What are the biggest workplace time wasters?

16 Mar 2015 Leave a comment

in industrial organisation, labour economics, labour supply, managerial economics, occupational choice, organisational economics, personnel economics, survivor principle Tags: cyber loafing

Do Paul Samuelson’s criticisms of behavioural economics make him a double secret Austrian economist?

13 Mar 2015 Leave a comment

in applied price theory, Austrian economics, behavioural economics, comparative institutional analysis, entrepreneurship, industrial organisation, survivor principle Tags: efficient markets hypothesis, entrepreneurial alertness, Paul Samuelson

via Samuelson vs. Friedman, David Henderson | EconLog | Library of Economics and Liberty and An Interview With Paul Samuelson, Part One — The Atlantic.

Signs of poor management – Not listening and not making people feel valued

12 Mar 2015 Leave a comment

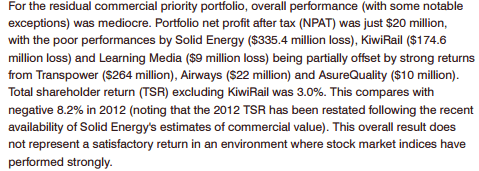

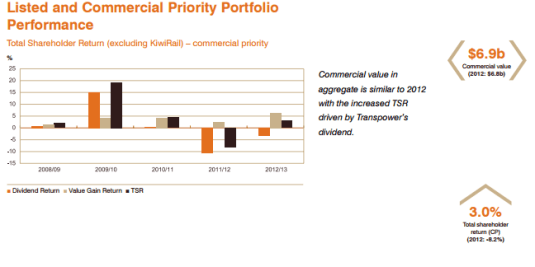

NZ taxpayers made a $20 million profit on its $30 billion state owned enterprises portfolio!

11 Mar 2015 Leave a comment

in economics of bureaucracy, industrial organisation, politics - New Zealand, privatisation Tags: privatisation, state owned enterprises

KiwiRail is such a dog that the Treasury reports on the rate of return to the taxpayer on the state owned enterprises portfolio by excluding KiwiRail from its calculations of rates of return.

The Treasury doesn’t do similar adjustments for state owned enterprises that are performing unusually well, so total shareholder return figures should be reported without this KiwiRail exception. If you buy a dog, you should own up to the fleas it spreads to the rest of your portfolio.

Trying to pretend that KiwiRail is just not there, or survives on the largess of someone other than the one and only New Zealand taxpayer, does no one any favours. This KiwiRail exception will have to apply for at least 10 years to the annual commercial portfolio report of the Treasury. I want to know the total shareholder return, including KiwiRail every year without exception or special pleading.

That total shareholder return of -8.2% in 2012 is worthy of comment too:

The portfolio generated a net loss after tax of $1.8 billion driven by a restructuring of KiwiRail’s balance sheet and reductions in bottom line results for Meridian and Solid Energy, affected by hydrology and coal market deterioration respectively.

It’s time for the government to wash its hands of Solid Energy and let it go bankrupt – updated

11 Mar 2015 1 Comment

in economics of bureaucracy, politics - New Zealand, survivor principle Tags: corporate welfare

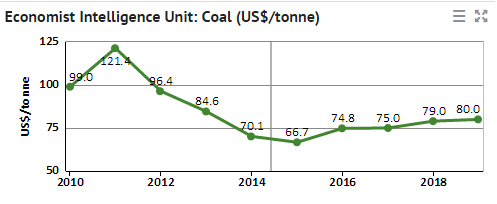

Government owned mining company Solid Energy lost $182 million last year. It is already received nearly $200 million in corporate welfare in bailouts from the New Zealand taxpayer. It’s time to call a halt.

The Christchurch-based coalminer is negotiating with banks in a bid to reduce its $320 million debt. In 2013, its annual revenue dropped by a third to $631 million.

Solid Energy invested heavily on a strategy that energy prices were going to go up and up. That investment strategy was against the market sentiment of that time, much less afterwards and the collapse of oil prices.

While Prime Minister John Key said on March 2 that it was not the Government’s preferred option to put more taxpayer cash into Solid Energy, Minister of Finance Bill English flatly ruled out cash, loans or guarantees. I hope Bill English wins that political struggle at the Cabinet table for the sake of the long-suffering New Zealand taxpayer.

