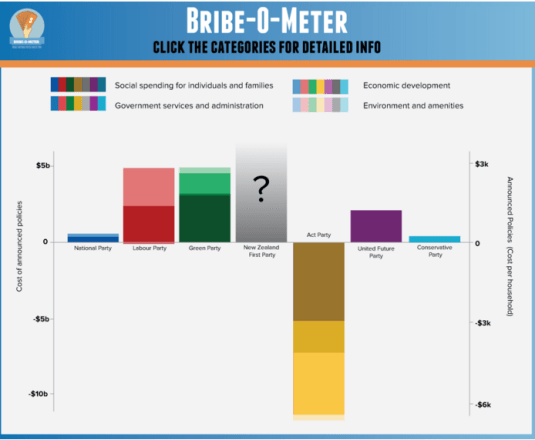

I am sure there will be lots of squabbling over parameters and assumptions of any tax, spending or regulation proposal submitted to the independent costings unit proposed recently by the New Zealand Greens.

The bigger problem is static and dynamic scoring. There is some history of doing this for taxes but little for spending and that is before you consider externalities. Imagine the squabbling over roading proposals and their externalities. The practical hurdles to dynamic scoring are:

- Economists do not know how to accurately measure the growth effects of most policies

- Dynamic scoring relies on less-than-accurate, theory-based macro models

- The macro models undergirding dynamic scoring have numerous controversial and unproven built-in assumptions

- The assumptions embedded in the macro models are not always carefully empirically based

- Macro models exclude theoretically and empirically supported evidence of supply-side effects of public investment

- Macro models exclude evidence-based effects of economic inequality

- Macro models exclude evidence-based effects of numerous policies

- Macro models provide different estimates of growth impacts of policy depending on guesses of how the policy may be finance

Against that is dynamic scoring removes the bias against pro-growth policies in current budgetary scoring:

[A] theoretical advantage of accurate dynamic scoring is that it is not biased against pro-growth policies compared to the current conventional scoring method. By ignoring macroeconomic effects, the conventional method overstates the true budgetary cost of pro-growth policies, such as infrastructure investments, and understates the cost of anti-growth policies.

The bigger problem is something I learnt when costing a tax proposal for an election campaign. There was an error because I did the costing on a spreadsheet while I had a bad head cold.

The advantage of the error was the policy, as a result of this minor error in the tabulations attracted considerable attention from the major parties.

I was advised by a very wise head that this tabulation error in the dynamic scoring was not so bad a problem. This was because the tabulation error gave our side a chance to have a go at them again in the media. The policy announcement stayed in the new cycles for longer than otherwise and attracted attention from the big parties.

If a policy is too good, too perfect, the other parties will kill it with silence. You get only one bite in the news cycle and that is it.

If your policy announcement is killed by silence, at least you are guaranteed a chance to go at it again when the proposed independent costings unit a week or so later in the election campaign. You might disagree of those costings just to attract attention in the next new cycle.

Given the size, ambition and nebulous externality content of Green party proposals, they will benefit considerably from getting another go by questioning the Parliamentary budget office costings. That guarantees at least two new cycles to every one of their budgetary and regulatory announcements. No wonder they have proposed this independent costings unit.

If the New Zealand Greens do not like the costing from their proposed independent costings unit, they can just rage against neoliberalism and the conservative bias of economists. They cannot lose in terms of another bite of the 24-hour news cycle.

As a starter to feigning disagreement with any independent costings of their tax, spending and regulation proposals, Milton Friedman argued that people agree on most social objectives, but they differ often on the predicted outcomes of different policies and institutions. This leads us to Robert and Zeckhauser’s taxonomy of disagreement:

Positive disagreements can be over questions of:

1. Scope: what elements of the world one is trying to understand?

2. Model: what mechanisms explain the behaviour of the world?

3. Estimate: what estimates of the model’s parameters are thought to obtain in particular contexts?

Values disagreements can be over questions of:

1. Standing: who counts?

2. Criteria: what counts?

3. Weights: how much different individuals and criteria count?

Any positive analysis tends to include elements of scope, model, and estimation, though often these elements intertwine; they frequently feature in debates in an implicit or undifferentiated manner. Likewise, normative analysis will also include elements of standing, criteria, and weights, whether or not these distinctions are recognised. There is a rich harvest for nit-picking to keep the story going.

/cdn0.vox-cdn.com/uploads/chorus_asset/file/5925471/sanders-taxes5002.jpg)

Recent Comments