There are plenty of critics of deregulation, albeit enough for them are smart enough to realise they cannot restore the lost monopolies and high marginal tax rates on the middle-class. They admit in their hearts that deregulation and other economic reforms worked as did inflation targeting.

The common force behind economic reform from 1980 onwards was the growing deadweight welfare losses of the pre-1980s status quo.The pressure for reform came from the rising burden that increases in taxes and regulation placed on economic growth as evidenced by the 1970s productivity slowdown and stagflation.

George Stigler argued that ideas about economic reform need to wait for a market. As Stigler noted, when their day comes, economists seem to be the leaders of public opinion. But when the views of economists are not so congenial to the current requirements of special interest groups, these economists are left to be the writers of letters to the editor in provincial newspapers and run angry blogs.

Post-1980 trends in taxes, spending, and regulation in New Zealand and abroad reflect demographic shifts, more efficient taxes, more efficient spending, a shift in the political influence from the taxed to the subsidised, shifts in political influence among taxed groups, and shifts in political influence among the subsidised groups (Becker and Mulligan 1998, 2003).

The common forces behind economic reform across the OECD area have subtle implications for the size of the reform dividend for New Zealand

- The deadweight losses of taxes, income transfers and regulation are a constraint on inefficient policies (Becker 1983, 1985; Peltzman 1989).

- This deadweight loss is the difference between winner’s gains less the loser’s losses from a tax or regulation-induced change in output. Changes in behaviour due to taxes and regulation reduce output and investment.

- Policies that significantly cut the total wealth available for distribution by governments are avoided because they reduce the payoff from taxes and regulation relative to the germane counter-factual, which are other even costlier modes of income redistribution (Becker 1983, 1985).

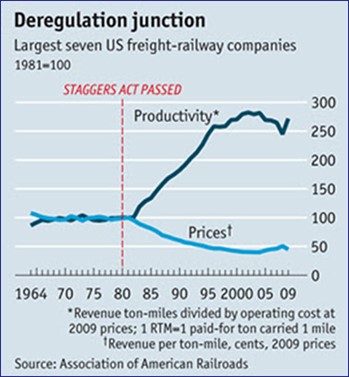

Certainly, in New Zealand, the post-1984 economic reforms followed a good 10 years of economic stagnation and regular economic crises.

In the early 1980s, New Zealand’s economy was in trouble. The country had lost its guaranteed export market when Britain joined the European Economic Union in 1973. The oil crisis that year had also taken a toll.

The Labour Party Minister of Finance, Sir Roger Douglas, prior coming to office in 1984, wrote a book called There’s Gotta Be A Better Way.

The rising deadweight cost of taxes and regulation due to technological change, and the dissipation of wealth through rising cost structures progressively enfeebled the subsidised groups, allowing others to win the initiative after the 1970s in many countries including New Zealand.

The Labour Government radically reduced the size and role of the state. It corporatised and restructured government departments, often in preparation for privatisation, and sold some state assets to private investors. It abolished many economic controls and removed farming subsidies.

The additional political pressure that the winners had to exert to keep the same dollar gain from income redistribution had to overcome rising pressure from the losers to escape their escalating losses.

Eventually, the fight was no longer worthwhile relative to the alternatives. Taxed, regulated and subsidised groups can find common ground in wealth enhancing policies and an encompassing interest in mitigating any reduction in wealth from income redistribution policies.

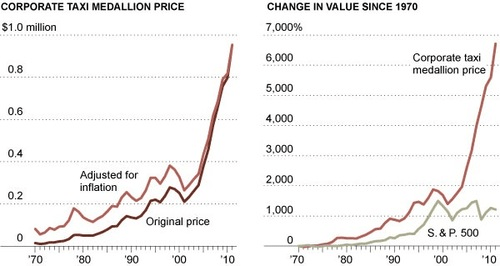

One barrier to reform is the transitional gains trap. The capitalisation of rents from taxi licenses is a classic example of the transitional gains trap.

Those who purchase the medallions from the owners at the time of initial regulation will pay the market rate for them and therefore will not receive any special rents. Yet, they will fight to prevent the taxi medallion system from being eliminated, since these owners will be harmed by such elimination. Thus, the city will be stuck with an inefficient medallion system that will be difficult to eliminate.