What is worse, the government has indemnified the directors of Solid Energy against unspecified liabilities thus giving them an open-ended cheque-book, from what I can see, to trade while insolvent:

State Owned Enterprises Minister Todd McClay confirmed last month that the Crown has offered an indemnity to the board of Solid Energy last year, but would not comment on what it was.

Asked if directors had raised concerns with him that they might be trading while insolvent, English said: “Any director of a company like this has that question uppermost in their mind. They need to be sure all the time that they’re not trading while insolvent.”

Directors’ duties regarding trading while insolvent is the last line of defence against financial irresponsibility. There are both civil liability and criminal penalties for trading while insolvent under company law.

Solid Energy has already been a black hole for nearly $200 million in taxpayers’ money as well as considerable bank write-offs of loans.

The company appeared before the Finance and Expenditure Select Committee of Parliament this morning. It told MPs the company was solvent and marginally cash positive, but looking at another significant loss this year.

It should be a matter of policy that the government, any government, should not indemnify directors of any company, be they government owned or not, for breaches of directors’ duties. It’s a matter of the rule of law and of governments not privileging itself in the marketplace at the expense of the taxpayer.

What is the point of having a State Owned Enterprises Act and setting up these businesses as companies with a duty to be as successful as a company not owned by the government if they don’t have to obey the most fundamental safeguards in company law when push comes to shove?

If these indemnities have indeed been issued by the government for breaches of directors’ duties regarding insolvency, and it seems as though they have been, what is the Crown liability to creditors if Solid Energy is indeed trading while insolvent? These indemnities may allow the creditors to pierce the corporate veil and sue the New Zealand government.

In the revenge of directors duties, the directors of banks and any other creditor will have a director’s duty to sue the New Zealand government for all it can get as a result of these indemnities.

At a minimum, the New Zealand government will have to settle out of court or go all the way to the Supreme Court because hundreds of millions of dollars are involved from the bank write-offs, past and present.

Naturally, the ideological blinkers of the opposition party in New Zealand prevents it from saying the obvious, which is calling for the Solid Energy to be put in receivership. The Labour Party spokesman on state owned enterprise attacked the stewardship of the Minister of Finance as a shareholding Minister, but had nothing to say in terms of solutions, including putting the company into receivership.

The Green Party did a little bit better in 2013 when its spokesman talked about a need for a transition to sustainable jobs – the Green party code for layoffs:

“The National Government need to take responsibility for their mismanagement of Solid Energy and cut their losses,” said Mr Hughes.

“The banks that made risky loans to Solid Energy need to bear the cost of their mistakes”. “Coal is not going to be the fuel of our future if we are to stabilise our climate”.

“New Zealanders and Solid Energy workers need a just transition into more sustainable jobs – jobs that don’t fry the planet.”

“The longer this Government effectively denies climate change, the more taxpayer money will go to subsidising coal and its foreign backers.”

Things are getting desperate when the Greens find a corporate welfare so appalling that they actually oppose it, if only because of support for lower carbon emissions. That is one green hypocrisy too many if it supported a bailout of a coal miner.

Winston’s big port up North won’t have any business

10 Mar 2015 Leave a comment

in applied welfare economics, industrial organisation, politics - New Zealand, rentseeking, transport economics

In the first shot in the pork-barrelling for a by-election, veteran New Zealand populist Winston Peters wants to stop the expansion of the Port of Auckland and move the extra shipping traffic up north to the Port of Whangarei:

And we will upgrade the Auckland to Northland railway line and build the rail link to your port

The Port of Whangarei is about two hours north by car from Auckland. Auckland is a global city of approaching 2 million. Whangarei is the only city up North, with a population of 50,000.

45% of the import traffic to the Port of Auckland is cars. Around 90% of light vehicle imports in New Zealand come through the Port of Auckland. The rest may go through Littleton.

|

|

|

Jellicoe and Freyberg wharves are located between the two container terminals. |

Bledisloe multipurpose Wharf |

Striving to move some of this light vehicle imports from the Port of Auckland up north to the Port of Whangarei where they be unloaded from a ship onto trains for a short train ride to Auckland, unloaded again onto trucks all seems unnecessary expense.

Photo: Port of Whangarei.

Auckland appears to have spare container capacity up until at least 2035, so this port up North will simply not have much to do in terms of extra container traffic because it will have to compete on the basis of cost and proximity to markets.

