan and Walsh (2002) wrote of belated income and productivity convergence. The delay in income and productivity convergence came from poor Irish economic and fiscal policies in the 1970s and 1980s.

This was after economic reforms in the late 1950s and the 1960s that started a process of rapid productivity convergence after decades of stagnation and mass emigration; Ireland’s population was the same in 1926 and 1971. During the 1950s, up to 10 per cent of the Irish population migrated in 10 years.

In the 1990s, many foreign investors started invested in Ireland as an export platform into the EU to take advantage of a 12.5 per cent company tax rate on trading profits. Between 1985 and 2001, the top Irish income tax rate fell from 65 to 42 per cent, the standard company tax from 50 to 16 per cent and the capital gains tax rate from 60 to 20 per cent (Honohan and Walsh 2002).

What happened after the onset of the global financial crisis in Ireland and the UK are for a future blog posts.

06 May 2015 Leave a comment

in economics of media and culture, entrepreneurship, industrial organisation, survivor principle, technological progress Tags: creative destruction, entrepreneurial alertness, PCs

"The march of technology"-Abrash

1980 4MHz computer: $6000

2015 TitanX: $1000

30 years & 1,000,000,000X more powerful http://t.co/zTexe8d259—

Darshan Shankar (@DShankar) March 26, 2015

Abrash demonstrating how quickly tech has evolved over time #f8 #VR http://t.co/TymEpfyHwv—

Mashable (@mashable) March 26, 2015

05 May 2015 1 Comment

in Austrian economics, entrepreneurship, Marxist economics, politics - New Zealand Tags: schools, state owned enterprises

At least one Labour MP must have watched the other channel when the Berlin Wall fell. How else could Chris Hipkins, MP ever think that government provision is cheaper because they don’t have to make a profit? OK, he was a teenager when the Berlin Wall fell, but even teenagers watch the headline news or pick up the gist of the headlines from friends.

The tidiest of all Marxist arguments, the saddest of all Marxist arguments is government operation of businesses is cheaper because they don’t have to make a profit. At least we were spared the cliché “people not profits”.

Leaving to one side that government school buildings are built by private contractors to the Ministry of Education, let’s focus on whether government businesses will be cheaper because they don’t have to make a profit.

No cheap shots about how the portfolio of state owned enterprises are worth $30 billion returned a profit of $20 million to New Zealand taxpayers last year or of the inherent flaws of government ownership:

On the free market, in short, the consumer is king, and any business firm that wants to make profits and avoid losses tries its best to serve the consumer as efficiently and at as low a cost as possible.

In a government operation, in contrast, everything changes. Inherent in all government operation is a grave and fatal split between service and payment, between the providing of a service and the payment for receiving it.

The government bureau does not get its income as does the private firm, from serving the consumer well or from consumer purchases of its products exceeding its costs of operation.

No, the government bureau acquires its income from mulcting the long-suffering taxpayer. Its operations therefore become inefficient, and costs zoom, since government bureaus need not worry about losses or bankruptcy; they can make up their losses by additional extractions from the public till.

The accounting profit or loss of any firm combines two rather different concepts of profit:

Normal profit is simply at the cost of raising capital from investors. This capital can be borrowed in the form of a loan or can be equity.

Chris Hipkins, MP concedes a need to borrow capital when he talks about government typically having lower costs to access capital in the screenshot above. Both private and public builders of schools will have to pay to access capital.

Economic profit is a far more complicated concept frequently misunderstood, especially by Marxists, the Left over Left and, of course, professional media commentators. As Mises explains:

If all people were to anticipate correctly the future state of the market, the entrepreneurs would neither earn any profits nor suffer any losses. They would have to buy the complementary factors of production at prices which would, already at the instant of the purchase, fully reflect the future prices of the products. No room would be left either for profit or for loss.

What makes profit emerge is the fact that the entrepreneur who judges the future prices of the products more correctly than other people do buys some or all of the factors of production at prices which, seen from the point of view of the future state of the market, are too low. Thus the total costs of production — including interest on the capital invested — lag behind the prices which the entrepreneur receives for the product. This difference is entrepreneurial profit.

Profits arise from the dynamism of the market and the ability of superior entrepreneur’s to anticipate the future better than others for which there is always only a temporary profit:

Profits are never normal. They appear only where there is a maladjustment, a divergence between actual production and production as it should be in order to utilize the available material and mental resources for the best possible satisfaction of the wishes of the public. They are the prize of those who remove this maladjustment; they disappear as soon as the maladjustment is entirely removed.

