How Expert Are Expert Stock Pickers?

25 Aug 2017 Leave a comment

in applied price theory, entrepreneurship, financial economics

Is ethical investing a dud? @NZSuperFund @JordNZ @EricCrampton @GreenpeaceNZ

17 Aug 2017 1 Comment

in defence economics, environmental economics, financial economics, health economics, politics - New Zealand

Imagine how much more would be available for funding old age pensioners, schools, hospitals and kidney machines if you have a passively invested portfolio rather than an ethically invested portfolio. Virtue signalling is not free. Ethical investing significantly underperforms the market even if done by the best of the passive investing funds such as Vanguard.

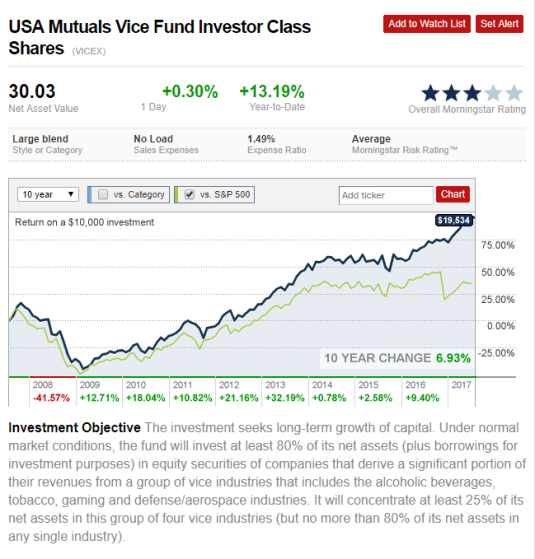

How is the vice fund going? @NZSuperFund @JordNZ @EricCrampton @GreenpeaceNZ

17 Aug 2017 Leave a comment

in defence economics, economics of regulation, entrepreneurship, financial economics

Ethical investing is back in the news again; time to look at the investment performance of a fund specialising in investing in the sin industries.

Conclusive evidence that Amazon takeover is pro-competitive

27 Jun 2017 Leave a comment

in applied price theory, financial economics, industrial organisation, law and economics Tags: antitrust economics, competition law

.@GreenpeaceNZ @OxfamNZ should invest their Kiwsaver in renewable energy? Step-up!

13 Jun 2017 Leave a comment

in energy economics, environmentalism, financial economics

Average Income of Top 10% in 2010

31 May 2017 Leave a comment

in financial economics, human capital, labour economics, labour supply, occupational choice Tags: superstars, top 1%

Amazon vs. Walmart market capitalisation

24 May 2017 Leave a comment

in entrepreneurship, financial economics Tags: creative destruction

Speaking of the @NZSuperfund -@TaxpayersUnion

24 Apr 2017 Leave a comment

in economic history, financial economics Tags: active investing, passive investing

#Hedgefunds don’t recruit from @NZSuperFund!? @VernonSmall @TaxpayersUnion

30 Mar 2017 Leave a comment

in financial economics, personnel economics, politics - New Zealand Tags: active investing, efficient markets hypothesis, hedge funds, passive investing, sovereign wealth funds

If the NZ Super Fund was any good at investing, rival investment houses will soon poach their staff to learn the secrets behind their self-proclaimed ability to beat the market.

Investment staff turnover at the NZ Super Fund is so low that you suspect they are overpaid.

Source: New Zealand Superannuation Fund, information released under the Official Information Act.

The Fund has no information on whether hedge funds head-hunt their staff but I think it might have got out in gossip if someone had a spectacular pay rise at their next job.

Sharp ratios of @NZSuperFund since inception @TaxpayerUnion

28 Mar 2017 Leave a comment

in financial economics, fiscal policy, politics - New Zealand, public economics Tags: sharp ratios, sovereign wealth funds

The Sharp ratio describes how much excess return you are receiving for the extra volatility that you endure for holding a riskier asset. If manager A generates a return of 15% while manager B generates a return of 12%, it would appear that manager A is a better performer. But if manager A took much larger risks than manager B, manager B may be a better risk-adjusted return.