Photo: The Marsden Point Oil Refinery on the opposite shore of Whangarei Harbour.

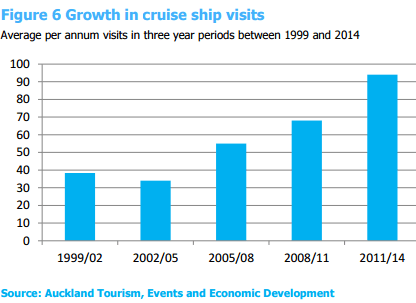

The traffic that is coming under pressure regarding capacity of the Port of Auckland is multi-cargo traffic such as building materials, vegetables, wheat, vehicles and other goods. The situation is further aggravated by the rapid increase in the number and increased size of cruise ships.

As a good part of the market for the multi cargo traffic is in Auckland, landing them away from their main market just makes no sense and will not happen unless the port of Auckland is prohibited by law from expanding and ships are not allowed to divert to ports such as Wellington and Christchurch.

The number of cruise ships visiting Auckland in the last 10 years to about 90 and is expected to reach one 20 by 2020 and 150 by 2030. That traffic cannot be diverted up north to the Port of Whangarei.

Any export traffic that would be viable to send through the Port of Whangarei up north will already be going through it. Export competitiveness is highly sensitive to costs as exporters must simply take the going price in the international market.

This question should be asked more often about the regulation of purported natural monopolies

09 Mar 2015 Leave a comment

Why delicious Indian food is surprisingly unpopular in the U.S.

05 Mar 2015 Leave a comment

in applied price theory, industrial organisation, survivor principle Tags: creative destruction, food, Indian food

No need to rage against the gaucheness of Americans who, in fact, have embraced many foods:

The cuisine is among the most labor intensive in the world. And yet Americans are unwilling to pay beyond a certain, and decidedly low, price point.

Via Why delicious Indian food is surprisingly unpopular in the U.S. – The Washington Post.

Creative destruction and what remains of the legacy mass media

05 Mar 2015 Leave a comment

in economic history, economics of media and culture, industrial organisation, survivor principle Tags: creative destruction, Google, legacy media

HT: zerohedge.com

France, here the New Zealand labour market comes – part 2! How the Employment Court is re-regulating

04 Mar 2015 7 Comments

in applied price theory, Austrian economics, entrepreneurship, F.A. Hayek, George Stigler, human capital, industrial organisation, job search and matching, labour economics, law and economics, Ludwig von Mises, politics - New Zealand, survivor principle Tags: Armen Alchian, employment law, employment protection laws, entrepreneurial alertness, France, Israel Kirzner, The fatal conceit, The pretence to knowledge

As discussed yesterday, if the Employment Court had its way, New Zealand case law under the Employment Relations Act regarding redundancies and layoffs would be as job destroying as those in France.

The Employment Court’s war against jobs goes back more than 20 years. To 1991 and G N Hale & Son Ltd v Wellington etc Caretakers etc IUW where the Court held that a redundancy to be justifiable under law it must be ‘unavoidable’, as in redundancies could only arise where the employer’s capacity for business survival was threatened.

The Court of Appeal slapped that down and affirm the right of the employer to manage his business in no uncertain terms:

…this Court must now make it clear that an employer is entitled to make his business more efficient, as for example by automation, abandonment of unprofitable activities, re-organisation or other cost-saving steps, no matter whether or not the business would otherwise go to the wall…

The personal grievance provisions … should not be treated as derogating from the rights of employers to make management decisions genuinely on such grounds. Nor could it be right for the Labour Court to substitute its own opinion as to the wisdom or the expediency of the employer’s decision.

When a dismissal is based on redundancy, it is the good faith of that basis and the fairness of the procedure followed that may fall to be examined on a complaint of unjustifiable dismissal

… the Court and the grievance committees cannot properly be concerned with an examination of the employer’s accounts except in so far as it bears on the true reason for dismissal.

The Employment Court could only inquire as to the genuineness of the employer’s decision and the procedures adopted. The Court could not substitute their views on management decisions. No second-guessing.

In Brake v Grace Team Accounting Ltd, the Employment Court found its way back into second-guessing employer’s decisions about how to manage their business. The figures used by the employer to decide that a redundancy was required were in error. The employer miscalculated.