Frank Knight in Risk, Uncertainty, and Profit (1921) distinguished between interest on capital that is lend as either a loan or equity – long-run normal profits – and the short-run profits and losses earned by superior, or suffered by inferior entrepreneurs , respectively. This entrepreneurial superiority or inferiority flows from the ability to forecast the uncertain future. Those entrepreneurs “with superior knowledge and superior foresight,” wrote Frank Fetter, “are merchants, buying when they can in a cheaper and selling in a dearer capitalisation market, acting as the equalizers of rates and prices.”

Knight argued that entrepreneurs earn profits as a return for putting up with uncertainty and anticipating uncertainty faster than the rest. Many businesses are unprofitable because of rising costs or falling sales that were not anticipated. The Knightian concept is of the profit-seeking entrepreneur investing resources under uncertainty about market demand and costs in the future.

Alchian (1950) illustrated the unreliability of cost estimation with the range of bids made in government tendering processes. When contractors bid for the same project, these entrepreneurs routinely disagree over its likely cost by margins of 20 percent. These tenderers are predicting their own costs, about which they are knowledgeable, and they have an incentive to be truthful to win the initial tender.

Profits and losses, by rewarding and penalising the entrepreneurs who are not the quickest, ensures that only what consumers want is bought to the market as Henry Hazlett explains:

In a free economy, in which wages, costs, and prices are left to the free play of the competitive market, the prospect of profits decides what articles will be made, and in what quantities—and what articles will not be made at all.

If there is no profit in making an article, it is a sign that the labour and capital devoted to its production are misdirected: the value of the resources that must be used up in making the article is greater than the value of the article itself.

Profits arise as the reward for superior foresight into the future and innovation. Both of these concepts are not associated with government run businesses as Alfred Marshall explained:

A government could print a good edition of Shakespeare’s works, but it could not get them written.

As for Hipkins’ argument that governments can borrow at a cheaper rate than private firms, Bailey and Jensen (1972) said:

…we argue that efficient allocation of risk bearing is usually more difficult for government projects than it is for private ones. Therefore, if anything, the allowance for risk should be greater for government projects than it is for otherwise comparable private ones…

We find no support for the arguments in favor of using the government bond rate or any other such universally low rate for discounting costs and benefits of public projects.

We concur in Hirshleifer’s conclusion that a public project with given attributes (in terms of dispersion of possible future outcomes and of the covariance of these outcomes with those for existing portfolios) should he discounted with at least as high a rate as a similar private project.

This “same rate” should include the appropriate allowances for taxes and other distortions in private markets (as outlined by Harberger) as well as the appropriate allowances for risk, which we have outlined above.

Moreover, if private markets in risk are as “imperfect” as many have claimed, that merely tends to increase the rate that should be used, because the government is even less able to distribute risks than are these markets.

05 May 2015 Leave a comment

in economics of media and culture, entrepreneurship, financial economics, industrial organisation, survivor principle Tags: creative destruction, Facebook, Twitter

04 May 2015 Leave a comment

in entrepreneurship, industrial organisation, survivor principle Tags: creative destruction, entrepreneurial alertness, technological unemployment

Before alarm clocks were affordable, 'knocker-ups' were used to wake people early in the morning. UK, around 1900 http://t.co/wD24qR85Jg—

History Pics (@HistoryPixs) January 20, 2014

03 May 2015 2 Comments

in economic growth, economic history, entrepreneurship, macroeconomics, Public Choice, public economics Tags: British disease, British economy, Margaret Thatcher, poor man of Europe, Sweden, Swedosclerosis, taxation and the labour supply, welfare state

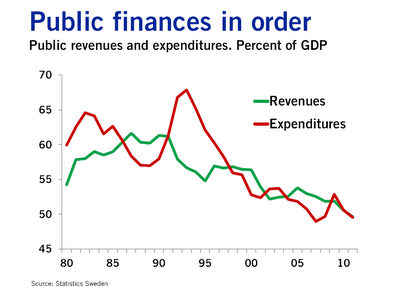

In 1970, Sweden was labelled as the closest thing we could get to Utopia. Both the welfare state and rapid economic growth – twice as fast as the USA for the previous 100 years.

Of course the welfare state was more of a recent invention. Assar Lindbeck has shown time and again in the Journal of Economic Literature and elsewhere that Sweden became a rich country before its highly generous welfare-state arrangements were created

Sweden moved toward a welfare state in the 1960s, when government spending was about equal to that in the United States – less that 30% of GDP.

