Is Growth of Government Inevitable? | Sam Peltzman

12 Oct 2017 Leave a comment

in applied price theory, economic history, fiscal policy, macroeconomics, Public Choice, public economics, Sam Peltzman Tags: Director's Law, growth of government

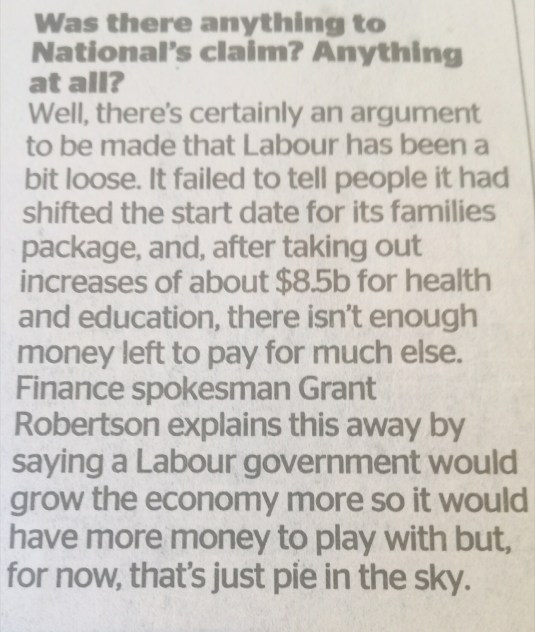

There is a hole in @NZLabour’s fiscal plan

06 Sep 2017 Leave a comment

in fiscal policy, politics - New Zealand Tags: 2017 New Zealand election

#GE2017 – Where’s the economic thinking?

04 Jun 2017 Leave a comment

in fiscal policy, macroeconomics Tags: 2017 British election, British politics

Ed Prescott makes an excellent point in his last paragraph

16 May 2017 Leave a comment

Source: RBC Methodology and the Development of Aggregate Economic Theory Edward C. Prescott, Federal Reserve Bank of Minneapolis Staff Report 527 February 2016.

Short Cut: Macron’s Scandi-Solution for France

16 May 2017 Leave a comment

in economics, fiscal policy, labour supply, macroeconomics, minimum wage, Public Choice, public economics, welfare reform

Macroeconomic Consequences of Taxing the Rich

11 May 2017 Leave a comment

in fiscal policy, macroeconomics, politics - USA, Public Choice, public economics, sports economics Tags: taxation and labour supply, top 1%

The one and only reason for the fall of the Celtic Tiger

11 May 2017 Leave a comment

in fiscal policy, macroeconomics, monetary economics, Public Choice, rentseeking

The wage bump from 1% Oz company tax cut @TheAusInstitute @GrattanInst @JordNZ

31 Mar 2017 Leave a comment

in economic growth, fiscal policy, politics - Australia, politics - New Zealand, public economics Tags: company tax incidence, endogenous growth theory, optimal tax theory

How wasteful is the Oz company tax? @TheAusInstitute @GrattanInst

30 Mar 2017 Leave a comment

Source: The incidence of company tax in Australia, Xavier Rimmer, Jazmine Smith and Sebastian Wende, Australian Treasury working paper.

Sharp ratios of @NZSuperFund since inception @TaxpayerUnion

28 Mar 2017 Leave a comment

in financial economics, fiscal policy, politics - New Zealand, public economics Tags: sharp ratios, sovereign wealth funds

The Sharp ratio describes how much excess return you are receiving for the extra volatility that you endure for holding a riskier asset. If manager A generates a return of 15% while manager B generates a return of 12%, it would appear that manager A is a better performer. But if manager A took much larger risks than manager B, manager B may be a better risk-adjusted return.

The Sharpe Ratio such as those below of the NZ Superannuation Fund can be used to compare two funds on how much risk a fund had to bear to earn excess return over the risk-free rate.

Source:New Zealand Superannuation Fund response to Official Information Act request.

The Kidney Machine Gambit & @NZSuperFund @VernonSmall @TaxpayersUnion

27 Mar 2017 Leave a comment

in fiscal policy, politics - New Zealand, public economics, television Tags: sovereign wealth funds, Yes Prime Minister

Prime Minister Jim Hacker: “Well, of course we do what we can. There are many calls on the public purse: inner cities, schools, hospitals, kidney machines…”

Recent Comments