The Employment Court had previously held in Rittson-Thomas T/A Totara Hills Farm v Hamish Davidson that the statutory test of what a fair and reasonable employer could have done in all the circumstances applies to the substantive reasoning for redundancies. Some enquiry into the employer’s substantive decision is required to establish that a hypothetical fair and reasonable employer could also make the same decision in all of the circumstances.

Subsequently in Brake v Grace Team Accounting Ltd, the Employment Court found that the actions by the employer were “not what a fair and reasonable employer would have done in all the circumstances” and “failed to discharge the burden of showing that the plaintiff’s dismissal for redundancy was justified”.

The Court found that the redundancy was “a genuine, but mistaken, dismissal”, but it still found that the dismissal was substantively unjustified. That is a major new development. Mistaken dismissals that are genuine are unlawful and grounds for compensation under the employment law.

The case was appealed where the issues were whether the correct test had been applied. The Court of Appeal, in a sad day for employers, job creation and the unemployed, found that the Employment Court was within its rights to do what it did and applied the statutory tests correctly:

GTA acted precipitously and did not exercise proper care in its evaluation of its business situation and it made its decision about Ms Brake’s redundancy on a false premise.

So it never turned its mind to what its proper business needs were but rather proceeded to evaluate its options based on incorrect information. We can see no error in the finding by the Employment Court that a fair and reasonable employer would not do this.

The test is now that fair and reasonable employers in New Zealand do not make mistakes. A much greater burden is now laid upon employers to show that not only that redundancies are justified, but they have made careful calculations and no mistakes.

No more seat of your pants entrepreneurship in New Zealand. No more entrepreneurial hunches – the essence of entrepreneurship is acting on hunches and other judgements that are incapable of being articulated to others and about which there is mighty disagreement in many cases. As Lavoie (1991) states:

…most acts of entrepreneurship are not like an isolated individual finding things on beaches; they require efforts of the creative imagination, skillful judgments of future costs and revenue possibilities, and an ability to read the significance of complex social situations.

The essence of entrepreneurship is your hunches are better than the next guy’s and you survive in competition by backing that hunch often to the consternation of the crowd. As Mises explains:

[Economics] also calls entrepreneurs those who are especially eager to profit from adjusting production to the expected changes in conditions, those who have more initiative, more venturesomeness, and a quicker eye than the crowd, the pushing and promoting pioneers of economic improvement…

The entrepreneurial idea that carries on and brings profits is precisely that idea which did not occur to the majority… The prize goes only to those dissenters who do not let themselves be misled by the errors accepted by the multitude

In many cases, those entrepreneurial hunches are sorted, sifted and selected on the basis of trial and error in the marketplace. Central to Hayek’s conception of the meaning of competition is it is a process of trial and error with many errors:

Although the result would, of course, within fairly wide margins be indeterminate, the market would still bring about a set of prices at which each commodity sold just cheap enough to outbid its potential close substitutes — and this in itself is no small thing when we consider the insurmountable difficulties of discovering even such a system of prices by any other method except that of trial and error in the market, with the individual participants gradually learning the relevant circumstances.

Remember Hayek’s conception of competition as a discovery procedure where prices and production emerge through the clash of entrepreneurial judgements and competitive rivalry:

…competition is important only because and insofar as its outcomes are unpredictable and on the whole different from those that anyone would have been able to consciously strive for; and that its salutary effects must manifest themselves by frustrating certain intentions and disappointing certain expectations

Errors are no longer permitted in the New Zealand labour market by the Employment Court. The Court has outlawed error in redundancy decisions.

This is despite the fact that the conception by Kirzner of the market process is that it is an error correction procedure without rival and a central role of entrepreneurial alertness is to correct errors in pricing and production:

It is important to notice the role played in this process of market discovery by pure entrepreneurial profit. Pure profit opportunities emerge continually as errors are made by market participants in a changing world. The inevitably fleeting character of these opportunities arises from the powerful market tendency for entrepreneurs to notice, exploit, and then eliminate these pure price differentials.

The paradox of pure profit opportunities is precisely that they are at the same time both continually emerging and yet continually disappearing. It is this incessant process of the creation and the destruction of opportunities for pure profit that makes up the discovery procedure of the market. It is this process that keeps entrepreneurs reasonably abreast of changes in consumer preferences, in available technologies, and in resource availabilities.

