Why are the Greeks so upset? pic.twitter.com/KmoRjTw7Mq

— ian bremmer (@ianbremmer) February 17, 2015

Italy is Europe’s ticking time bomb

15 Feb 2015 Leave a comment

What happens when you play “chicken” with a game theorist (The Greek Finance Minister)?

14 Feb 2015 Leave a comment

in currency unions, Euro crisis, international economics Tags: game theory, Greece, Greek default, optimal currency areas, sovereign default

Luke Froeb suggests:

However, opting for forgiveness risks creating dangerous incentives for other countries to act in the same way as Athens. “Germany may decide that if the eurozone does not punish Greece, it will have problems with other countries such as Spain and Italy,” says Roger Myerson, a Nobel-winning economist at the University of Chicago.

Mr Varoufakis should therefore try to convince Germany that Athens’ situation is unique and that other eurozone countries will not seek debt relief as a result, he says. In doing so, he would follow the illustrious precedent of the citizens of Melos, to whom Athens, during the Peloponnesian war between Athens and Sparta, gave the choice of surrendering or facing annihilation.

“The Melians sought to argue that they were different and that sparing them would not set a dangerous precedent vis-à-vis other islands,” says Mr Myerson.

The problem with this strategy, however, is that the other player may choose to build a reputation for toughness. This is what Athens opted for — it laid siege to the island and starved the inhabitants into submission.

via Managerial Econ: What happens when you play “chicken” with a game theorist? and Greek Game Theory: Default, Devaluation, Deliverance?..

Why did Britain join the EU? A new insight from economic (and political) history

11 Feb 2015 Leave a comment

in Euro crisis, international economic law, macroeconomics Tags: British economy, EU membership, European Union

Nice article by Nauro F. Campos and Fabrizio Coricelli on UK-EU history.

It tracks the history behind the two regions and why UK eventually joined EU in 1973:

View original post 189 more words

Is Euroland an optimal currency area?

05 Feb 2015 Leave a comment

in currency unions, Euro crisis, global financial crisis (GFC), macroeconomics, monetary economics Tags: Euroland, optimal currency area

Deflation and Depression: Is There an Empirical Link?

31 Jan 2015 Leave a comment

in budget deficits, business cycles, economic growth, Euro crisis, great depression, great recession, macroeconomics, monetary economics, politics - Australia, politics - New Zealand, politics - USA Tags: deflation, fiscal policy, liquidity traps, monetary policy, stabilisation policy

Deflation has a bad reputation. People blame deflation for causing the great depression in the 1930s. What worse reputation can you get as a self-respecting macroeconomic phenomena?

The inconvenient truth for this urban legend is empirical evidence of deflation leading to a depression is rather weak.

The most obvious is confounding evidence, is up until the great depression, deflation was commonplace. In the late 19th century, deflation coincided with strong growth, growth so strong that it was called the Industrial Revolution.

For deflation to be a depressing force, something must have happened in the lead up to the Great Depression to change the impact of deflation on economic growth.

Atkeson and Kehoe in the AER looked into the relationship between deflation and depressions and came up empty-handed.

Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

Deflation and Depression: Is There an Empirical Link?

Andrew Atkeson, and Patrick J. Kehoe, 2004.

Are deflation and depression empirically linked? No, concludes a broad historical study of inflation and real output growth rates. Deflation and depression do seem to have been linked during the 1930s. But in the rest of the data for 17 countries and more than 100 years, there is virtually no evidence of such a link.

View original post 1,842 more words

Greece should default and abandon the euro – Jeff Miron

27 Jan 2015 Leave a comment

in budget deficits, currency unions, development economics, economic growth, economic history, Euro crisis, fiscal policy, global financial crisis (GFC), growth disasters, law and economics, macroeconomics, poverty and inequality Tags: currency unions, Euroland, Greece, optimal currency area, sovereign default

The Greek depression compared

26 Jan 2015 Leave a comment

Economic Rebounds in U.S. and Euro Zone: Deceivingly Similar, Strikingly Different

20 Jan 2015 Leave a comment

in business cycles, Euro crisis, global financial crisis (GFC), great recession, labour economics, macroeconomics, unemployment Tags: Euroland

via Economic Rebounds in U.S. and Euro Zone: Deceivingly Similar, Strikingly Different – Dallas Fed.

Involuntary unemployment and the great vacation theories of the great depression and Eurosclerosis – updated again

10 Dec 2014 1 Comment

in economic growth, Edward Prescott, Euro crisis, great depression, job search and matching, labour economics, macroeconomics, Robert E. Lucas, unemployment Tags: Eurosclerosis, great depression, voluntary unemployment

Most Keynesian economists are convinced that something exists called involuntary unemployment and people can be unemployed through no fault of their own. They will accept the going wage but no employer is willing to offer it to them.

Lucas and Rapping’s (1969) paper, “Real Wages, Employment, and Inflation” provides the micro-foundations for an analysis of the labour suppl. They felt the need to reconcile the existence of unemployment with market clearing and referred to recent work of Armen Alchian (1969) on search explanations of unemployment.

Lucas and Rapping viewed unemployment as voluntary, including the mass unemployment during the great depression (Lucas and Rapping 1969: 748).

Lucas and-Rapping viewed current labour demand as a negative function of the current real wage. Current labour supply was a positive function of the real wage and the expected real interest rate, but a negative function of the expected future wage.

Under their framework, if workers expect higher real wages in the future or a lower real interest rate, current labour supply would be depressed, employment would fall, unemployment rise, and real wages increase.