Sweden could afford to expand its welfare state at the end of the era that Lindbeck labelled ‘the period of decentralization and small government’. Swedes in the 60s had the third-highest OECD per capita income, almost equal to the USA in the late 1960s, but higher levels of income inequality than the USA.

By the late 1980s, Swedish government spending had grown from 30% of gross domestic product to more than 60% of GDP. Swedish marginal income tax rates hit 65-75% for most full-time employees as compared to about 40% in 1960. What happened to the the Swedish economic miracle when the welfare state arrived?

In the 1950s, Britain was also growing quickly, so much so that the Prime Minister of the time campaigned on the slogan you never had it so good.

By the 1970s, and two spells of labour governments, Britain was the sick man of Europe culminating with the Winter of Discontent of 1978–1979. What happened?

Sweden and Britain in the mid-20th century are classic examples of Director’s Law of Public Expenditure. Once a country becomes rich because of capitalism, politicians look for ways to redistribute more of this new found wealth. What actually happened to the Swedish and British growth performance since 1950 relative to the USA as the welfare state grew?

Figure 1: Real GDP per Swede, British and American aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1950-2013, $US

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

Figure 1 is not all that informative other than to show that there is a period of time in which Sweden was catching up with the USA quite rapidly in the 1960s. That then stopped in the 1970s to the late 1980s. The rise of the Swedish welfare state managed to turn Sweden into the country that was catching up to be as rich as the USA to a country that was becoming as poor as Britain.

Figure 2: Real GDP per Swede, British and American aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, detrended, 1.9%, 1950-2013

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014, http://www.conference-board.org/economics

Figure 2 which detrends British and Swedish growth since 1950 by 1.9% is much more informative. The US is included as the measure of the global technological frontier growing at trend rate of 1.9% in the 20th century. A flat line indicates growth at 1.9% for that year. A rising line in figure 2 means above-trend growth; a falling line means below trend growth for that year. Figure 2 shows the USA growing more or less steadily for the entire post-war period. There were occasional ups and downs with no enduring departures from trend growth 1.9% until the onset of Obamanomics.

Figure 2 illustrates the volatility of Swedish post-war growth. There was rapid growth up until 1970 as the Swedes converged on the living standards of Americans. This growth dividend was then completely dissipated.

Swedosclerosis set in with a cumulative 20% drop against trend growth. The Swedish economy was in something of a depression between 1970 and 1990. Swedish economists named the subsequent economic stagnation Swedosclerosis:

Prescott’s definition of a depression is when the economy is significantly below trend, the economy is in a depression. A great depression is a depression that is deep, rapid and enduring:

There is no significant recovery during the period in the sense that there is no subperiod of a decade or longer in which the growth of output per working age person returns to rates of 2 percent or better.

The Swedish economy was not in a great depression between 1970 and 1990 but it meets some of the criteria for a depression but for the period of trend growth between1980 and 1986.

Between 1970 and 1980, output per working age Swede fell to 10% below trend. This happened again in the late 80s to the mid-90s to take Sweden 20% below trend over a period of 25 years.

Some of this lost ground was recovered after 1990 after tax and other reforms were implemented by a right-wing government. The Swedish economic reforms from after 1990 economic crisis and depression are an example of a political system converging onto more efficient modes of income redistribution as the deadweight losses of taxes on working and investing and subsidies for not working both grew.

The Swedish economy since 1950 experienced three quite distinct phases with clear structural breaks because of productivity shocks. There was rapid growth up until 1970; 20 years of decline – Swedosclerosis; then a rebound again under more liberal economic policies.

The sick man of Europe actually did better than Sweden over the decades since 1970. The British disease resulted in a 10% drop in output relative to trend in the 1970s, which counts as a depression.

There was then a strong recovery through the early-1980s with above trend growth from the early 1980s until 2006 with one recession in between in 1990. So much for the curse of Thatchernomics?

After falling behind for most of the post-war period, the UK had a better performance compared with other leading countries after the 1970s.

This continues to be true even when we include the Great Recession years post-2008. Part of this improvement was in the jobs market (that is, more people in work as a proportion of the working-age population), but another important aspect was improvements in productivity…

Contrary to what many commentators have been writing, UK performance since 1979 is still impressive even taking the crisis into consideration. Indeed, the increase in unemployment has been far more modest than we would have expected. The supply-side reforms were not an illusion.