Rothbard made similar arguments about the centrality of discrepancies and error in entrepreneurship:

The capitalist-entrepreneur buys factors or factor services in the present; his product must be sold in the future. He is always on the alert, then, for discrepancies, for areas where he can earn more than the going rate of interest.

In Frank Knight’s conception of profit, there were temporary profits that arise from the correction of error:

In the theory of competition, all adjustments “tend” to be made correctly, through the correction of errors on the basis of experience, and pure profit accordingly tends to be temporary.

The Employment Court misunderstands the market process as a process of error correction. Those errors are identified through entrepreneurial alertness and trial and error. These errors are both of over-optimism and over-pessimism as Kirzner explains:

Errors of over-pessimism are those in which superior opportunities have been overlooked. They manifest themselves in the emergence of more than one price for a product which these resources can create. They generate pure profit opportunities which attract entrepreneurs who, by grasping them, correct these over-pessimistic errors.

The other kind of error, error due to over-optimism, has a different source and plays a different role in the entrepreneurial discovery process. Over-optimistic error occurs when a market participant expects to be able to complete a plan which cannot, in fact, be completed.

A considerable part of entrepreneurial alertness arises from the business opportunities created by sheer ignorance and pure error as Kirzner explains:

What distinguishes discovery (relevant to hitherto unknown profit opportunities) from successful search (relevant to the deliberate production of information which one knew one had lacked) is that the former (unlike the latter) involves that surprise which accompanies the realization that one had overlooked something in fact readily available. (“It was under my very nose!”)

The market process is a selection procedure where the more efficient survive for reasons that may be unknown to the entrepreneurs directly concerned as well as to observers and officious judges. Alchian pointed out the evolutionary struggle for survival in the face of market competition ensured that only the profit maximising firms survived:

- Realised profits, not maximum profits, are the marks of success and viability in any market. It does not matter through what process of reasoning or motivation that business success is achieved.

- Realised profit is the criterion by which the market process selects survivors.

- Positive profits accrue to those who are better than their competitors, even if the participants are ignorant, intelligent, skilful, etc. These lesser rivals will exhaust their retained earnings and fail to attract further investor support.

- As in a race, the prize goes to the relatively fastest ‘even if all the competitors loaf.’

- The firms which quickly imitate more successful firms increase their chances of survival. The firms that fail to adapt, or do so slowly, risk a greater likelihood of failure.

- The relatively fastest in this evolutionary process of learning, adaptation and imitation will, in fact, be the profit maximisers and market selection will lead to the survival only of these profit maximising firms.

The surviving firms may not know why they are successful, but they have survived and will keep surviving until overtaken by a better rival. All business needs to know is a practice is successful.

One method of organising production and supplying to the market will supplant another when it can supply at a lower price (Marshall 1920, Stigler 1958). Gary Becker (1962) argued that firms cannot survive for long in the market with inferior product and production methods regardless of what their motives are. They will not cover their costs.

The more efficient sized firms are the firm sizes that are currently expanding their market shares in the face of competition; the less efficient sized are those firms that are currently losing market share (Stigler 1958; Alchian 1950; Demsetz 1973, 1976). Business vitality and capacity for growth and innovation are only weakly related to cost conditions and often depends on many factors that are subtle and difficult to observe (Stigler 1958, 1987). The Employment Court pretends to know better than the outcome of the competitive struggle in the market for survival.

The Employment Court also believes employers have something akin to academic tenure. In 2010, the Court found that an employee’s redundancy was unjustified because the employer did not offer redeployment and there is no requirement that the right of the redeployment be written into the employment agreement (Wang v Hamilton Multicultural Services Trust). The particulars of this case were quite interesting:

- A new management role was created with significantly more responsibility for training, supervision and decision making than the redundant finance administrator role, with a 50% salary increase to recognise the increased responsibilities and duties.

- The vacancy was advertised externally but the existing finance administrator was encouraged to apply.

- His experience and qualifications meant that he could fulfil the new role, albeit with some up-skilling.

- He decided not to apply for it to avoid jeopardising a personal grievance claim that his redundancy was not genuine and therefore unjustified.

