Today in the Dominion Post, Bill Rosenberg, a trade union self-described economist, argued that the workers are not getting their fair share of productivity gains in New Zealand over the last 35 years:

I calculate that wages in the 60 per cent of the economy studied by the commission would have been 12 per cent higher on average by March 2011, if they had kept up with productivity since 1978.

He then rounded up the usual Twitter Left suspects:

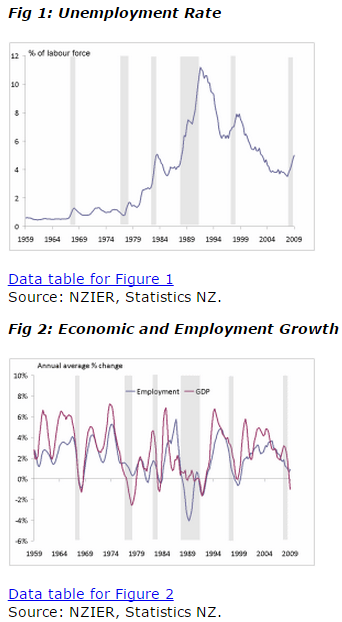

The commission’s study is important in that it finds that a large part of the fall in the labour share of income in the 1990s was due to high unemployment created by the radical restructuring of the economy that began in the 1980s and the Employment Contracts Act passed in 1991. Australia underwent similar restructuring during the period, but its labour income share fell only slightly. Its labour market is underpinned with an award system and other protections.

12%! 12% is at all that the class struggle is about over a 35 year period in terms of wage losses and labour surplus extract by the greedy bosses?

Figure 1: Real equivalised median household income (before housing costs) by ethnicity, 1988 to 2013 ($2013)

Source: Bryan Perry, Household incomes in New Zealand: Trends in indicators of inequality and hardship 1982 to 2013. Ministry of Social Development (July 2014).

As shown in figure 1, between 1994 and 2010, real equivalised median New Zealand household income rose by 47%; for Māori, this rise was 68%; for Pasifika, the rise in real equivalised median household income was 77%. Obviously these losses from the change in shares of GDP are dwarfed by the general increases in living standards over the last 20 years.

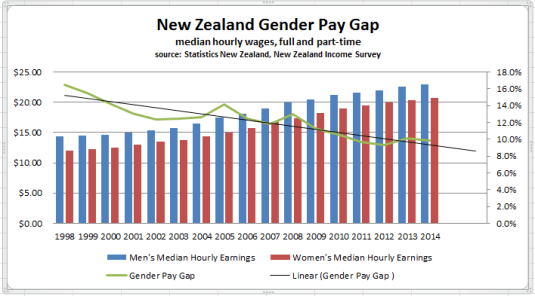

As is common with every member of the Left over Left that I run into these days, such as Bill Rosenberg, their analysis has no gender analysis.

The Left over Left invariably fail to mention that New Zealand has the smallest gender wage gap of all the industrialised countries.

Over the last more than two decades in New Zealand, there has been sustained income growth spread across all of New Zealand society contrary to hopes and dreams of the Left over Left. Perry (2014) reviews the poverty and inequality data in New Zealand every year for the Ministry of Social Development. He concluded that:

Overall, there is no evidence of any sustained rise or fall in inequality in the last two decades. The level of household disposable income inequality in New Zealand is a little above the OECD median. The share of total income received by the top 1% of individuals is at the low end of the OECD rankings.

As for Rosenberg’s hypothesis that it’s all the fault of the Employment Contracts Act, that doesn’t stand up. Figure 2 shows that union membership has been in a long slow decline in New Zealand since the mid-1970s. This is been pretty much the pattern all round the world.

Figure 2: Union density, New Zealand, Australia, the UK and USA 1970-2013

Source: OECD Stats Extract

The much hated Employment Contracts Act 1991, much hated by the Left over Left, doesn’t really show up in the union density figures in figure 2. There is no sudden break in trend obvious in figure 2 in the early 1990s when the Employment Contract Act was passed.

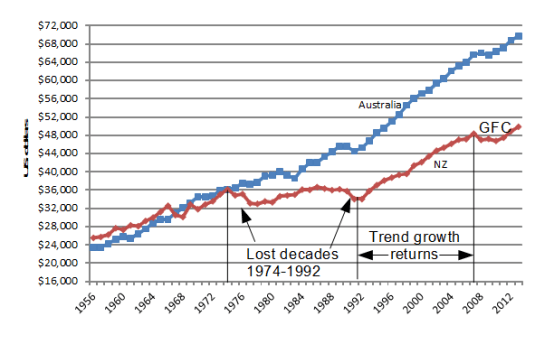

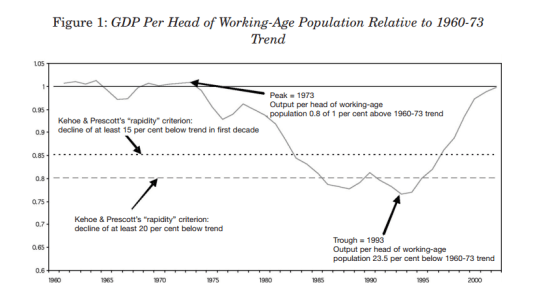

Indeed, the passage of the Employment Contracts Act 1991 was followed by a 15 year economic boom in employment and economic growth, as shown in figure 3. This was after the lost decades of 1974 to 1992 when there was next to no growth in real GDP per New Zealander aged 15 to 64. The good old days when the Lost Decades for New Zealand.

Figure 3: Real GDP per New Zealander and Australian aged 15-64, converted to 2013 price level with updated 2005 EKS purchasing power parities, 1956-2013

Source: Computed from OECD Stat Extract and The Conference Board, Total Database, January 2014.

Things are so grim for the class struggle in New Zealand that the leader of the Labour Party has had to redefine the working class because it is withering away so rapidly because so many workers are joining the middle-class:

Recent Comments