John van Reenen goes on to explain what these supply-side reforms were:

These include increases in product-market competition through the withdrawal of industrial subsidies, a movement to effective competition in many privatised sectors with independent regulators, a strengthening of competition policy and our membership of the EU’s internal market.

There were also increases in labour-market flexibility through improving job search for those on benefits, reducing replacement rates, increasing in-work benefits and restricting union power.

And there was a sustained expansion of the higher-education system: the share of working-age adults with a university degree rose from 5% in 1980 to 14% in 1996 and 31% in 2011, a faster increase than in France, Germany or the US. The combination of these policies helped the UK to bridge the GDP-per-capita gap with other leading nations.

02 May 2015 Leave a comment

in entrepreneurship, health economics Tags: creative destruction, economics of smoking, entrepreneurial alertness

Per capita consumption of #tobacco in the United States via @USGA & @voxdotcom: plot.ly/~Dreamshot/1999 http://t.co/W5J1D2iJQN—

plotly (@plotlygraphs) April 21, 2015

01 May 2015 Leave a comment

in economics of crime, economics of regulation, entrepreneurship, environmentalism, law and economics, property rights Tags: black markets, economics of prohibition, endangered species, offsetting behaviour, or unintended consequences

Animated #Dailychart: Bear bile, rhino horn, tiger bone–how much do animal products cost? econ.st/1nfrFKf http://t.co/oG5HtZvzOL—

The Economist (@ECONdailycharts) July 23, 2014

30 Apr 2015 Leave a comment

in economic history, entrepreneurship, technological progress Tags: creative destruction, entrepreneurial alertness, technology diffusion, The Great Enrichment

via The 100-Year March of Technology in 1 Graph – The Atlantic and Guess What’s the Fastest-Adopted Gadget of the Last 50 Years – The Atlantic..

30 Apr 2015 Leave a comment

in economics of information, economics of media and culture, entrepreneurship, health economics Tags: charlatans, creative destruction, entrepreneurial alertness, market selection, quackery

30 Apr 2015 Leave a comment

in economic history, entrepreneurship Tags: entrepreneurial alertness, megaprojects

On the plus side, #1WTC is not the only large-scale construction project that ran over budget. forbes.com/sites/niallmcc… http://t.co/JYRwnE0M5T—

Statista (@StatistaCharts) December 10, 2014

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Scholarly commentary on law, economics, and more

Beatrice Cherrier's blog

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Why Evolution is True is a blog written by Jerry Coyne, centered on evolution and biology but also dealing with diverse topics like politics, culture, and cats.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

A rural perspective with a blue tint by Ele Ludemann

DPF's Kiwiblog - Fomenting Happy Mischief since 2003

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

The world's most viewed site on global warming and climate change

Tim Harding's writings on rationality, informal logic and skepticism

A window into Doc Freiberger's library

Let's examine hard decisions!

Commentary on monetary policy in the spirit of R. G. Hawtrey

Thoughts on public policy and the media

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Politics and the economy

A blog (primarily) on Canadian and Commonwealth political history and institutions

Reading between the lines, and underneath the hype.

Economics, and such stuff as dreams are made on

"The British constitution has always been puzzling, and always will be." --Queen Elizabeth II

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

WORLD WAR II, MUSIC, HISTORY, HOLOCAUST

Undisciplined scholar, recovering academic

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Res ipsa loquitur - The thing itself speaks

In Hume’s spirit, I will attempt to serve as an ambassador from my world of economics, and help in “finding topics of conversation fit for the entertainment of rational creatures.”

Researching the House of Commons, 1832-1868

Articles and research from the History of Parliament Trust

Reflections on books and art

Posts on the History of Law, Crime, and Justice

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Exploring the Monarchs of Europe

Cutting edge science you can dice with

Small Steps Toward A Much Better World

“We do not believe any group of men adequate enough or wise enough to operate without scrutiny or without criticism. We know that the only way to avoid error is to detect it, that the only way to detect it is to be free to inquire. We know that in secrecy error undetected will flourish and subvert”. - J Robert Oppenheimer.

The truth about the great wind power fraud - we're not here to debate the wind industry, we're here to destroy it.

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Economics, public policy, monetary policy, financial regulation, with a New Zealand perspective

Celebrating humanity's flourishing through the spread of capitalism and the rule of law

Restraining Government in America and Around the World

Recent Comments