The Sharpe Ratio such as those below of the NZ Superannuation Fund can be used to compare two funds on how much risk a fund had to bear to earn excess return over the risk-free rate.

Source:New Zealand Superannuation Fund response to Official Information Act request.

Business Cycles – Edward C. Prescott

25 Mar 2017 Leave a comment

in business cycles, development economics, economic growth, economic history, financial economics, fiscal policy, macroeconomics Tags: Edward Prescott, real business cycles

98% top US economists disagree @NZSuperFund strategy @VernonSmall @JordNZ

24 Mar 2017 Leave a comment

in financial economics, fiscal policy, politics - New Zealand, public economics Tags: active investing, efficient markets hypothesis, passive investing, sovereign wealth funds

There is always one. Liran Einav had to be the only economist out of 100 or so top American and European economists who disagreed with the proposition that:

In general, absent any inside information, an equity investor can expect to do better by choosing a well-diversified, low-cost index fund than by picking a few stocks.

The New Zealand Superannuation Fund’s policy of active investing has one supporter out of 100 surveyed by the Initiative for Global Markets. I suppose it is better than none.

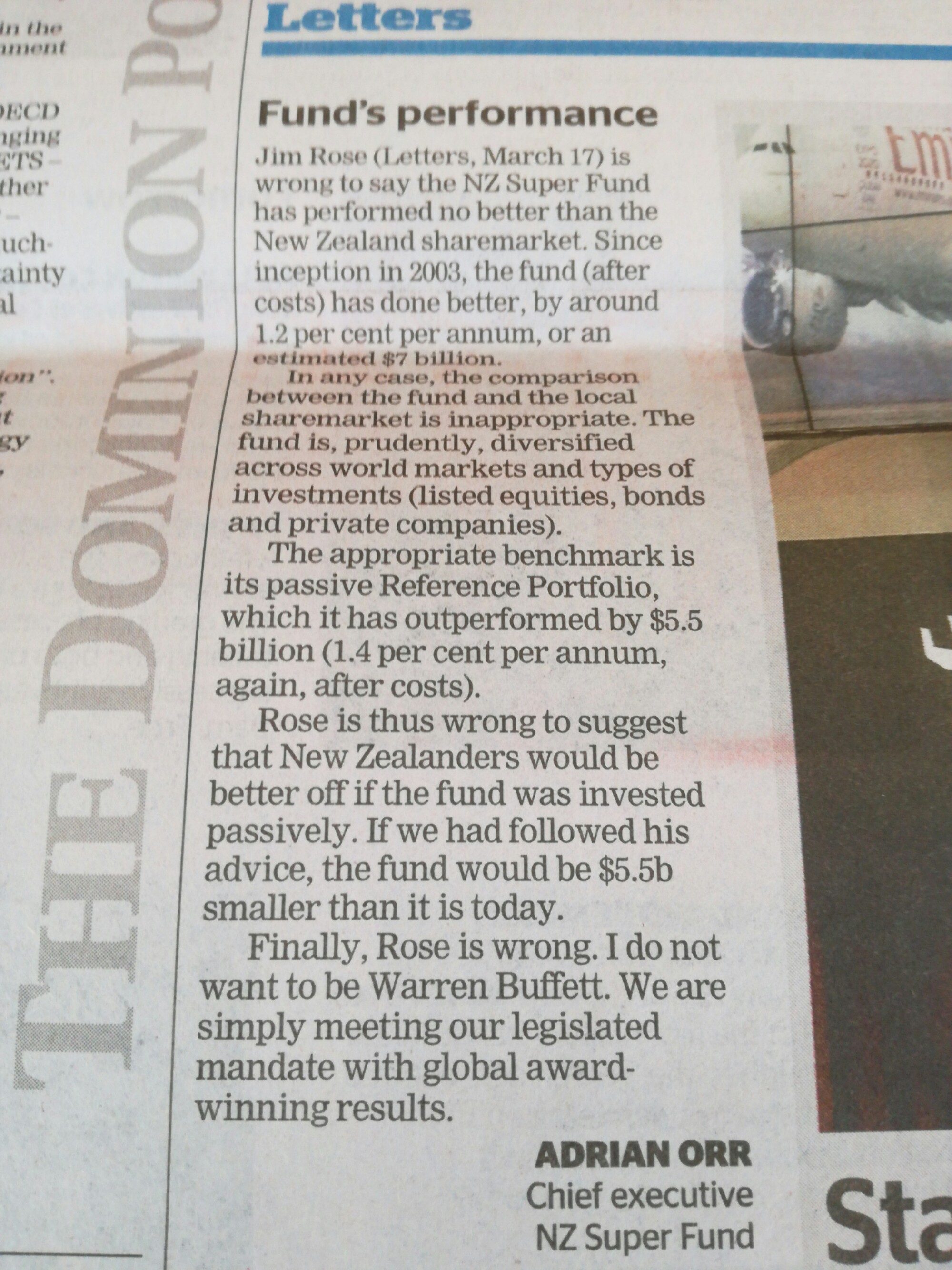

Letter to @DomPost on @NZSuperfund performance @Taxpayersunion utopiayouarestandinginit.com/2017/03/18/let… https://t.co/wxo6F1zZn5—

Jim Rose (@JimRose69872629) March 18, 2017

The chief executive of the fund quibbles by claiming there is a 3rd way between active and passive investing but there is not as William Sharp explained in his timeless 1991 article, The Arithmetic of Active Management:

- A passive investor always holds every security from the market, with each represented in the same manner as in the market. Thus if security X represents 3 per cent of the value of the securities in the market, a passive investor’s portfolio will have 3 per cent of its value invested in X. Equivalently, a passive manager will hold the same percentage of the total outstanding amount of each security in the market2.

- An active investor is one who is not passive. His or her portfolio will differ from that of the passive managers at some or all times. Because active managers usually act on perceptions of mispricing, and because such misperceptions change relatively frequently, such managers tend to trade fairly frequently — hence the term “active.”