In the case at hand, the Employment Court held that the employer was obliged to look for alternatives to making the employee redundant. Given that he would be able to perform the new finance manager position with some up-skilling, the employer should have offered him the position rather than simply inviting him to apply for it.

The notion that an employee through training can quickly increase their marginal productivity by 50% to fill a more senior role contradicts the modern labour economics of human capital. A 50% salary increase through a bit of training would imply extraordinary annual returns on other forms of on-the-job training and formal education as well as the training at hand in the Employment Court case.

I would very much like to be in the position where I can get a 50% salary increase after a bit of training. As I recall, I required about 5-10 years of on-the-job human capital acquisition before my starting salary as a graduate was 50% higher through promotion and transfers.

In summary, the Employment Court stands apart from the modern labour economics of human capital and job search and matching as well as the modern theory of entrepreneurial alertness, and the market as a discovery procedure and an error correction mechanism. The Employment Court has fallen for both the pretence to knowledge and the fatal conceit.

Why doesn’t capital flow from the rich countries to supposedly capital shallow New Zealand?

03 Mar 2015 Leave a comment

in econometerics, economic growth, industrial organisation, politics - New Zealand Tags: capital mobility, Trans-Tasman income gap

Hall and Scobie (2005) attributed 70 percent of the labour productivity gap with Australia to New Zealand workers using less capital per worker than their Australian counterparts, rather than their using w3capital less efficiently. Figure 1 shows that the capital labour ratio is lower in New Zealand than in Australia and has been lower than Australia for several decades and is getting worse.

Figure 1: Capital intensity in New Zealand relative to Australia: 1978-2002

Source: Hall and Scobie 2005.

In 1978, New Zealand and Australian workers had about the same amount of capital per hour worked. By 2002, capital intensity in Australia was over 50 percent greater than in New Zealand. This lower rate of capital intensity is capital shallowness.

Capital should flow to countries with the highest risk adjusted rates of return. If workers in a country work with less capital than in other countries, the rate of return on providing them with more capital is higher than the global average return to capital. As Stigler (1963) said:

There is no more important proposition in economic theory than that, under competition, the rate of return on investment tends toward equality in all industries.

Entrepreneurs will seek to leave relatively unprofitable industries and enter relatively profitable industries, and with competition there will be neither public nor private barriers to these movements.

This mobility of capital is crucial to the efficiency and growth of the economy: in a world of unending change in types of products that consumers and businesses and governments desire, in methods of producing given products, and in the relative availabilities of various resources—in such a world the immobility of resources would lead to catastrophic inefficiency

Hall and Scobie (2005) acknowledged that lower capital intensities could be entirely a by-product of lower MFP. New Zealand had the third worst MFP growth performance since 1985, one quarter the OECD average (OECD 2009).

Rather than money being left on the table by persistent, known but unexploited entrepreneurial opportunities for pure profit by investing more in under-capitalised New Zealand and providing additional capital and equipment and more advanced technologies for New Zealanders to work with, investors have done the best they could the relative poor investment opportunities here.

Figure 2: Differences in capital intensity: the case of different production functions

Source: Hall and Scobie 2005.

A divergence in labour productivity levels between Australia and New Zealand emerged in the 1970s and 1980s. Kehoe and Ruhl (2003) attributed 96 percent of the fall in labour productivity in New Zealand between 1974 and 1992 to a fall in MFP. Changes in capital intensities played a minor role.

Aghion and Howitt (2007) found that three-quarters of the growth in output per worker in Australia and New Zealand between 1960 and 2000 was due to growth in MFP. New Zealand’s annual MFP growth of 0.45 percent between 1960 and 2000 was simply much lower than Australia’s 1.26 percent per year. Capital deepening was equally lower in New Zealand with 0.16 percent comparing to 0.41 percent in Australia.

Less would be invested in a country if the returns are lower because the capital is poorly employed. There might be a lack of complementary skills and education and, more often, policy distortions that lower MFP (Alfaro et al 2007; Caselli and Feyrer 2007; Lucas 1990).Investment in ICT capital is greatest in the USA because it is the global industrial leader and has very flexible markets. Investment in ICT in the EU is proportionately less because less flexible markets make ICT investments in the EU members less fruitful to investors.