Lucas and Rapping depicted labour suppliers as rational optimisers who engaged in inter-temporal substitution: working more when current wages were high relative to expected wages. The prevailing Keynesian approach assumed labour supply was passive, and movements in the demand for labour determined changes in employment.

Lucas and Rapping offered an unemployment equation relating the unemployment rate to actual versus anticipated nominal wages, and actual versus anticipated price levels. Unemployment could be the product of expectational errors about wages.

Lucas and Rapping’s model was poor at explaining unemployment after 1933 in terms of job search and expectational errors.

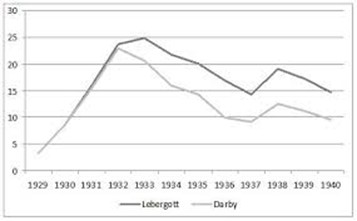

The graph below shows two different series for unemployment in the 1930s in the USA: the official BLS level by Lebergott; and a data series constructed famously by Darby. Darby includes workers in the emergency government labour force as employed – the most important being the Civil Works Administration (CWA) and the Works Progress Administration (WPA).

Once these workfare programs are accounted for, the level of U.S. unemployment fell from 22.9% in 1932 to 9.1% in 1937, a reduction of 13.8%. For 1934-1941, the corrected unemployment levels are reduced by two to three-and-a half million people and the unemployment rates by 4 to 7 percentage points after 1933.

Not surprisingly, Darby titled his 1976 Journal of Political Economy article Three-and-a-Half Million U.S. Employees Have Been Mislaid: Or, an Explanation of Unemployment, 1934-1941.

The corrected data by Darby shows stronger movement toward the natural unemployment rate after 1933. Darby concluded that his corrected date are suggests that the unemployment rate was well explained by a job search model such as that by Lucas and Rapping together with the wage fixing under the New Deal that kept real wages up and unemployment high.

Both the Keynesian approach to unemployment and the job search approach to unemployment view workers in emergency government work programs as employed and not as unemployed.

In the late 1970s, Modigliani dismissed the new classical explanation of the U.S. great depression in which the 1930s unemployment was mass voluntary unemployment as follows:

Sargent (1976) has attempted to remedy this fatal flaw by hypothesizing that the persistent and large fluctuations in unemployment reflect merely corresponding swings in the natural rate itself.

In other words, what happened to the U.S. in the 1930’s was a severe attack of contagious laziness!

I can only say that, despite Sargent’s ingenuity, neither I nor, I expect most others at least of the nonMonetarist persuasion,. are quite ready yet. to turn over the field of economic fluctuations to the social psychologist!

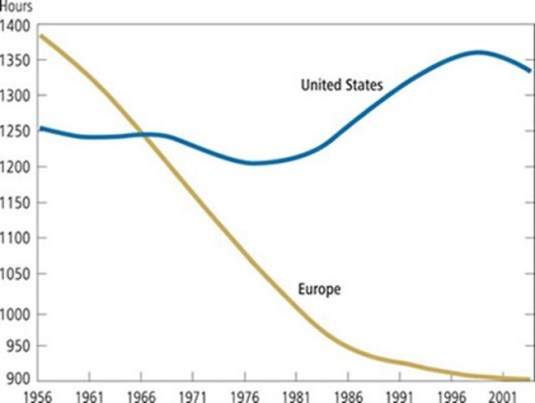

As Prescott has pointed out, the USA in the Great Depression and France since the 1970s both had 30% drops in hours worked per adult. That is why Prescott refers to France’s economy as depressed. The reason for the depressed state of the French (and German) economies is taxes, according to Prescott:

Virtually all of the large differences between U.S. labour supply and those of Germany and France are due to differences in tax systems.

Europeans face higher tax rates than Americans, and European tax rates have risen significantly over the past several decades.

In the 1960s, the number of hours worked was about the same. Since then, the number of hours has stayed level in the United States, while it has declined substantially in Europe. Countries with high tax rates devote less time to market work, but more time to home activities, such as cooking and cleaning. The European services sector is much smaller than in the USA.

Time use studies find that lower hours of market work in Europe is entirely offset by higher hours of home production, implying that Europeans do not enjoy more leisure than Americans despite the widespread impression that they do.

Richard Rogerson, 2007 in “Taxation and market work: is Scandinavia an outlier?” found that how the government spends tax revenues when assessing the effects of tax rates on aggregate hours of market work:

- Different forms of government spending imply different elasticities of hours of work with regard to tax rates;

- While tax rates are highest in Scandinavia, hours worked in Scandinavia are significantly higher than they are in Continental Europe with differences in the form of government spending can potentially account for this pattern; and

- There is a much higher rate of government employment and greater expenditures on child and elderly care in Scandinavia.

Examining how tax revenue is spent is central to understanding labour supply effects:

- If higher taxes fund disability payments which may only be received when not in work, the effect on hours worked is greater relative to a lump-sum transfer; and

- If higher taxes subsidise day care for individuals who work, then the effect on hours of work will be less than under the lump-sum transfer case.

Others such as Blanchard attribute the much lower labour force participation in the EU since the 1970s to their greater preference for leisure in Europe. An increased preference for leisure is another name for voluntary unemployment.

The lower labour force participation in higher unemployment in Europe is voluntary because of the higher demand for leisure among Europeans. According to Blanchard:

The main difference [between the continents] is that Europe has used some of the increase in productivity to increase leisure rather than income, while the U.S. has done the opposite.

An unusual left-right unity ticket emerged to explain the great depression in the 1930s and the depressed EU economies from the 1970s: the great vacation theory.

Recent Comments