An active fund is a fund that is not a passive fund. If you do not own a balanced portfolio of every security in the market, you are an active investor.

The majority of the New Zealand Superannuation fund is passively invested but some of it is not. It is invested in dogs like KiwiBank, in Z service stations and even in some bad Portuguese loans.

It’s "threadbare" to question @NZSuperFund’s investment strategy @TaxpayersUnion

23 Mar 2017 Leave a comment

There really is an issue on which economists are unanimous, a big issue to boot.

Source: Diversified Investing | IGM Forum.

Actively-managed mutual funds cannot earn excess returns over index funds because in aggregate they earn the same as index funds, less the difference in cost. This was proposed by Sharpe in his timeless 1991 article, The Arithmetic of Active Management.

Of course, certain definitions of the key terms are necessary. First a market must be selected — the stocks in the S&P 500, for example, or a set of “small” stocks. Then each investor who holds securities from the market must be classified as either active or passive.

- A passive investor always holds every security from the market, with each represented in the same manner as in the market. Thus if security X represents 3 per cent of the value of the securities in the market, a passive investor’s portfolio will have 3 per cent of its value invested in X. Equivalently, a passive manager will hold the same percentage of the total outstanding amount of each security in the market2.

- An active investor is one who is not passive. His or her portfolio will differ from that of the passive managers at some or all times. Because active managers usually act on perceptions of mispricing, and because such misperceptions change relatively frequently, such managers tend to trade fairly frequently — hence the term “active.”

… Properly measured, the average actively-managed dollar must underperform the average passively-managed dollar, net of costs. Empirical analyses that appear to refute this principle are guilty of improper measurement.

In 2008, Warren Buffett made a bet of $1 million with Protégé Partners LLC that, including fees, costs and expenses, an S&P 500 index fund would outperform a hand-picked portfolio of hedge funds over the 10 years ending December 31, 2017.

Recent Comments