To explore the relative role of lower MFP and the cost of capital in capital shallowness, Hall and Scobie (2005) used national accounts data to estimate the cost of capital and found that New Zealand faced a higher cost of capital than Australia, the USA and the OECD average since the early 1990s. Research that is more recent disputes these concerns about a higher cost of capital in New Zealand.

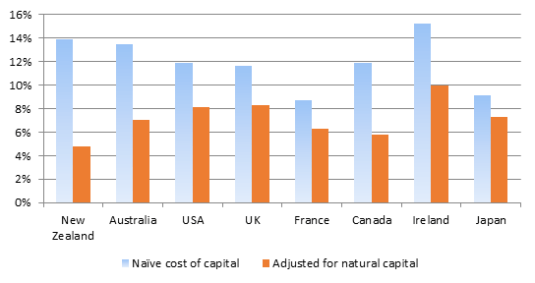

In Caselli and Feyrer’s (2007) revised cost of capital estimates, the cost of capital is significantly lower in New Zealand than in Australia and elsewhere in the OECD area such as the USA, Japan and UK – see Figure 3. Caselli and Feyrer (2007) correct for an overestimation of the cost of capital that is prevalent for countries such as New Zealand where the value of land and natural resources are high.

Figure 3: Caselli and Feyrer’s Estimates of the Cost of Capital, 1996

Source: Caselli and Feyrer (2007); Hsieh and Klenow (2011).

Notes: The measure of capital income used by Hall and Scobie (2005) to calculate the cost of capital includes payments to reproducible physical capital (equipment, machinery, ICT, buildings and other structures) as well as payments to natural capital (land and natural resources). Dividing the income that flows to all types of capital including land and natural resources by just the value of reproducible physical capital overestimates the cost of capital. Caselli and Feyrer (2007) used World Bank (2006) estimates of natural capital stocks in 1996 to estimate of income flows to reproducible physical capital. Their estimates excluded income flows to land and natural resources to estimate the cost of reproducible capital.

Caselli and Feyrer (2007) revised estimate in Figure 3 is for the cost of capital for investing in equipment, machinery, ICT, buildings and structures. When land and resources are included, shown in light blue as the naive cost of capital, the estimated cost of capital is one-half of percentage point higher in New Zealand than in Australia and two percent higher in New Zealand than the USA and UK in Figure 3. When land and natural resources are excluded, shown in red as the adjusted for natural capital estimate, the cost of capital is much lower in New Zealand than in Australia, the USA, Japan and UK – see Figure 3.

What Caselli and Feyrer (2007) show is the estimation of the cost of capital to New Zealand is fraught with statistical difficulties. A broader data set yields radically different results. That is the broader lesson.

At a minimum, safest thing to say, is there are no reliable estimates of the cost of capital in New Zealand. Depending on how you measure it, the cost of capital in New Zealand is either much higher or much lower than in the leading industrial countries such as the USA and UK. Such a broad range of estimates is no basis for public policy interventions.

When having to choose between arguing for a persistent, known but unexploited entrepreneurial opportunities for risk-free profit left on the table in New Zealand by foreign investors for decades, and measurement error in the case of one of the nastiest measurement jobs – measuring capital and natural resources – measurement error is more likely.

Capital is the most internationally mobile of factors of production. Entrepreneurs have every incentive to move it to new destinations with higher risk-adjusted rates of returns. Returns will not be exactly equal, but there will be a tendency for equalisation subject to these reservations listed by George Stigler in 1963:

- Some dispersion in rates of return exist because of imperfect knowledge of returns on alternative investments.

- Dispersion of returns would arise because of unexpected developments and events which call for movements of resources requiring considerable time to be completed.

- Dispersion in rates of return would arise because of differences among industries in monetary and nonmonetary supplements to the average rate of return.

- In any empirical study, there is also a fourth source of dispersion: the difference between the income concepts used in compiling the data and the income concepts relevant to the allocation of resources.

The last of these reservations listed by George Stigler in 1963 about the statistical concepts used in compiling what data can be collected and the concepts relevant to the entrepreneurial decisions about the allocation of resources appear to be crucial to the debate about capital shallowness in New Zealand. They also echo Hayek’s great reservation in his 1974 lecture The Pretence to Knowledge about focusing on what can be measured rather than what is important in both economic analysis and public policy making:

We know: of course, with regard to the market and similar social structures, a great many facts which we cannot measure and on which indeed we have only some very imprecise and general information. And because the effects of these facts in any particular instance cannot be confirmed by quantitative evidence, they are simply disregarded by those sworn to admit only what they regard as scientific evidence: they thereupon happily proceed on the fiction that the factors which they can measure are the only ones that are relevant.