Eliminating the medallion program will harm existing taxis, many of whom did not lobby for the system in the first place and do not receive super competitive profits. The resources used in establishing the regulation or other programmes are lost forever.

Termination of a particular regulation or subsidies will nonetheless cause large capital losses for the incumbents. This will motivate incumbents to oppose reforms that jeopardise the income stream that has been previously capitalised (Tullock 1975; McCormick et al. 1984; Tollison and Wagner 1991). Any resources wasted in fighting economic reform must be deducted from the net gains from economic reform.

The literature on the transitional gains trap suggested that economic reform does not necessarily make society better off (Tullock 1975; McCormick et al. 1984; Tollison and Wagner 1991). The rent-seeking costs of the original privileges are capitalised and are lost forever. They are not regained by reform. The transitional gains trap is just a subset of a more general phenomenon indicating that deregulation can never replicate the status quo ante.

Too often it is assumed that deregulation can replicate the status quo ante. The prevailing model of deregulation is essentially a nirvana model, in that the gains from deregulation can essentially be had without cost. Further rent-seeking costs are incurred in lobbying for and against proposed reforms and these too are lost to forever.

The standard analysis of deregulation too easily treats reform as a return to the status quo ante. Fred McChesney observed

The airline industry of 1999 is not the airline industry of 1978 minus the Civil Aeronautics Board.

The wealth lost in rent seeking is not recovered, or even recoverable by deregulation. Production possibilities have been irretrievably diminished (McCormick et al. 1984; Tollison and Wagner 1991).

Reform is not a free lunch. To the extent that specialised resources were involved in the rent seeking–resources that could have been devoted to amassing specific capital in producing the regulated good–the deregulated relative price must be higher than the pre-regulation or competitive price. The abstract of the relevant article by Tollison and Wagner is as follows:

This paper applies the theory of rent seeking to argue that economic reform, in the sense of correcting past deformities in the economy, does not pay from a social point of view. Economic reform, at best, should focus on the prevention of future deformities.

The analysis is developed in terms of the example of monopoly, but its applicability extends to any example of economic reform. The general principle underlying the analysis is that reform is not a free lunch, all the more so when the costs of the reformer and the resistance of the object of reform are taken into account.

Despite this, new institutions arise when social groups notice opportunities for new gains which are impossible to realise under the prevailing institutional arrangements (Diana Thomas 2009). The chances that new institutional frameworks may develop increase when these alternative technological opportunities and export markets become available.

Reform is more likely when the net benefits of reform become large because there is plenty left over for credible compensation of the losers who could block change (Acemoglu and Robinson 2005; Acemoglu 2008). An example is if taxes or regulation causes cost padding or delay new technologies. Shedding these inefficiencies are potential benefits for all.

The political secret of the East Asian economic miracles was the focus on export led industrialisation. Because the new industries were exporting rather than entering and competing with domestic suppliers to home markets, these domestic special interest groups had no reason to lobby against the establishment of these export industries and otherwise blocked both their entry and the adoption of new technologies. The social change is much more subtle. The local industry is simply had to pay more for contract as the export industries grew and bid away their labour force with higher pay.

Successful subsidised groups are often coalitions of sub-sets of producers, consumers, employees and input suppliers and deregulation is always a possibility if some members can benefit from joining another coalition (Peltzman 1976, 1989). A surprising number of incumbents of regulated and state-owned industries were unprofitable – some close to bankruptcy – because of rising cost structures, the growing losses from mandated services and erosion of rents through non-price competition with existing firms. They would have closed anyway but for bailouts.

The economic reforms that picked up pace around 1980 were a success as Andrei Shleifer’s paper

The Age of Milton Freedom begins

The last quarter century has witnessed remarkable progress of mankind. The world’s per capita inflation-adjusted income rose from $5400 in 1980 to $8500 in 2005.Schooling and life expectancy grew rapidly, while infant mortality and poverty fell just as fast.

Compared to 1980, many more countries in the world are democratic today. The last quarter century also saw wide acceptance of free market policies in both rich and poor countries: from private ownership, to free trade, to responsible budgets, to lower taxes.

Recent Comments