Hall and Scobie (2005) were careful scholars who noted that possibility that the apparent capital shallowness in New Zealand is merely the result of measurement error because of the problems of measuring land and natural. Caselli and Feyrer (2007) justify their caution and vindicated the view that the marginal product of capital is pretty much the same all round the world. As Caselli and Feyrer (2007) explain:

There is no prima facie support for the view that international credit frictions play a major role in preventing capital flows from rich to poor countries.

Lower capital ratios in these countries are instead attributable to lower endowments of complementary factors and lower efficiency, as well as to lower prices of output goods relative to capital. We also show that properly accounting for the share of income accruing to reproducible capital is critical to reach these conclusions.

There is various debates in policy circles in New Zealand about this lack of capital per worker and a higher cost of capital in New Zealand.

But that debate and any policy measures that were introduced as a result may be misplaced and all due to measurement error, or more correctly the grave difficulties of measuring both the capital stock and the cost of capital, both generally and in New Zealand course of its large bounty of natural resources. The data was always in doubt, so any policy interventions should be very cautious and incremental.

It would have been surprising to find that lower productivity in New Zealand was due to a lack of access to capital. There is growing evidence that capital intensities are not a major contributor to cross-national per capita income gaps.

There is a broad empirical consensus that capital intensity explains about 20 per cent of cross-country income differences; differences in human capital account for 10 to 30 per cent of cross-national differences with MFP accounting for the remaining 50 to 70 percent (Hsieh and Klenow 2011).

The New Zealand capital shallowness hypothesis is too marred in measurement shortcomings to rebut this broad empirical consensus about MFP differences between all other countries. For example, when reviewing the trans-Atlantic productivity and income gap, Edward Prescott said:

The capital factor is not an important factor in accounting for differences in incomes across the OECD countries… [It] contributes at most 8 percent to the differences in income between any of these countries.”

At the broader level, this blind alley about capital shallowness in New Zealand illustrates the pretence to knowledge. The politicians and bureaucrats pretended to know the cost of capital and the size of the capital stock in New Zealand and then work out what to do in response while doing more good than harm. This was despite serious reservations about the quality of data at hand.

This blind alley about the cost of capital and capital shallowness in New Zealand illustrates Josh Lerner’s point about distractions such as these and their many equivalents overseas reinforce the importance of the neglected art of setting the table– of fostering a favourable business environment. The neglected art of setting the table includes:

- investing in a favourable tax regime (low taxes on capital gains relative to income tax are particularly important as studies show people respond to incentives); and

- making the labour market more flexible (again the opposite of what has happened in continental Europe ),

- reducing informal and formal sanctions on involvement in failed ventures;

- easing barriers to technology transfer, and

- providing entrepreneurship education for students and professionals alike.

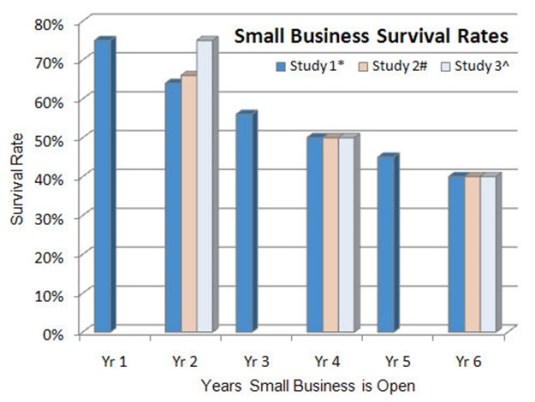

What is the survival rate of new small businesses?

02 Mar 2015 Leave a comment

in economic history, entrepreneurship, survivor principle

HT: Do nine out of 10 new businesses fail, as Rand Paul claims? – The Washington Post.

For venture capital start-ups, about three or 4 out of 10 fail; three or 4 out of 10 return the original investment, with the rest offering a substantial profit.

Digital ad revenue by company

02 Mar 2015 Leave a comment

in economics of media and culture, industrial organisation, survivor principle Tags: creative destruction, legacy media

Recent Comments